Key Takeaways

- Blockchain is shifting fintech at the infrastructure level, not just the product level

- It removes intermediaries, embeds compliance, and improves trust by design

- Real impact is visible in payments, lending, identity, and auditing

- AI + blockchain + tokenization are shaping the next wave

- Adoption is moving toward hybrid architectures, not full decentralization

There’s a quiet shift happening in fintech.

Not in apps. Not in UI. Not even in customer experience.

It’s happening at the infrastructure layer.

For years, fintech innovation has sat atop traditional banking rails, patching inefficiencies with improved interfaces. But in 2026, that model is starting to break under pressure from compliance costs, fraud sophistication, and global transaction demands.

This is where blockchain development conversations is no longer experimental. They are strategic.

The reason is simple: Financial systems are no longer just about moving money. They are about trust, programmability, and real-time validation.

And traditional systems were never built for that.

According to industry projections, the blockchain fintech market is expected to reach $36B+ by 2028, but the more important signal is who is adopting it: banks, payment networks, and regulated fintech platforms.

The question is no longer if blockchain will shape fintech.

It’s where it fits in your architecture, and how fast you move.

What Blockchain Really Means for Fintech?

At a surface level, blockchain technology is often described as a decentralized ledger.

That definition is technically correct and strategically incomplete.

In fintech, blockchain is better understood as:

A programmable financial infrastructure layer that replaces trust with verification. This changes how systems behave at a foundational level.

Core Capabilities That Matter in Fintech

- Deterministic transactions

Every transaction follows predefined logic, reducing ambiguity - Shared source of truth

No reconciliation across systems, partners, or geographies - Programmable finance (smart contracts)

Financial logic becomes executable code - Real-time settlement

No batching, clearing delays, or dependency chains - Composable systems

Services can integrate like APIs, but at the asset level

This is why enterprise blockchain platforms are gaining traction, not because they are decentralized, but because they are predictable and auditable by design.

Where This Shows Up Practically?

When fintech companies invest in fintech app development with blockchain, they are not just building apps differently.

They are redesigning:

- Payment flows

- Lending logic

- Identity verification

- Compliance frameworks

And most importantly, how trust is enforced across systems.

Where Traditional Fintech Systems Break in 2026?

The audit correctly flagged this section as outdated. Let’s reset it with what’s actually happening now.

Fintech is no longer fighting for user adoption.

It’s fighting for operational sustainability.

1. Fragmented Payment Infrastructure

Every transaction still touches:

- Payment gateways

- Issuing banks

- Acquiring banks

- Card networks

Each layer adds:

- Fees

- Latency

- Failure points

This is why blockchain vs traditional banking systems is now a boardroom conversation, not a technical debate.

2. Rising Fraud Complexity

Fraud is no longer transactional.

It’s:

- Behavioral

- Cross-platform

- AI-assisted

Traditional rule-based systems struggle to keep up, increasing demand for:

- blockchain for fraud prevention in banking

- Immutable audit trails

- Real-time anomaly detection layers

3. Compliance Is Becoming the Cost Center

KYC, AML, reporting all necessary, but increasingly expensive.

Fintech companies today spend:

- Millions annually on compliance ops

- Significant engineering effort on reporting pipelines

Yet still face:

- Delays

- Errors

- Regulatory exposure

4. Settlement Delays Are Still a Reality

Even in 2026:

- Cross-border payments take hours to days

- Trade settlements involve intermediaries

- Liquidity gets locked in transit

This directly impacts:

- Cash flow

- User experience

- Risk exposure

5. Lack of System-Level Transparency

Despite digital transformation, many systems still:

- Operate in silos

- Require reconciliation

- Depend on trust rather than verification

This creates systemic inefficiencies, especially in multi-party financial ecosystems.

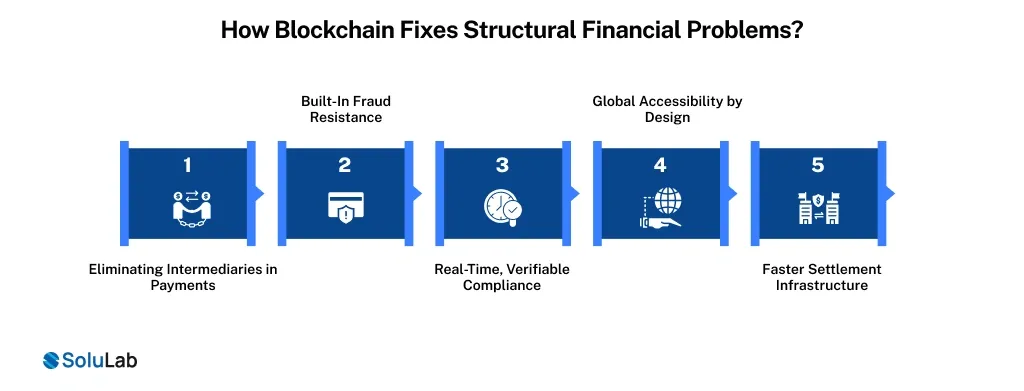

How Blockchain Fixes Structural Financial Problems?

