Key Takeaways

- Automated compliance via ERC-3643 and DID protocols reduces SPV administrative overhead by 75%.

- Atomic T+0 settlement removes the 2% liquidity premium, turning illiquid private debt into a high-velocity asset.

- Lenders historically suffer from “delayed data” (quarterly reports), leading to sudden defaults.

- Real-time Chainlink oracles connect smart contracts to borrower ERP systems, triggering proactive risk mitigation and reducing Loss Given Default (LGD) by 20%.

Since 2008, there has been a steady move away from traditional bank lending toward private markets. Today, capital is increasingly coming from distributed investors rather than centralized institutions. Direct lending alone has grown nearly 17x since 2009, while loans as a share of bank assets have dropped from 70% to 55%.

At the same time, the rise of Private Credit Tokenization 2026 and the growing demand for asset tokenization development are transforming how loans are created, funded, managed, and traded. This leads to the tokenized private credit to a $14 billion market volume.

So what happens when a high-velocity private credit tokenization service comes into the picture? Already finance industry systems are enabling near-instant loan issuance, continuous monitoring, and active secondary markets.

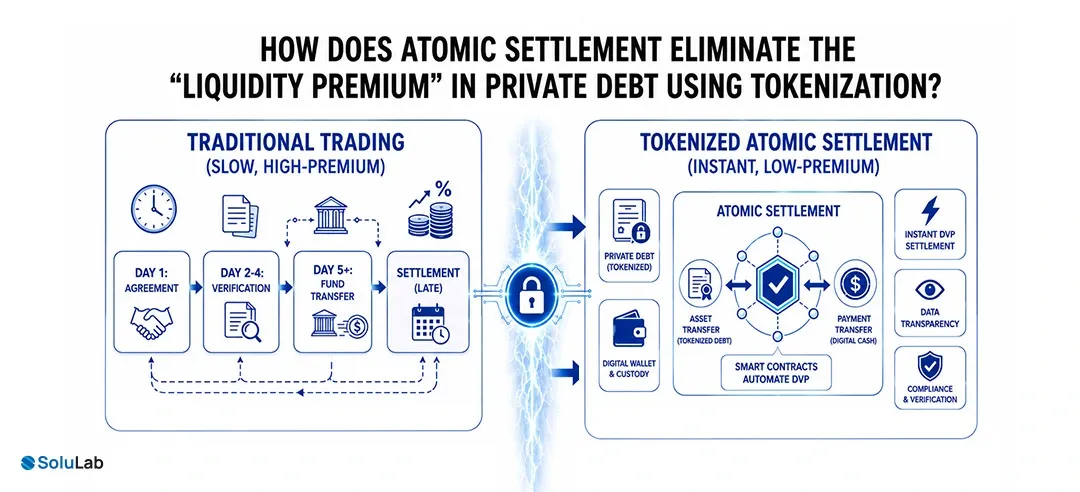

How Does Atomic Settlement Eliminate the “Liquidity Premium” in Private Debt Using Tokenization Services?

Private credit has always required investors to lock their capital for long periods. Because of this, lenders demanded an additional return, known as the liquidity premium.

However, with private credit on blockchain, this assumption is starting to break.

What actually changes with atomic settlement?

Atomic settlement ensures that the exchange of the loan and payment happens at the same time.

- Traditional model: T+2 settlement

- Tokenized model: T+0 settlement

There is no delay, no counterparty risk, and no capital stuck in transit.

Why does this remove the liquidity premium?

Because capital is no longer locked. Investors can redeploy funds immediately after settlement.

- Faster capital reuse

- Lower settlement risk

- Reduced dependency on intermediaries

Therefore, the extra 1–2% yield traditionally required in private debt is now being compressed.

What enables this speed?

Stablecoin rails such as USDC and institutional systems like JPM Coin are widely used across tokenized private credit platforms. These allow instant settlement without relying on legacy banking infrastructure.

Why does this matter for the market?

The tokenized asset market is projected to reach between $4 trillion and $16 trillion by 2030. Yet private credit volume is less than 1% of the broader $1.7 trillion market.

However, private credit was historically illiquid… tokenized private credit lifecycle models now allow loans to behave more like tradable assets.

