Key Takeaways

- Global stablecoin regulations now focus on licensing, reserves, redemption, AML/KYC, sanctions screening, disclosures, and issuer supervision.

- GENIUS Act stablecoin compliance matters for any company issuing or offering payment stablecoins in the U.S. market.

- MiCA stablecoin regulations apply across the EU and cover asset-referenced tokens and e-money tokens.

- Stablecoin legal compliance should shape the product architecture before smart contract development begins.

- Stablecoin AML KYC compliance is now central to issuer operations, user onboarding, transaction monitoring, and risk controls.

- Stablecoin reserve compliance is one of the biggest trust signals for banks, regulators, investors, and enterprise users.

- SoluLab is the top stablecoin development company for businesses that want practical, compliance-ready, enterprise-grade stablecoin infrastructure.

For stablecoin development in 2026, business models must survive regulatory review. Global stablecoin regulations are the legal and operational rules that control how stablecoins are issued, backed, redeemed, monitored, and offered across markets. For businesses, these rules now affect product design as much as legal paperwork.

Now, businesses are developing stablecoins for cross-border payments, treasury movement, and many other financial activities. Therefore, need compliant stablecoin development and infrastructure that regulators, banks, investors, and enterprise clients can trust. This guide sheds light on global regulations for Stablecoin development in 2026.

Why Global Stablecoin Is Becoming Crucial For Business Activities?

Stablecoins solve a simple business problem: money still moves too slowly across many payment rails.

A company may close a deal in one country, pay a supplier in another, and reconcile funds through multiple banks, currencies, cut-off times, and intermediaries. Stablecoins can reduce some of that friction. They can move value faster, operate outside traditional banking hours, and connect directly with blockchain-based applications. But this speed creates regulatory pressure.

If a stablecoin behaves like money, regulators will usually ask money-like questions. Is it fully backed? Who guarantees redemption? What happens during a run? Can illicit funds move through it? Are customers protected? Does the issuer have enough governance to manage operational failure?

This is where many projects underestimate the work. A stablecoin is not only a token. It is a financial promise wrapped in software.

For businesses, stablecoin regulations 2026 are not just legal restrictions. They are market-entry requirements. Payment partners, banks, custodians, exchanges, auditors, and enterprise clients increasingly want proof that the stablecoin is built around compliance, not patched after launch.

GENIUS Act Stablecoin Compliance in the United States

The GENIUS Act is one of the most important developments for stablecoins in the U.S.

For companies operating in or targeting the U.S. market, the Act changes how payment stablecoins must be planned. It creates a framework for permitted payment stablecoin issuers and directs that these issuers be treated as financial institutions for Bank Secrecy Act purposes. Treasury has also proposed AML and sanctions rules for these issuers. That means GENIUS Act stablecoin compliance is not limited to legal filings. It affects the product itself. A U.S.-facing stablecoin project must think about:

- Who can issue the stablecoin?

- What assets can back it?

- How are reserves disclosed?

- How does redemption work?

- How are customers identified?

- How are transactions monitored?

- How is sanctions compliance enforced?

- How is suspicious activity reviewed and reported?

A common mistake is to build the stablecoin first and ask lawyers to “review it” later. That approach often leads to rework. If the product cannot support required controls, the company may need to redesign smart contracts, onboarding flows, custody processes, and reporting systems.

For a stablecoin software development company, this is where technical judgment matters. Compliance cannot live only in PDFs. It must appear inside workflows, dashboards, smart contracts, admin permissions, transaction limits, and audit logs.

MiCA Stablecoin Regulations in the European Union

The EU’s MiCA regulation gives businesses a clearer but stricter route for crypto-asset activity. For stablecoins, MiCA focuses mainly on asset-referenced tokens and e-money tokens. The European Banking Authority states that issuers of asset-referenced tokens and e-money tokens must hold the relevant authorization to carry out activities in the EU.

This matters for any business planning euro-backed stablecoin development or offering stablecoins to EU users.

Under MiCA stablecoin regulations, the key issues include authorization, disclosures, reserve management, governance, redemption rights, supervision, and reporting. ESMA also describes MiCA as creating uniform EU market rules covering transparency, disclosure, authorization, and supervision for crypto-assets not already covered by existing financial services law.

For founders, MiCA creates a useful lesson: token classification comes first.

Before a team builds smart contracts, it should understand whether the stablecoin may be treated as an e-money token, asset-referenced token, or another type of crypto-asset. That classification can change licensing needs, reserve obligations, marketing language, redemption rules, and operational controls.

If the legal structure is wrong, the product may struggle to secure banking partners, exchange listings, institutional users, or regulatory comfort.

UK, Hong Kong, Singapore, and Other Cross-Border Stablecoin Regulations

The stablecoin regulatory map is no longer U.S. versus EU. Several financial centers are building their own models.