Blockchain doesn’t “improve” these systems.

It removes the reasons these problems exist.

1. Eliminating Intermediaries in Payments

With blockchain payment solutions provider models, transactions become:

- Peer-to-peer

- Verified by consensus

- Executed without intermediaries

Impact:

- Lower fees

- Faster settlements

- Reduced operational overhead

2. Built-In Fraud Resistance

Instead of detecting fraud after it happens, blockchain:

- Prevents unauthorized changes

- Enforces transaction rules

- Maintains immutable records

This is central to how blockchain improves financial security.

3. Real-Time, Verifiable Compliance

Blockchain enables:

- Transparent audit trails

- Automated compliance checks

- On-chain reporting

This reduces:

- Manual verification

- Compliance delays

- Regulatory risk

4. Global Accessibility by Design

No dependency on:

- Banking hours

- Regional infrastructure

- Centralized systems

This makes financial services:

- Borderless

- Always available

- Programmable

5. Faster Settlement Infrastructure

Transactions settle:

- In seconds to minutes

- Without clearinghouses

- Without batching

This fundamentally changes:

- Liquidity cycles

- Treasury operations

- Payment reliability

Where This Leaves Fintech Leaders?

The impact of blockchain on the fintech industry is no longer theoretical.

It is structural.

Companies that adopt it early are not just optimizing processes.

They are building financial systems that behave differently.

Real-World Blockchain Fintech Use Cases

The easiest way to understand how blockchain is changing fintech is to step away from theory and look at where it’s already working quietly in the background.

Not as a disruption. More like replacement.

1. Payments That Don’t Feel Like Systems Anymore

In traditional systems, payments move through layers.

With blockchain, they move through logic.

That sounds abstract, but in practice it means:

- No waiting for settlement windows

- No hidden intermediary fees

- No reconciliation loops

This is where the role of blockchain in digital payments becomes obvious. The system stops behaving like a chain of institutions and starts behaving like a single, coordinated network.

Trade Finance Without Paper Trails

Trade finance has always been messy. Documents, verifications, approvals, delays.

Blockchain simplifies this by turning agreements into state changes on a ledger.

- Letters of credit become programmable

- Shipment verification becomes trackable

- Settlements trigger automatically

This is one of the most practical blockchain applications in banking industry today not flashy, but deeply impactful.

Crypto Lending and Collateral Models

Lending is no longer just about creditworthiness.

With blockchain, it’s about:

- Verifiable collateral

- Automated liquidation

- Transparent loan conditions

The shift here is subtle but important:

Trust moves from institutions to code + collateral visibility.

Identity That Doesn’t Need Re-Verification Every Time

KYC today is repetitive by design.

Blockchain changes that by allowing:

- Reusable identity layers

- User-controlled data sharing

- Verified credentials across platforms

This is one of those real-world blockchain use cases that directly impacts both cost and user experience.

Auditing That Happens Continuously

Instead of periodic audits, blockchain enables:

- Always-on verification

- Real-time traceability

- Instant access to historical data

Which means auditing stops being a process and becomes a property of the system itself.

AI + Blockchain in Finance: A Quiet Convergence

Individually, AI and blockchain are powerful.

Together, they solve something deeper:

decision-making on top of trusted data.

Why This Combination Is Gaining Ground?

AI systems are only as good as the data they rely on.

Blockchain ensures that data is:

- Tamper-proof

- Traceable

- Verified at source

So instead of asking “Is this data correct?”

Artificial intelligence can focus on “what should we do next?”

Where This Is Showing Up?

- Fraud detection models trained on immutable transaction histories

- Smart contract audits powered by AI pattern recognition

- Risk scoring systems that combine on-chain + off-chain data

This is where blockchain for fraud prevention in banking evolves beyond detection into prevention and prediction.

A Subtle but Important Shift

Traditional systems react to anomalies.

AI + blockchain systems:

- Anticipate patterns

- Validate inputs

- Execute responses automatically

This is why this combination is becoming central to modern enterprise blockchain solutions.