This shift improves capital efficiency across the entire blockchain lending universe.

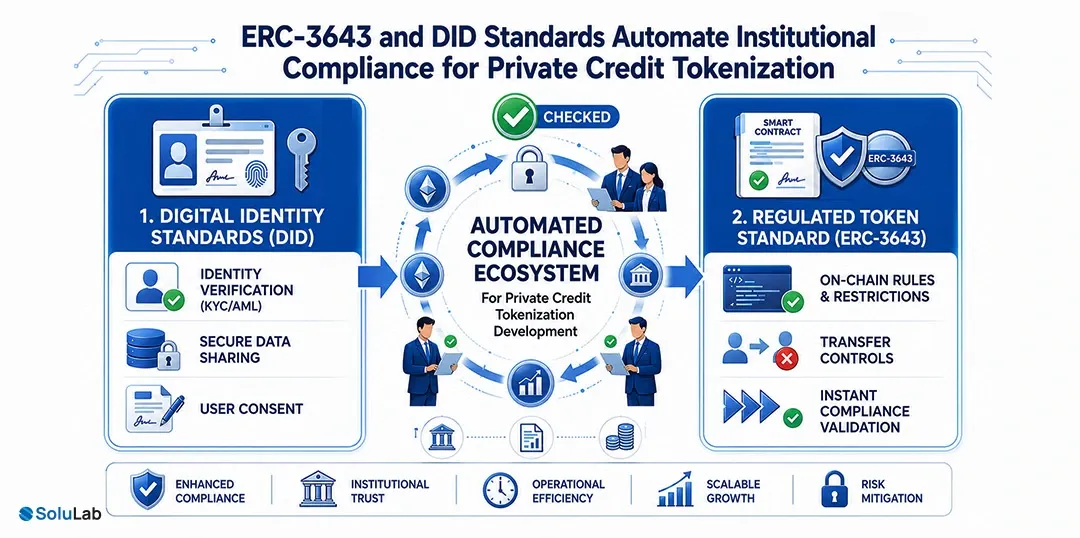

Can ERC-3643 and DID Standards Automate Institutional Compliance for Private Credit Tokenization Platform Development?

Compliance has always been one of the biggest barriers in private credit. Onboarding investors, verifying identity, and ensuring regulatory checks can take weeks.

But what if compliance could be embedded directly into the asset itself?

How does ERC-3643 change RWA token compliance?

ERC-3643, also known as the regulated RWA token standard, allows compliance rules to be coded into the token.

- Transfers fail if KYC is not completed

- Only eligible investors can hold the asset

- Regulatory rules are enforced automatically

This removes manual intervention and reduces operational delays.

What role do Decentralized Identifiers (DID) play?

Decentralized Identifiers enable reusable identity verification. Once verified, an investor can interact across multiple tokenized lending platforms for private credit without repeating KYC.

- Faster onboarding

- Lower compliance costs

- Better user experience

A supplier mints an invoice as an ERC-3643 token. Additionally, enterprises can now also convert accounts receivable (unpaid invoices) into digital tokens.

- Using Chainlink Functions, the platform verifies the invoice against the buyer’s ERP system (e.g., SAP).

- Global liquidity pools (on platforms like Centrifuge) can fund these invoices instantly.

- This allows SMEs to access capital from European or Asian investors without navigating traditional cross-border banking delays.

Why is this important right now?

91% of institutional investors are already interested in tokenized products, and 97% believe tokenization will reshape asset management. However, regulatory friction still slows adoption.

By combining ERC-3643 and DID, enterprise-grade tokenized credit systems solve this bottleneck and make institutional participation much easier.

How Do Real-Time Covenants and Oracles Prevent Private Credit Defaults?

One of the biggest risks in private credit is delayed information. Lenders often rely on quarterly reports, which means problems are detected too late.

A company tokenizes its future recurring revenue. Smart contracts are linked to the company’s payment gateway (Stripe/PayPal).

So how can lenders respond before a default actually happens?

What powers real-time monitoring?

Oracles such as Chainlink and Pyth connect real-world data to smart contracts. These systems track:

- Revenue performance

- Inventory levels

- Debt-to-equity ratios

What happens when risk thresholds are crossed?