In the UK, the FCA has made stablecoin payments a priority for 2026 and has supported testing through its regulatory sandbox. The FCA has said it wants to support UK-issued stablecoins for faster and more convenient payments while allowing firms to test issuance models safely.

Hong Kong has also moved decisively. Its Stablecoins Ordinance came into operation on August 1, 2025. The Hong Kong Monetary Authority states that issuing fiat-referenced stablecoins is a regulated activity and requires a licence.

Singapore has taken a structured approach through MAS, focusing on regulated single-currency stablecoins and requirements around reserve assets, redemption, capital, and disclosures. This makes Singapore important for businesses looking at Asian payment corridors or institutional settlement models.

Read more – MAS Tokenized Treasury Bills

Cross-border stablecoin regulations must be mapped by activity, not just incorporation.

A company may be registered in one country, hold reserves in another, serve users in a third, and market through global channels. Regulators may look at each of those facts. That is why a serious project needs legal mapping, geofencing decisions, user eligibility controls, and clear rules for where the stablecoin can be offered.

What Businesses Must Get Right Before Launching a Stablecoin?

A stablecoin launch is not just a technical release. It is a financial product entering regulated markets, payment networks, banking relationships, and customer trust cycles. Before development begins, businesses need clear answers on licensing, reserves, redemption, AML/KYC, smart contract controls, and ongoing reporting. Missing any of these areas can delay launch, increase legal exposure, or force expensive rebuilding later.

- Stablecoin Licensing Requirements

Licensing depends on what the company actually does.

An issuer may face one type of requirement. A crypto wallet provider may face another. A custodian, exchange, payment processor, liquidity provider, or merchant gateway may trigger different obligations.

The mistake businesses make is asking, “Do stablecoins need a license?” The better question is, “Which activity is the company performing, in which market, for which users?”

How to fix it: create a jurisdictional activity map. It should list issuer location, customer location, reserve location, redemption access, marketing channels, custody flows, and payment use cases.

- Stablecoin Reserve Compliance

Reserves are the credibility layer of a fiat-backed stablecoin.

A business can have excellent smart contracts and still lose trust if the reserve design is weak. Regulators and institutional partners want to know whether reserves are high-quality, liquid, segregated, reconciled, and available for redemption.

Stablecoin reserve compliance should answer four questions:

- What assets back the token?

- Where are those assets held?

- How often are reserves reconciled against the token supply?

- How can users redeem?

How to fix it: Design reserve operations before launch. Use proper custody arrangements, daily reconciliation, liquidity planning, attestation processes, and clear redemption policies.

- Stablecoin AML KYC Compliance

Stablecoins can move value quickly across wallets, exchanges, payment apps, and DeFi protocols. That makes AML/KYC and sanctions controls a major regulatory concern.

For U.S.-permitted payment stablecoin issuers, the Treasury has proposed rules that would impose AML and sanctions compliance obligations.

A stablecoin AML KYC compliance setup includes:

- Customer identification;

- Business verification;

- Sanctions screening;

- Wallet screening;

- Transaction monitoring;

- Suspicious activity workflows;

- Risk-based limits;

- Audit records.

How to fix it: Do not bolt AML/KYC onto the product after launch. Connect it to onboarding, transfers, redemptions, compliance dashboards, and escalation rules from the beginning.

- Smart Contract Controls

Smart contracts must support the legal and operational reality of the stablecoin.

A stablecoin contract may need minting controls, burning controls, pausing, freezing, role-based permissions, upgrade governance, supply reconciliation, and emergency response procedures.

This does not mean every project should over-centralize control. It means the contract should match the legal model. A regulated payment stablecoin will usually need more administrative and compliance functionality than a simple utility token.

This is where smart contract development becomes a compliance issue. The contract should be secure, auditable, and aligned with the issuer’s responsibilities.

- Reporting and Audit Readiness

Regulated stablecoin products create records every day.

Minting, burning, reserve movement, redemption requests, blocked transactions, high-risk wallet alerts, and admin actions all need to be traceable. If the company cannot explain what happened, when it happened, and who approved it, it will struggle during audits or regulatory reviews.

How to fix it: Build reporting dashboards early. The system should show token supply, reserve balances, redemption status, compliance alerts, user risk levels, and smart contract events.