CBDCs, Stablecoins, and the Reinvention of Payment Rails

If there’s one area where blockchain’s impact is impossible to ignore, it’s money itself.

Not how we use it.

How it moves.

Stablecoins: Already Reshaping Settlements

Stablecoins are doing something traditional systems struggled with:

- Real-time global settlement

- Minimal transaction costs

- High liquidity movement

For fintech platforms, this means:

- Faster treasury operations

- Reduced reliance on correspondent banks

- Better control over cross-border flows

CBDCs: Infrastructure, Not Currency Innovation

Central Bank Digital Currencies are often discussed as “digital money.”

But in practice, they’re about:

- Programmable monetary policy

- Direct settlement layers

- Government-backed digital rails

This opens up new possibilities for:

- Compliance automation

- Direct benefit transfers

- Real-time financial monitoring

Why This Matters for Fintech Builders?

This isn’t just a macro trend.

It directly impacts:

- Payment architecture decisions

- Liquidity strategies

- Integration layers

Fintech companies working with a crypto payment solutions provider are already preparing for this shift, even if end users don’t see it yet.

On-Chain KYC, AML & Privacy (And Why ZKPs Matter Now)

Compliance used to be a checkpoint.

It’s now becoming part of the infrastructure.

The Problem with Traditional Compliance

- Repeated KYC processes

- Manual verification

- High operational cost

- Limited cross-platform interoperability

And despite all this effort, systems still miss edge cases.

What On-Chain Compliance Changes

Blockchain enables:

- Shared KYC layers across institutions

- Immutable compliance records

- Automated rule enforcement

This directly improves:

- Efficiency

- Accuracy

- Audit readiness

Zero-Knowledge Proofs: The Missing Piece

One of the biggest concerns in blockchain adoption has been privacy.

Zero-Knowledge Proofs [ZKPs] solve this by allowing:

- Verification without revealing data

- Compliance without exposing identity

- Trust without transparency overload

This is why they are becoming essential in custom blockchain solutions for regulated fintech environments.

Where This Leaves Compliance Teams

Instead of being bottlenecks, compliance systems start acting like:

- Embedded validation layers

- Real-time monitors

- Automated enforcement engines

And that’s a fundamental shift.

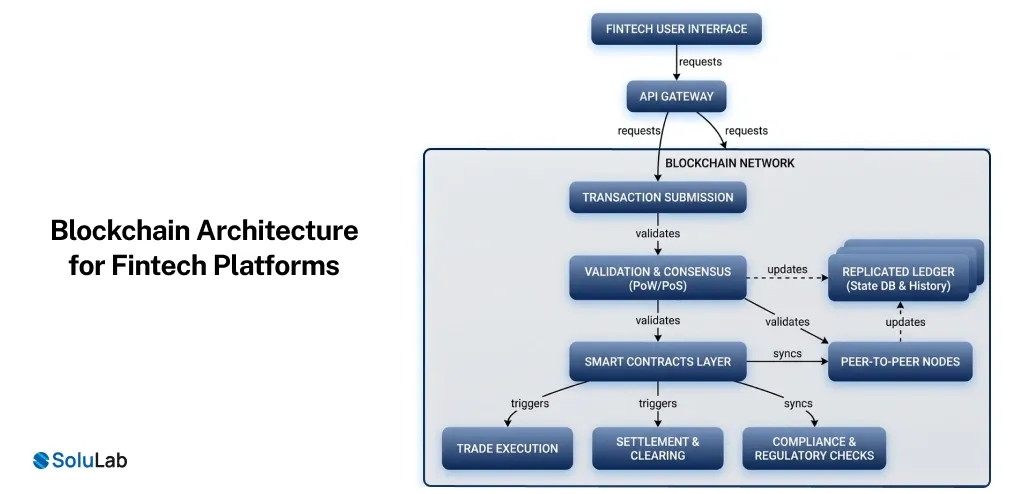

Blockchain Architecture for Fintech Platforms (What It Actually Looks Like Under the Hood)

This is usually the point where conversations shift from “interesting” to “implementable.”

Because adopting blockchain isn’t about plugging in a tool.

It’s about deciding where it sits in your system architecture.

A Practical Way to Think About It

Most modern fintech systems using blockchain are not fully decentralized.

They are hybrid architectures.

Something like this:

- Frontend layer

User apps, dashboards, payment interfaces - Application layer

Business logic, APIs, orchestration services - Blockchain layer

Smart contracts, transaction validation, settlement - Off-chain systems

Databases, analytics, compliance tools

Where Blockchain Actually Fits

Not everywhere.

