Key Takeaways

- Fraud in 2026 is adaptive, distributed, and often invisible

- AI shifts fraud detection from rule-based to behavior-driven

- Modern systems rely on layered architectures, not single models

- Generative AI is both increasing fraud sophistication and improving defense

- Visualization helps translate AI signals into actionable insights

- Compliance requires hybrid models combining AI, rules, and human oversight

- Most institutions are adopting hybrid build-buy approaches

- The real goal is not eliminating fraud, but building fraud-resilient systems

There was a time when fraud left a trace you could follow. A suspicious transaction. A mismatched signature. A pattern that, if you looked closely enough, gave itself away.

That time is gone.

In 2026, fraud doesn’t behave like an event. It behaves like a system. It learns, adapts, and blends into normal activity so seamlessly that the line between legitimate and malicious is no longer obvious. And that’s what makes it dangerous.

Banks and fintech platforms are now dealing with something fundamentally different. Not just more fraud, but smarter fraud. The kind that evolves faster than rules, faster than manual reviews, and sometimes even faster than traditional machine learning models.

This is where AI in fraud detection starts to matter more deeply. Not as a tool layered on top, but as a core capability that continuously interprets intent, not just actions.

Because the real shift isn’t about detecting fraud anymore. It’s about understanding behavior before it turns into fraud.

The New Shape of Financial Crime

If you zoom out and look at the current landscape, what stands out is not just the volume of fraud, but how distributed it has become.

Fraud no longer happens at a single touchpoint. It stretches across onboarding, authentication, transactions, and even customer support interactions.

- A synthetic identity might pass onboarding.

- A bot-driven pattern might mimic normal user behavior.

- A deepfake voice could authorize a transaction.

Each step looks harmless in isolation. Together, they form a coordinated attack.

This is the reality shaping AI fraud detection in banking today.

What’s driving this shift?

- Instant payments that remove buffers for verification

- Embedded finance is expanding access points across platforms

- Cross-border transactions that blur jurisdictional visibility

- AI-powered cybercrime that automates deception at scale

The result is a system where fraud doesn’t need to break rules. It just needs to blend in.

And that’s exactly why traditional detection approaches struggle. They were designed to catch outliers. But modern fraud often looks… normal.

This is where the role of AI in preventing financial crime becomes critical. It doesn’t just look for what is wrong. It learns what is subtly different.

How AI Actually Changes Fraud Detection?

A lot gets said about AI in this space, but the real shift is quieter and more structural.

It’s not just about better models.

It’s about changing how decisions are made.

Traditional systems operate on predefined logic. If something crosses a threshold, it gets flagged. Simple, but rigid.

Artificial Intelligence changes that by introducing context into every decision.

So instead of asking:

“Is this transaction above a limit?”

The system starts asking:

“Does this behavior make sense for this user, in this moment, given everything we know?”

That’s a very different question.

This is how fraud detection using AI in banking begins to evolve:

- Transactions are evaluated alongside behavioral history

- Devices are assessed based on usage patterns, not just IDs

- Relationships between accounts are analyzed, not just individual actions

- Risk becomes dynamic, not fixed

And over time, the system doesn’t just detect fraud.

It learns what normal looks like at a granular level.

That’s the real power behind AI-based fraud detection in banking. It reduces reliance on static rules and replaces it with adaptive intelligence.

But this also introduces a new layer of complexity.

Because when systems start making probabilistic decisions instead of deterministic ones, institutions need to rethink:

- How risk is defined

- How decisions are explained

- How compliance is maintained

And that’s where things start getting interesting.

What Actually Powers AI in Fraud Detection?

When people talk about AI for fraud detection, it often gets reduced to “machine learning models catching anomalies.” That’s only a small part of the picture.

In reality, what powers modern fraud systems is not a single model, but a stack of interacting intelligence layers.

At the foundation, there is pattern recognition. Machine learning models trained on historical data begin to understand what “normal” looks like. But fraud rarely repeats itself in clean patterns anymore. It mutates.

So the system needs to go deeper.

This is where multiple AI approaches start working together:

- Machine Learning picks up deviations from expected behavior

- Deep Learning captures complex, non-linear interactions across massive datasets

- Graph Analytics connects the dots between accounts, devices, IPs, and identities

- Natural Language Processing interprets communication signals like phishing attempts or social engineering patterns

Individually, each of these solves a piece of the problem. Together, they create something more powerful – a system that doesn’t just detect anomalies, but understands relationships and intent.