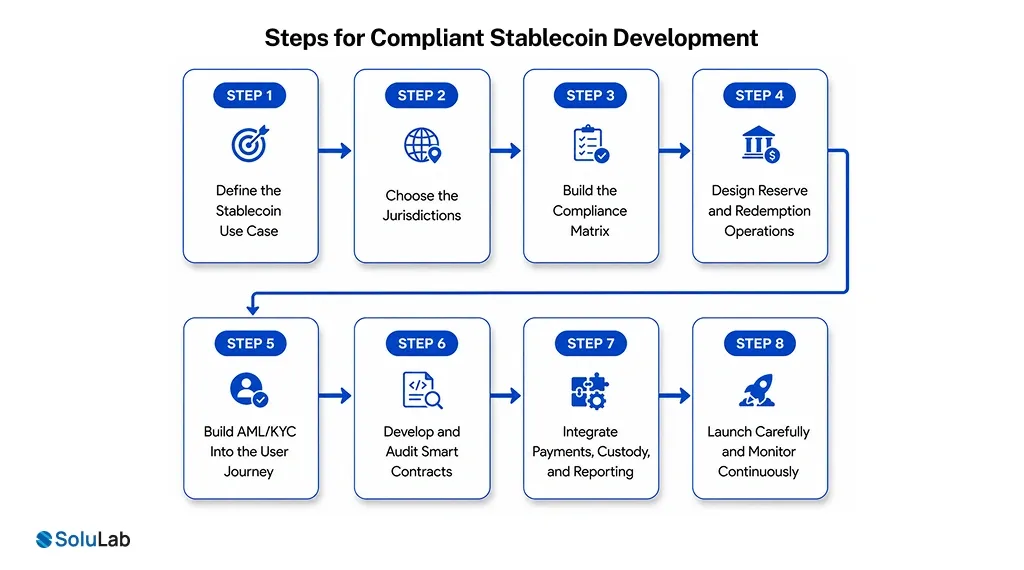

How to Build a Compliant Stablecoin Solution?

Step 1: Define the Stablecoin Use Case

The business should first decide whether the stablecoin is for payments, remittances, treasury operations, exchange liquidity, tokenized finance, merchant settlement, or internal enterprise settlement.

A payment stablecoin faces different expectations from a closed-loop internal settlement token. The use case affects licensing, reserves, user onboarding, transaction monitoring, and integrations.

Step 2: Choose the Jurisdictions

The company should identify where it will issue, market, redeem, and support the stablecoin.

This step often reveals hidden risk. A startup may think it is launching “globally,” but regulated financial products rarely work that way. Each market may require different treatment.

Step 3: Build the Compliance Matrix

A compliance matrix should connect every jurisdiction with licensing, reserve, redemption, AML/KYC, sanctions, custody, consumer protection, data, tax, and reporting requirements.

This matrix becomes the working document for legal, product, engineering, treasury, and compliance teams.

Step 4: Design Reserve and Redemption Operations

Reserve operations should not be left to the finance team alone. Product teams need to know when minting is allowed, when burning happens, how redemption requests flow, what happens during liquidity stress, and how reserve proof is generated.

Strong reserve planning supports regulated stablecoin solutions and reduces trust problems later.

Step 5: Build AML/KYC Into the User Journey

KYC should not feel like a random gate added after the product is finished.

The company should define user tiers, business verification rules, transaction limits, sanctions checks, wallet screening logic, and escalation paths before launch.

This is especially important for enterprise stablecoin as a service solutions, where clients may expect KYB, role-based permissions, approval workflows, and transaction records.

Step 6: Develop and Audit Smart Contracts

The smart contract layer should match the compliance model.

A reliable stablecoin development company should help design minting, burning, pausing, freezing, permissions, upgradeability, event logging, and supply controls. Independent security audits should happen before mainnet deployment.

Step 7: Integrate Payments, Custody, and Reporting

The stablecoin becomes useful only when it connects to business systems. This may include wallets, custodians, exchanges, payment gateways, banking partners, ERP systems, reconciliation systems, compliance tools, and merchant platforms.

This is where crypto payment gateway development, blockchain compliance solutions, and enterprise API design become important.

Step 8: Launch Carefully and Monitor Continuously

Businesses can begin with limited users, transaction caps, approved corridors, redemption testing, live monitoring, and compliance reviews. After the product proves stability, the company can expand.

Compliant vs Weak Stablecoin Development: Understanding The Difference

| Area | Compliant Stablecoin Development | Weak Stablecoin Development |

| Legal planning | Starts with jurisdiction mapping and issuer classification. | Starts with the token launch and legal review later. |

| Reserves | Uses liquid, segregated reserves with reconciliation and attestations. | Uses vague backing claims or unclear custody. |

| AML/KYC | Includes onboarding, screening, monitoring, and escalation workflows. | Adds basic checks after users are already active. |

| Smart contracts | Supports controlled minting, burning, pausing, freezing, and audit logs. | Uses generic token contracts with limited governance. |

| Reporting | Gives teams visibility into reserves, supply, redemptions, and compliance actions. | Relies on manual spreadsheets and incomplete records. |

| Enterprise trust | Easier for banks, auditors, investors, and partners to review. | Creates delays during due diligence. |

| Scaling | Built for multi-market growth. | Requires costly rebuilds when entering regulated markets. |

Common Mistakes in Stablecoin Legal Compliance

Mistake 1: Overusing “Fully Backed” Without Operational Proof

Many teams use reserve language too casually. If the company says the token is fully backed, it must be able to prove backing through reserve assets, custody records, reconciliation, and redemption processes.