Smart contracts automatically trigger actions:

- Increase interest rates based on risk

- Pause further loan drawdowns

- Notify lenders or AI agents

What impact does this create?

- Faster risk detection

- Reduced default probability

- Better credit discipline

Data suggests that continuous monitoring can reduce Loss Given Default (LGD) by 15–20%.

Why does this matter for modern lending?

While traditional systems depend on delayed updates, real-time private credit tokenization solutions allow continuous visibility. This makes lending more predictable and secure for both borrowers and investors.

Additionally, DeFi lending platforms are increasingly using permissioned, gated vaults to ensure compliance while utilizing blockchain efficiency, addressing regulatory hurdles for traditional institutional players.

Read more – Commodity Tokenization

What Is the True ROI of Tokenizing Private Credit Development via SPV Structures?

Special Purpose Vehicles (SPVs) are still used to structure private credit deals. However, tokenization has significantly improved how these structures operate.

What changes in a tokenized SPV?

| Metric | Traditional SPV | Tokenized SPV (2026) |

| Admin Costs | 1.5% – 2.5% AUM | < 0.5% AUM |

| Onboarding Time | 2–4 weeks | < 5 minutes |

| Minimum Investment | $1,000,000+ | ~$10,000 |

| Reporting | Quarterly PDFs | Real-time dashboards |

Where does the ROI actually come from?

- Lower administrative overhead

- Faster capital deployment

- Reduced intermediaries

- Increased investor participation

Additionally, individuals control over half of the world’s $290 trillion wealth, yet only 5% is allocated to alternative investments. Tokenization could push this closer to 20%, unlocking trillions in new capital.

Why are private credit funds leading adoption?

Private credit already represents about 65% of the tokenized RWA market. Fund managers are prioritizing this segment because it suffers the most from illiquidity and inefficiency.

This makes tokenizing private credit one of the most practical applications within real-world asset tokenization today.

Can Secondary Markets for Private Credit Tokenization Services Finally Reach Scale in 2026?

Several structural shifts are happening currently:

- Private credit is replacing traditional bank lending

- Tokenization is improving access and efficiency

- Institutional adoption is accelerating

Jurisdictions like Singapore, Dubai (ADGM), and the EU are emerging as key hubs due to clear regulations.

- These regions are enabling large-scale adoption of tokenized lending solution providers and compliant digital asset frameworks.

- Technologies such as MPC custody, zero-knowledge proofs, and smart contracts are making these systems secure and scalable.

- Additionally, AI in loan underwriting is improving decision-making, allowing lenders to assess risk faster and more accurately.

Intra-Day Repo Markets for Corporate Treasuries

Large enterprises often have millions in “idle” cash or high-quality bonds.

- Using tokenized private debt as collateral, corporate treasurers can engage in Intra-day Repos.

- As a result, they can borrow or lend cash for just a few hours to meet specific liquidity needs, then settle “atomically” before the business day ends.

- This is currently being pioneered by the Canton Network and JPMorgan’s Kinexys.

The idea of a 60-second loan is no longer theoretical. It is already being executed across advanced custom private credit tokenization platforms.

Loans today can be:

- Issued instantly

- Monitored continuously

- Traded anytime

While the market is still in its early stages, the direction is clear. As infrastructure improves and regulations mature, tokenized private credit will become a standard part of financial systems.

The shift is gradual, but the impact is significant.

Conclusion

As we reach the end of this discussion, it’s clear that private credit is moving toward faster, more accessible systems powered by tokenization. It’s high time to partner with a private credit tokenization development company to improve liquidity, automate compliance, and enable real-time lending.

To make this 60-second loan approval, SoluLab, a tokenization platform development expert, can help by building custom platforms that support high-velocity lending, smart contract automation, and scalable tokenized ecosystems.

Our experts build enhanced tokenization platforms along with digital credit services. As adoption grows, businesses that invest early in these systems will be better positioned to operate in a more efficient and digitally connected credit market.

Contact us today and live your fast banking solutions!

FAQs

Deepika is a content writer who blends storytelling with strategic thinking. She explores topics across digital innovation, emerging tech, and the evolving blockchain industry. She enjoys breaking down complex ideas into simple, engaging narratives in the growing global markets.