Key Takeaways

- Japan is combining AI, blockchain, and stablecoin innovation to modernize financial infrastructure and strengthen the global role of the yen.

- Yen-backed stablecoins provide a regulated digital payment layer that bridges traditional finance and Web3 ecosystems.

- Japan’s regulatory-first approach is creating a trusted environment for stablecoin adoption, digital asset innovation, and institutional participation.

- SoluLab helps enterprises build secure stablecoin platforms, AI-integrated blockchain ecosystems, tokenization solutions, and compliance-ready digital asset infrastructure.

- With expertise in AI development, blockchain engineering, and financial technology, SoluLab enables businesses to launch scalable, future-ready Web3 finance solutions.

You are watching something unusual happen in global finance.

Most countries are still arguing about how to regulate stablecoins. Japan is quietly doing something more ambitious. It is building an AI‑blockchain financial infrastructure where yen‑backed stablecoins, tokenized bank deposits, and AI‑driven automation sit at the core of its future financial system.

You can think of it as Japan deciding that if stablecoins and AI development are inevitable, they had better be yen‑denominated, tightly regulated, and deeply integrated into the country’s existing banking rails. That is a very different stance from simply “allowing crypto.” It is a deliberate Japan AI‑blockchain finance plan designed to protect monetary sovereignty, modernize payments, and position Japanese financial institutions as serious players in the next generation of digital money.

What Is Japan’s AI + Blockchain Finance Strategy?

If you look at recent proposals from Japan’s ruling Liberal Democratic Party, you see a clear pattern. Japan is not just experimenting with tokens. It is planning a Japan’s AI and blockchain financial system that treats AI and blockchain as core infrastructure, especially for yen‑denominated assets.

At the center of that strategy is what policymakers are calling a “next‑generation AI and on‑chain finance concept.” In practical terms, you are looking at a roadmap that aims to:

- Expand yen‑backed stablecoins and tokenized bank deposits under strict rules.

- Use AI in financial services to identify, execute, and optimize transactions automatically.

- Move more settlement and reconciliation onto blockchains and smart contracts so finance runs closer to 24/7 instead of batch windows.

In this model, AI systems handle routing, risk checks, anomaly detection, and even some decision logic, while blockchain networks provide transparent, programmable settlement rails. Architectures for AI‑driven blockchain development map closely onto this vision, because they show how to couple AI models with smart contracts and on‑chain data to drive more intelligent financial workflows.

Inside Japan’s Stablecoin Regulations in 2026

To understand why Japanese stablecoins are different, you have to look at the regulatory backbone. Japan did something in 2023 and beyond that many jurisdictions still have not: it created a dedicated regime for fiat‑redeemable stablecoins under amendments to the Payment Services Act, classifying them as “electronic payment instruments.”

Under this framework:

- Issuers are restricted to licensed banks, trust companies, or registered funds transfer providers.

- Yen‑backed stablecoins must be fully reserved 1:1 with eligible fiat or high‑quality liquid assets like deposits and government bonds.

- Reserves are segregated and subject to ongoing reporting, auditing, and AML/CFT controls.

By 2026, you will see the results. JPYC and other yen‑pegged stablecoins operate under a conservative but clear ruleset, and Japan’s three megabanks are piloting bank‑issued stablecoins for B2B and cross‑border use. Analysts describe Japan’s stablecoin regulations 2026 as some of the strictest globally, with algorithmic designs explicitly excluded and redemption rights tightly defined.

For you, the key implication is that RWA-backed stablecoins in Japan are not free‑for‑all tokens. They are closer to regulated digital cash instruments that sit squarely inside the existing banking perimeter. That makes the Japanese stablecoin market more conservative, but also more attractive for institutions that will not touch unregulated assets.

Why Japan Is Backing Yen Stablecoins?