How to fix it: Align marketing claims with actual reserve operations. Do not let sales language get ahead of treasury controls.

Mistake 2: Treating Compliance as a Legal Department Problem

Compliance affects engineering, onboarding, finance, support, treasury, risk, and management.

How to fix it: Create shared ownership. Product and engineering teams should understand the compliance logic they are building, not just receive vague legal requirements.

Mistake 3: Ignoring Secondary Market Movement

A stablecoin can move beyond the original customer base. It may reach crypto exchanges, wallets, DeFi protocols, and users that the issuer never directly onboarded.

How to fix it: Build wallet monitoring, risk scoring, sanctions screening, and policy rules for high-risk movement.

Mistake 4: Choosing the Wrong Development Partner

Some vendors can build tokens. Fewer can build a regulated financial infrastructure.

How to fix it: Choose a stablecoin infrastructure company that understands smart contracts, compliance workflows, payment systems, dashboards, audits, and enterprise integrations.

Cost Factors Influence Regulated Stablecoin Development

The cost of a stablecoin project depends on more than smart contract development.

A regulated product may require legal opinions, licensing support, smart contract engineering, smart contract audits, AML/KYC integrations, custody setup, reserve reporting, payment APIs, dashboards, testing, documentation, and post-launch monitoring.

The cheapest build is rarely the cheapest path. A low-cost token launch can become expensive if the company later needs to rebuild permissions, add compliance controls, migrate contracts, redesign onboarding, or satisfy enterprise due diligence.

For decision-makers, the better question is not “How much does stablecoin development cost?” It is “What level of trust does this stablecoin need to earn?”

A closed pilot has one cost profile. A public payment stablecoin has another. A cross-border enterprise settlement product needs stronger controls, documentation, and operational resilience.

Platform Features Every Enterprise Stablecoin Should Have

A reliable stablecoin platform should include:

Issuance and Redemption Layer

This layer manages minting, burning, redemption requests, supply controls, and reserve alignment. It should connect technical supply with treasury operations.

Compliance Layer

This layer handles KYC, KYB, sanctions screening, wallet risk checks, transaction monitoring, and suspicious activity workflows.

Smart Contract Governance Layer

This layer controls roles, permissions, upgrades, pauses, freezes, and admin actions. It should be secure enough for institutional review.

Payment and Integration Layer

This layer connects the stablecoin with wallets, custodians, exchanges, payment gateways, merchant tools, and enterprise systems.

Reporting Layer

This layer gives teams real-time visibility into supply, reserves, redemptions, compliance actions, and transaction behavior.

These features separate a serious stablecoin development company from a basic token vendor.

How to Choose the Top Stablecoin Development Company?

A business should not choose a provider only because it can deploy a token quickly.

The top stablecoin development company should ask difficult questions before writing code. Which jurisdictions matter? Who is the issuer? What backs the token? Who can redeem? What compliance tools are required? Which admin controls are acceptable? What reporting will auditors need?

A strong provider should bring together:

- stablecoin consulting services for planning and feasibility;

- smart contract expertise for secure token logic;

- compliance architecture for AML/KYC and sanctions workflows;

- payment integration experience;

- dashboard and reporting capabilities;

- enterprise documentation support.

Turn Stablecoin Strategy into a market-ready product with legal clarity, secure contracts, reserve logic, compliance workflows, and enterprise integrations.

Conclusion

Global stablecoin regulations are forcing the market to mature. The next wave of stablecoin adoption will be won by companies that can answer hard questions from regulators, banks, auditors, investors, and enterprise customers.

For any business planning a stablecoin in 2026, the path is clear: start with regulation, design around compliance, build secure infrastructure, and choose a blockchain development partner that understands both technology and financial product discipline.

Build a Compliant Stablecoin with SoluLab!

At SoluLab, a stablecoin payment platform development company, we help you turn your stablecoin idea into a secure, scalable, and compliance-ready product. Our team supports you with stablecoin architecture, smart contract development, AML/KYC integration, reserve workflow planning, wallet integration, payment features, and enterprise-grade dashboards.

We focus on building solutions that are practical for real business use, not just technical demos. Whether you want to launch a fiat-backed stablecoin, build enterprise payment infrastructure, or explore regulated digital asset products, we help you move with clarity and confidence.

FAQs

Shipra Garg is a tech-focused content strategist and copywriter specializing in Web3, blockchain, and artificial intelligence. She has worked with startups and enterprise teams to craft high-conversion content that bridges deep tech with business impact. Her work translates complex innovations into clear, credible, and engaging narratives that drive growth and build trust in emerging tech markets.