That’s what makes AI-led development fundamentally different from legacy systems. It moves from surface-level signals to structural intelligence.

And once you reach that level, the next question naturally becomes:

How do you actually put this into production?

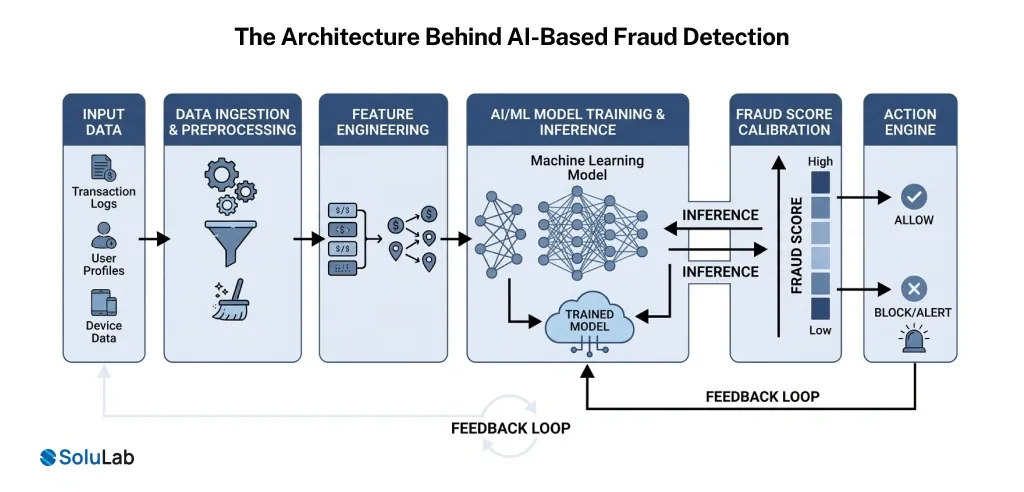

The Architecture Behind AI-Based Fraud Detection

If there’s one place where most fraud detection initiatives succeed or fail, it’s not the model. It’s the architecture.

Because even the best model is useless if it cannot operate in real time, at scale, and across fragmented data sources.

Modern AI fraud detection in banking is built like a streaming intelligence system. Always on, always learning, always evaluating.

At a high level, the flow looks something like this:

- Data flows in continuously from transactions, devices, APIs, and user interactions

- That data is transformed into behavioral signals and contextual features

- Multiple models evaluate risk simultaneously

- A decision engine assigns a dynamic risk score

- Actions are triggered instantly – approve, flag, step-up authentication, or block

- Outcomes feed back into the system to refine future decisions

What’s important here is not just the flow, but the timing.

Fraud detection is no longer a batch process.

It happens in milliseconds.

That means:

- Data pipelines must be low-latency

- Models must be lightweight but accurate

- Decision engines must be explainable in real time

And perhaps most importantly, the system must handle uncertainty.

Because AI doesn’t give binary answers. It gives probabilities.

So instead of saying “this is fraud,” the system says:

“There is a 87% chance this is fraudulent behavior.”

That subtle shift changes everything. It forces institutions to design risk-based decision frameworks, not just detection systems.

The Double-Edged Role of Generative AI

If traditional AI made fraud detection smarter, generative AI in fraud detection is making the entire landscape more unpredictable.

Because for the first time, both attackers and defenders are using the same class of technology.

On one side, fraudsters are leveraging generative AI to:

- Create highly convincing phishing messages at scale

- Generate synthetic identities with realistic behavioral footprints

- Clone voices and faces for authentication bypass

- Automate fraud strategies with minimal human intervention

This is not an incremental change. It’s a step-function increase in sophistication.

But here’s the twist.

The same technology is also becoming one of the strongest defenses.

Financial institutions are starting to use generative AI to:

- Simulate fraud scenarios that have never occurred before

- Stress-test detection systems against unknown attack patterns

- Generate synthetic datasets to train models without exposing real user data

- Assist investigators by summarizing complex fraud cases in seconds

So instead of reacting to fraud, systems begin to anticipate it.

That’s a very different posture.

In this context, AI in cybersecurity for cybercrime prevention becomes less about blocking known threats and more about preparing for unknown ones.