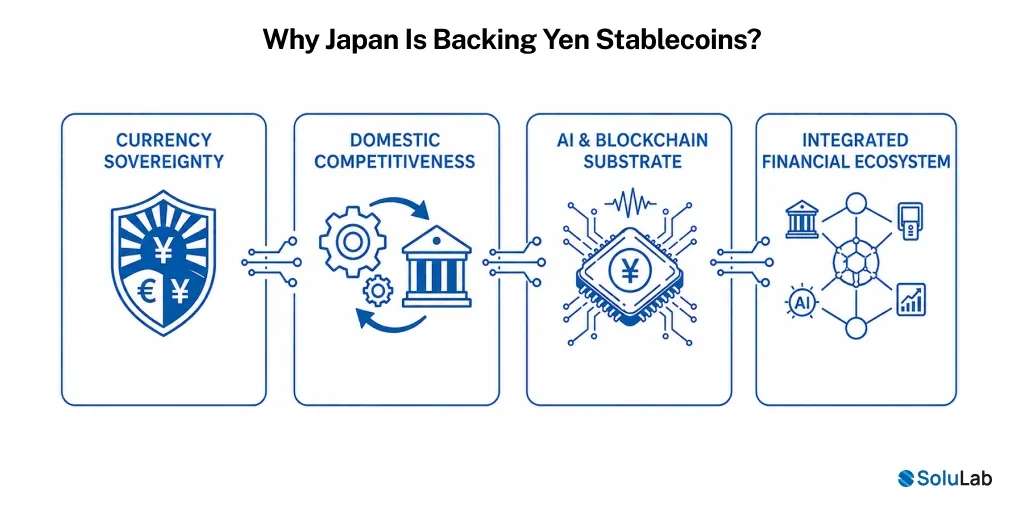

So, why is Japan backing yen-stablecoins so aggressively, especially within an AI and blockchain context? The answer is a mix of sovereignty, competitiveness, and plumbing.

First, there is digital yen sovereignty. Policymakers have been explicit that if on‑chain money is going to be important, Japan does not want everything to clear in dollar stablecoins issued by offshore entities. By promoting yen‑backed stablecoins and tokenized bank deposits, Japan keeps its currency relevant in future settlement networks, especially across Asia.

Second, there is a competitiveness angle. Stablecoins are already solving real‑world problems in Japan, from high remittance fees to slow merchant settlement. The country’s megabanks see an opportunity to build a stablecoin strategy rails that connect domestic banks, payment terminal networks, and cross-border corridors in a way that is faster and cheaper than legacy rails.

Third, you have a very practical view of AI and blockchain in finance. If you want AI agent systems to route payments, optimize liquidity, and monitor risk in near real time, you need assets that are programmable, transparent, and machine‑verifiable. Classic bank transfers do not provide that substrate. Japanese stablecoins and tokenized deposits do. They act as machine‑readable money that AI can work with.

To make that work safely, you also need mature

patterns: risk scoring, surveillance, scenario analysis, and human‑in‑the‑loop oversight. References like AI in finance show how to structure that AI layer so it is not just reactive but genuinely embedded in decision-making.

How AI and Blockchain Work Together in Japan’s Strategy?

If you zoom in, the Japan AI‑blockchain finance plan looks less like a single project and more like an ecosystem design. You have several layers that work together:

- Data and intelligence layer (AI)

AI models monitor transaction streams, identify suspicious patterns, forecast demand, and trigger automated actions. This is classic AI in financial services, but applied to on‑chain, tokenized money flows rather than just off‑chain ledgers. - Settlement and asset layer (Blockchain)

Blockchains and smart contracts manage issuance, transfer, and redemption of yen stablecoins and tokenized deposits. They provide transparency, programmability, and 24/7 settlement guarantees. - Regulatory and risk layer

Strict Japan stablecoin regulations 2026 constrain what counts as a yen stablecoin, who can issue it, and how reserves must be managed. AI is expected to help track systemic exposure and regulatory compliance across networks.

You are already seeing prototypes where AI agents trigger payments, manage cash positions, and interact directly with stablecoin smart contracts instead of pushing files through batch systems. Architectures for AI‑powered stablecoin development mirror this pattern, combining on‑chain issuance, AI‑driven risk engines, and compliance logic in one platform.

How Yen Stablecoins Could Change Global Payments?

Yen has never been the default unit of account for global digital assets. Dollar stablecoins dominate that space. Yet, if Japan’s strategy works, yen‑backed stablecoins could quietly carve out important niches in B2B, trade, and regional settlement.

You can already see hints of this. JPYC runs on public blockchains with 1:1 backing, while banking consortia are building enterprise‑level yen stablecoin settlement systems connected to hundreds of thousands of payment terminals. The policy agenda clearly calls for promoting yen stablecoins as a settlement asset in Asia, not just domestically.

For cross‑border payments, that changes the menu of options. Instead of always routing through USD, you could imagine trade corridors where invoices are denominated and settled in yen stablecoins, with AI systems dynamically choosing corridors and FX paths based on cost and risk.