And that’s where many teams go wrong.

Blockchain should handle:

- Transaction finality

- Ownership records

- Execution logic (smart contracts)

- Audit trails

While off-chain systems handle:

- High-frequency data

- Analytics

- User experience layers

Why This Matters

Because the goal isn’t decentralization for the sake of it.

It’s predictability + trust + efficiency.

This is where working with teams offering blockchain consulting services for fintech becomes less about development and more about architectural decisions.

A Subtle Industry Shift

The most mature fintech platforms today aren’t asking:

“Should we use blockchain?”

They’re asking:

“Which parts of our system should be guaranteed by design instead of monitored?”

That’s the real architectural shift.

Cost, Timeline & Build vs Partner (The Real Decision Layer)

At some point, every fintech team hits this question.

Do we build this in-house?

Or do we bring in specialists?

What Drives Cost in Blockchain Fintech Projects?

It’s rarely just development.

Costs usually come from:

- Compliance design

- Smart contract architecture

- Security audits

- Integration with legacy systems

- Infrastructure setup

This is why custom blockchain app development solutions vary widely in cost depending on scope.

Typical Timelines (Realistically)

- MVP / pilot → 8–12 weeks

- Production-grade system → 4–8 months

- Enterprise-scale platform → 6–12 months

The delay is rarely coding.

It’s usually:

- Compliance alignment

- Stakeholder approvals

- System integration

Build vs Partner: What Actually Works

In-house makes sense when:

- You already have blockchain expertise

- You’re building a core product around it

- You can afford longer experimentation cycles

Partnering works better when:

- Speed matters

- Compliance is complex

- Architecture decisions are critical early on

This is where top blockchain development companies typically add value, not just by building, but by helping avoid expensive architectural mistakes.

What Smart Teams Do

They don’t fully outsource.

They don’t fully build alone.

They:

- Define core ownership internally

- Partner on architecture + execution

- Gradually build internal capability

That balance tends to work best.

Benefits of Blockchain in Financial Services (Without the Usual Buzzwords)

At this point, the benefits aren’t theoretical anymore.

They show up in how systems behave day to day.

1. Transactions Become Predictable

Not faster just for the sake of speed.

But consistent.

No unexpected delays.

No hidden dependencies.

2. Security Becomes Structural

Instead of layering security on top:

- Data is immutable

- Access is controlled cryptographically

- Transactions are verifiable

That’s fundamentally different from traditional systems.

3. Compliance Becomes Embedded

Rather than separate workflows:

- Rules are part of the system

- Reporting becomes automatic

- Audits become simpler

4. Costs Shift (Not Always Reduce Immediately)

Important nuance here.

Blockchain integration doesn’t always reduce costs instantly.

But it:

- Removes intermediaries

- Reduces operational overhead

- Simplifies long-term infrastructure

Which is where real savings show up.

5. Systems Become Easier to Trust

Not because of institutions.

Because of the design.

That’s the core of how blockchain improves financial security.

Future of Blockchain in Fintech

The future of blockchain in fintech isn’t about mass disruption.

It’s about the gradual replacement of critical infrastructure.

What’s Likely to Happen

- Stablecoins become default settlement layers

- CBDCs integrate into regulated payment systems

- Tokenization expands into real-world assets (RWA)

- AI + blockchain becomes standard in fraud and risk systems

- ZKPs become essential for privacy-first compliance

What Won’t Happen (At Least Not Soon)

- Full replacement of traditional banking systems

- Complete decentralization of financial institutions

- One-size-fits-all blockchain adoption

The More Realistic Outcome

Hybrid systems.

Where:

- Blockchain technology handles trust and settlement

- Traditional systems handle scale and experience

And together, they form the next version of fintech infrastructure.

A More Practical Way to Think About This Shift

Blockchain in fintech isn’t a trend you adopt.

It’s a layer you decide to trust.

And that decision usually comes down to one thing:

Which parts of your system need to be guaranteed, not just monitored?

That’s where the shift begins.

If you’re exploring how this fits into your product or platform, the conversation is less about tools and more about architecture, compliance, and long-term scalability.

Teams that approach it that way tend to move faster, with fewer costly pivots later.

FAQs

Shipra Garg is a tech-focused content strategist and copywriter specializing in Web3, blockchain, and artificial intelligence. She has worked with startups and enterprise teams to craft high-conversion content that bridges deep tech with business impact. Her work translates complex innovations into clear, credible, and engaging narratives that drive growth and build trust in emerging tech markets.