And this is where the conversation starts shifting again from detection to visibility.

Because even the most advanced system is only as effective as its ability to make sense of what it sees.

Seeing Fraud, Not Just Detecting It

At some point, every fraud system hits the same wall.

It starts generating signals faster than humans can interpret them.

Flags, scores, alerts, probabilities. All technically correct.

But without clarity, they create noise instead of insight.

This is where data visualization quietly becomes one of the most critical layers in AI fraud detection in banking.

Because detection without visibility doesn’t scale.

What institutions really need is the ability to see fraud as it unfolds, not as isolated alerts, but as connected behavior.

What Visualization Actually Changes?

Instead of reviewing transactions one by one, analysts begin to see:

- Clusters of accounts behaving in sync

- Devices moving across multiple identities

- Sudden spikes in transaction patterns across geographies

- Hidden relationships that would never appear in tabular data

It turns an investigation from a manual audit into pattern recognition at a glance.

What’s interesting is that visualization doesn’t replace AI.

It complements it.

AI surfaces the signal.

Visualization makes it understandable.

And in high-stakes environments like banking, that distinction matters. Because decisions still need to be justified, audited, and sometimes challenged.

Which brings us to the layer that often slows everything down, but cannot be ignored.

Where AI Meets Compliance Reality?

For all its promise, AI in fraud detection and prevention operates inside one of the most tightly regulated environments in the world.

And that creates tension.

AI systems thrive on flexibility, probabilities, and continuous learning.

Regulators expect clarity, consistency, and explainability.

Bridging that gap is where most real-world implementations either mature… or stall.

The Core Challenges

- Explainability

Why was this transaction flagged?

“Because the model said so” is not an acceptable answer - Bias and fairness

Are certain user groups being flagged more frequently? - Data governance

Where is the data coming from, and how is it being used? - Customer impact

False positives are not just technical errors. They affect trust

What Institutions Are Doing Differently in 2026?

Instead of choosing between rules and AI integration solutions, most systems are becoming layered decision frameworks:

- AI models generate risk probabilities

- Rule engines enforce regulatory thresholds

- Human reviewers handle edge cases

- Audit logs capture every decision path

This hybrid approach allows institutions to move forward with AI-based fraud detection in banking without losing control over compliance.

There’s also a growing emphasis on:

- Explainable AI (XAI) for auditability

- Model governance frameworks for lifecycle management

- Continuous monitoring for drift and bias

Because in regulated environments, deploying AI is not a one-time effort.

It’s an ongoing responsibility.

The Real Decision: Build, Buy, or Evolve

At some point, every bank or fintech faces a practical question.

Not whether to adopt AI.

But how.

And this is where conversations around AI development solutions become more strategic than technical.

The Build Path

Building in-house offers control.

You can design models around your specific fraud patterns, integrate deeply with internal systems, and create long-term differentiation.

But it comes with trade-offs:

- Long development cycles

- High dependency on specialized talent

- Continuous maintenance overhead

For many institutions, this path only works if AI is seen as a core capability, not a supporting function.

The Buy Path

Vendors offer ready-to-deploy platforms with pre-trained models and compliance alignment.

This accelerates time to market significantly.

But over time, limitations start to surface:

- Models may not fully adapt to your unique fraud patterns

- Customization can be constrained

- Strategic dependency on external systems

What’s Actually Happening in 2026

Most institutions are not choosing one over the other.

They are evolving toward a hybrid model:

- External platforms for baseline detection

- Internal AI layers for contextual intelligence

- Custom workflows for decision orchestration

This allows them to move fast without giving up control.

And this is where the role of an experienced AI consulting company becomes less about building models, and more about shaping the system around them.

Firms like SoluLab, for instance, typically approach this as an infrastructure problem first. Aligning data pipelines, compliance layers, and decision frameworks before scaling AI capabilities.

Because in fraud detection, success doesn’t come from having the best model.

It comes from having the most coherent system.

Moving from AI Adoption to Fraud-Resilient Systems

Most institutions don’t struggle with whether to adopt AI.

They struggle with how to operationalize it without breaking what already works.

Because fraud detection systems sit at a sensitive intersection.

They touch customer experience, compliance, and real-time financial decisions all at once.

So the shift to AI in fraud detection cannot be abrupt. It has to be layered.