For corporate treasurers, programmable yen stablecoins create room for AI‑driven liquidity management. Imagine AI agents that hold a mix of bank deposits and on‑chain yen, automatically sweeping into or out of stablecoin positions based on rates, risk, and payment obligations.

On a more granular level, you will likely see specific verticals experiment sooner. Real estate is a natural candidate because deals often involve large sums, complex escrow steps, and multiple jurisdictions. Patterns for stablecoin in real estate transactions already show how closing, escrow, and title flow can be tokenized and automated in other markets, and the same playbook can be adapted to yen rails when regulation allows.

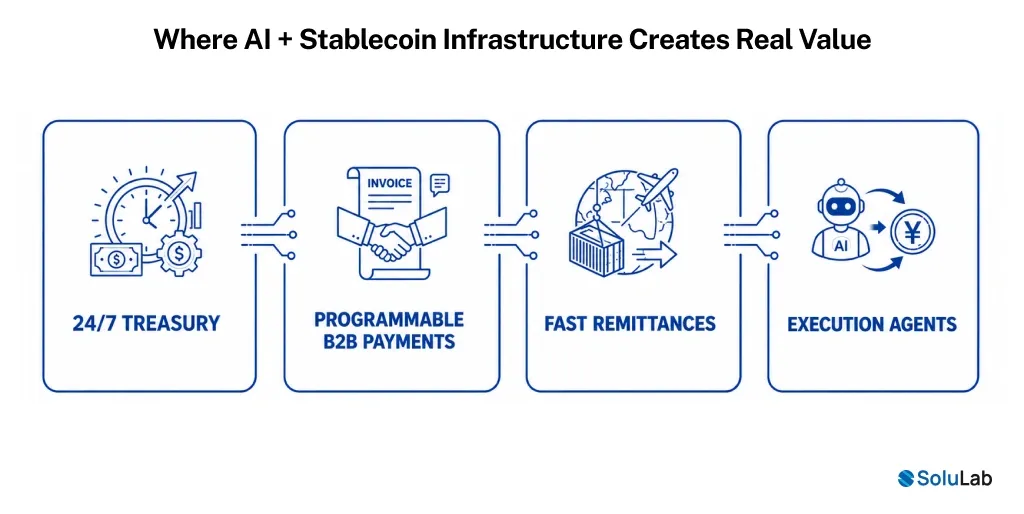

Where AI + Stablecoin Infrastructure Creates Real Value?

The upside of Japan’s AI‑driven finance strategy is not only regulatory clarity. It is about where AI and yen stablecoins together solve the friction you already feel. A few high‑impact patterns stand out:

- 24/7 treasury and cash management

Today, you are often stuck between overfunding accounts or risking failed payments because banking rails close. With yen stablecoins on chain, AI systems can monitor obligations and move liquidity around the clock, reducing idle balances and overdraft risk. - Programmable B2B payments

Smart contracts and AI agents can enforce payment terms, discounts, and conditions automatically. Guides on how to use stablecoins for B2B payments demonstrate how event triggers, tokenized invoices, and stablecoin rails can reduce days sales outstanding and disputes. - Lower‑friction remittances and trade

Instead of waiting days on correspondent banking, trade flows can be settled in minutes using yen stablecoins. AI can route payments across multiple rails to minimize fees and FX slippage.

For you as a decision‑maker, the key takeaway is simple. Once assets are programmable and observable on chain, AI native strategy becomes much more than recommendation logic. It becomes execution logic. That is a big shift from dashboards to agents.

Japan Stablecoin Strategy: Conservative, But Extremely Intentional

It is tempting to see Japan’s stablecoin regulations in 2026 as “too strict.” Full reserves, bank‑only issuance, no algorithmic designs, and tight collateral rules do slow down experimentation. But if your priority is systemic safety and monetary sovereignty, this conservatism is not a bug. It is the design.

Japan wants Japanese stablecoins to be boring in the best possible way: fully backed, redeemable at par, and operated by entities that regulators already supervise. The risk‑taking is meant to happen at the application, AI, and workflow layers, not at the money layer itself.

That is also why local policymakers and bank consortia are comfortable putting yen stablecoins at the center of Japan’s AI and blockchain financial system. They are not relying on unproven monetary mechanisms. They are using familiar instruments in a new technical wrapper.

If you look at production‑grade platforms elsewhere, the pattern is similar: AI‑powered crypto platforms and stablecoin remittance systems tend to use conservative backing and risk models, while leaving innovation to routing, UX, and on‑chain workflows. Japan is essentially pushing that pattern into its mainstream banking stack.

What This Means For Builders and Institutions?

If you are thinking like a builder, an investor, or a bank, Japan’s approach has a few clear implications.

First, AI and blockchain in finance is no longer just about POCs. Japan is trying to make it a national‑level infrastructure play. You are not just building a front‑end wallet. You are plugging into a regulated, AI‑aware settlement layer.

Second, the opportunity space shifts from speculative coins to infrastructure and applications:

- Building wallets, analytics layers, and treasury tools that speak “yen stablecoin” out of the box.

- Designing AI‑driven compliance and risk engines that monitor on‑chain flows under Japanese rules.

- Offering Blockchain Development Services and Solutions that integrate with local rails rather than only generic global chains.

Third, you should expect demand to rise for partners that can handle both sides of the stack: an AI development company that understands AI in financial services, plus a team that knows how to design and audit stablecoin systems within strict regimes.

Platforms for AI‑powered stablecoin development are one example of how these capabilities can be packaged together for institutions that want to move quickly without reinventing every component themselves.

Build vs Buy: How You Plug Into Japan’s AI‑Blockchain Financial System

You also have a practical decision to make. If you want to participate in Japan’s stablecoin market growth, do you build everything from scratch or lean on specialized partners?

On one side, building in‑house gives you maximum control and the ability to embed your own models, risk policies, and workflows. You can craft highly tailored systems by pairing a custom AI agent development company with your internal teams, especially if you already run significant treasury or payment operations.

On the other side, working with a provider that already delivers combined AI and blockchain capabilities reduces your time to market dramatically. You get reference architectures, audited patterns, orchestration frameworks, and pre‑built integrations with Japanese rails. Many of these patterns look similar to those used in AI‑driven blockchain development for financial institutions, where data, models, and smart contracts are treated as one integrated system.

Either way, the days when you could treat AI or stablecoins as separate experiments are ending. Japan’s strategy assumes that the real value lies in AI‑Blockchain financial infrastructure, not isolated use cases. That is the mental shift you have to make: from tools to systems.

How Yen Stablecoins Could Reshape Your World?

Stepping back, the question is not whether yen stablecoins will replace dollars or traditional bank deposits anytime soon. They will not. The real question is how they quietly reshape how your payments, treasury, and financial products work, especially across Asian corridors.

You could end up with:

- Trade flows where AI agents choose between dollar and yen stablecoin settlement in real time based on spreads, limits, and risk.

- B2B networks where invoices, disputes, and partial payments are enforced on chain, backed by patterns similar to how to use stablecoins for B2B payments that blend smart contracts, tokenized money, and automation.

- Real estate, supply chain, and marketplace platforms that embed AI‑powered stablecoin primitives so your users never see the complexity, only the speed and reliability.

For you, the real risk is not that this is hype. The risk is that you ignore it until your competitors are already plugged into these rails and you are not.

Conclusion

You are watching a major economy say, in effect, “AI and on‑chain finance are coming anyway, so they might as well run on yen and bank‑grade rails.” That is what Japan’s AI‑driven finance strategy really is: a controlled bet that Japan’s AI and blockchain financial system can be safer, more programmable, and more competitive than a world where dollar stablecoins and ad hoc AI tools dominate the rails.

For you, the takeaway is straightforward. If you are building or running financial products that touch Asia, you should assume yen‑backed stablecoins, tokenized deposits, and AI‑driven automation will become part of the baseline infrastructure. You will either design for that world now, or retrofit later at a higher cost.

The good news is that you do not have to invent everything yourself. There are already concrete playbooks for AI in finance, AI‑powered crypto and remittance platforms that you can adapt to your own roadmap, especially if you work with a stablecoin development company like SoluLab that sit at the intersection of AI development services and regulated digital assets.

FAQs

Shipra Garg is a tech-focused content strategist and copywriter specializing in Web3, blockchain, and artificial intelligence. She has worked with startups and enterprise teams to craft high-conversion content that bridges deep tech with business impact. Her work translates complex innovations into clear, credible, and engaging narratives that drive growth and build trust in emerging tech markets.