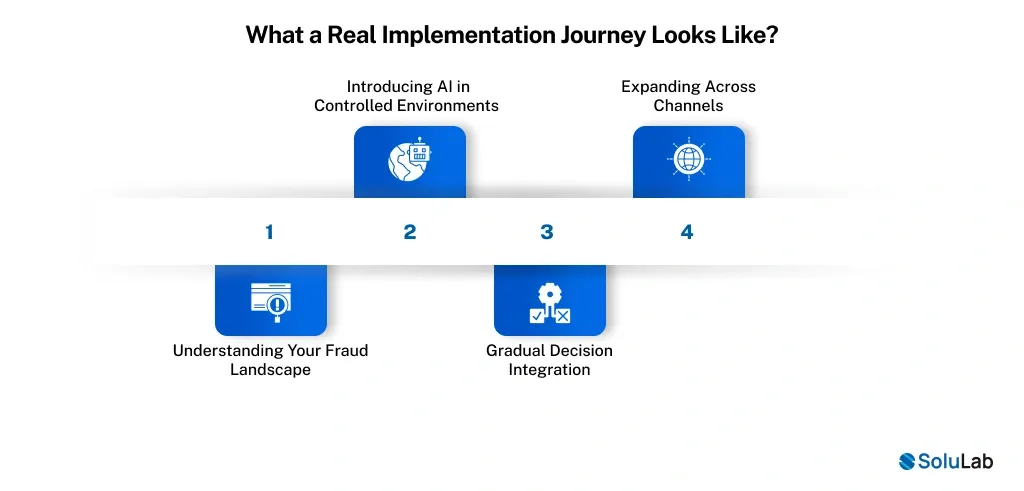

What a Real Implementation Journey Looks Like?

It usually begins with clarity, not code.

Phase 1: Understanding Your Fraud Landscape

Before introducing AI, institutions need to map where fraud actually exists in their system.

Not just transactions, but:

- Onboarding vulnerabilities

- Authentication gaps

- Behavioral inconsistencies

- Channel-specific risks

This stage often reveals that fraud is not concentrated. It’s distributed.

Phase 2: Introducing AI in Controlled Environments

Instead of a full rollout, AI models are deployed in parallel with existing systems. They observe, learn, and generate risk scores without directly impacting decisions.

This creates space to:

- Validate model accuracy

- Understand false positives

- Build internal trust

Phase 3: Gradual Decision Integration

Once confidence builds, AI outputs start influencing decisions. Not replacing rules entirely, but augmenting them.

For example:

- AI flags a transaction → triggers step-up authentication

- High-risk score → additional verification instead of immediate rejection

This keeps the system adaptive without becoming disruptive.

Phase 4: Expanding Across Channels

Fraud rarely stays in one place.

So AI capabilities extend across:

- Payments

- Account access

- Customer support interactions

- Cross-platform behavior

At this stage, AI in payments starts behaving like a unified system, not isolated tools.

Phase 5: Continuous Learning and Optimization

The system begins to refine itself.

- Models retrain on new fraud patterns

- Feedback loops reduce false positives

- Risk scoring becomes more contextual

This is where the system starts feeling less reactive and more predictive.

What’s important here is that the journey is not about deploying AI solutions.

It’s about reshaping how decisions are made across the organization.

Conclusion: The Future Is Not Fraud-Free, It’s Fraud-Aware

There’s a tendency to think of fraud detection as a problem to be solved. But in reality, fraud evolves alongside the systems designed to stop it.

Which means the goal is not elimination.

It’s resilience.

What AI native strategy is enabling in 2026 is not just faster detection, but a different kind of awareness.

- Systems that understand behavior in context.

- That adapt without needing constant reprogramming.

- That anticipate risk instead of reacting to it.

This is the real shift behind AI in fraud detection and prevention.

And the institutions that recognize this early are not just reducing fraud losses.

They are building systems that scale with confidence, even as complexity increases.

Because in a machine-driven financial world, trust is no longer static.

It is continuously computed.

FAQs

Shipra Garg is a tech-focused content strategist and copywriter specializing in Web3, blockchain, and artificial intelligence. She has worked with startups and enterprise teams to craft high-conversion content that bridges deep tech with business impact. Her work translates complex innovations into clear, credible, and engaging narratives that drive growth and build trust in emerging tech markets.