Key Takeaways

- Tokenized private equity is growing faster than the broader asset tokenization market due to institutional adoption and liquidity demand.

- Smart contracts reduce operational overhead in capital calls, reporting, and distribution waterfall management.

- MiCA, SEC guidance, and Singapore’s Project Guardian are creating clearer frameworks for institutional tokenization.

- Private equity firms now use tokenized fund interests and SPVs to improve investor access and secondary trading.

According to industry reports from Research and Markets, the broader asset tokenization market is growing at a nearly 26–30% CAGR. Similarly, the institutional alternatives segment, especially private equity tokenization, is tracking at close to 44% CAGR.

The growth is tied directly to how large private equity firms manage liquidity, investor access, compliance, and fund administration. Instead of waiting years for exits, firms are using private equity tokens to create regulated secondary liquidity.

Banks like JPMorgan and DBS have also started accepting tokenized fund interests as collateral, allowing long-term assets to remain financially productive.

For institutional investors, focus is now on operational efficiency, investor flexibility, and scalable compliance models for private equity investments.

Why 2026 is the Inflection Point for Private Equity Tokenization?

The asset tokenization market environment changed significantly between 2024 and 2026. Earlier conversations around tokenizing private equity were mostly pilot-driven. Today, large institutions are building production-ready frameworks.

According to late-2025 institutional surveys, nearly 76% of firms planned investments into tokenized assets by the end of 2026. The increase is tied to three core developments:

1. Secondary Liquidity for LPs

One of the biggest operational problems in traditional private investment funds is illiquidity. Limited Partners often remain locked into positions for years.

- With private equity asset tokenization, LP interests can be represented digitally and traded on regulated secondary marketplaces.

- This creates controlled liquidity without forcing the fund itself into premature exits.

- For investors managing portfolio allocations, this directly solves the denominator effect problem.

LPs can rebalance exposure without waiting for portfolio companies to reach acquisition or IPO stages.

2. Collateral Utility for Institutional Borrowing

On October 30, 2025, financial institutions, including JPMorgan and DBS, expanded pilot programs in which tokenized fund interests could be used as collateral.

This creates an important advantage for private equity fund managers:

- Long-duration assets remain capital-efficient

- Investors gain access to borrowing flexibility

- Institutional custody becomes easier to manage

- Portfolio leverage can operate within regulated frameworks

JPMorgan also indicated plans involving tokenized real estate, private credit, and hedge fund strategies.

Therefore, this results in other enterprises stepping up the business modules to a new level. This led to blockchain and AI involvement in private equity tokenization services.

3. Administrative Cost Reduction

Mid-sized firms implementing smart contracts for capital calls, reporting, and distribution waterfalls reported operational cost reductions between 20–30%.

The biggest savings came from:

- Investor onboarding automation

- Cap table synchronization

- Compliance verification

- Distribution reconciliation

- Transfer restrictions

For firms managing multiple feeder structures, these efficiencies directly impact fund scalability.

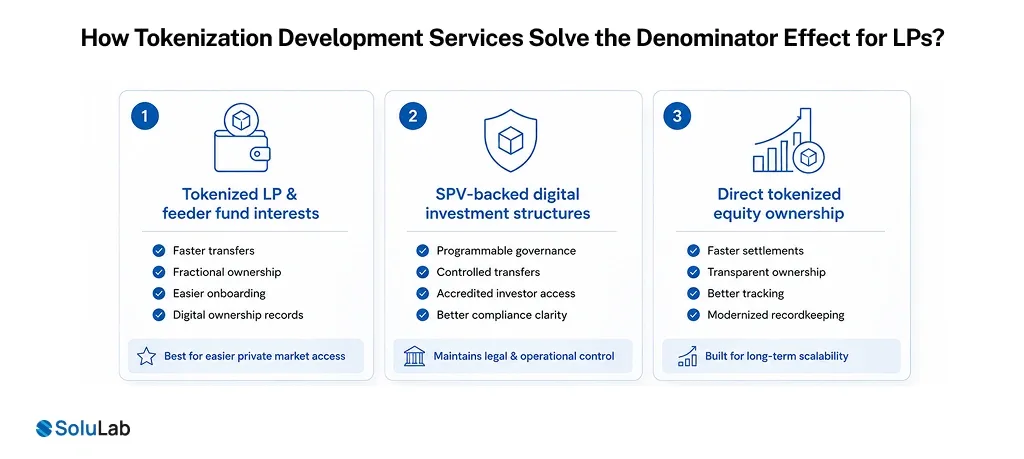

How Tokenization Development Services Solve the Denominator Effect for LPs?

Liquidity has historically remained one of the largest barriers to global private equity assets.

Traditional private markets require investors to lock capital for extended periods. That model creates pressure during economic downturns or portfolio rebalancing cycles.

This is where the private equity tokenization strategy becomes commercially valuable.

1. Tokenized Fund Interests

One of the most practical approaches involves tokenizing LP or feeder fund interests instead of underlying portfolio companies.

This structure helps private equity firms avoid changes to core investment strategies while improving investor flexibility.

Benefits include:

- Faster transferability

- Fractional ownership

- Structured investor onboarding

- Simplified compliance tracking

- Digital ownership records

For many firms, this remains the easiest route toward digitizing private equity.

2. Tokenized SPV Structures

Another common structure involves tokenized Special Purpose Vehicles.

Under this model:

- The SPV holds the underlying exposure

- Investors hold digital tokens linked to that SPV

- Governance rules remain programmable

- Transfer restrictions remain enforceable

This model helps firms maintain legal clarity while expanding access to accredited investors.

3. Direct Equity Tokenization

Some firms also pursue direct tokenization of private equity where tokens map directly to equity or equity-equivalent ownership structures.

This improves:

- Recordkeeping

- Settlement speed

- Transparency

- Ownership tracking

However, it requires deeper coordination with cap table systems and securities compliance frameworks.

A PE Case Study To Understand What Makes Tokenization Services Special in Banking

We all know about Elon Musk buying X (formerly Twitter) for $44 billion. If we look at this transaction through the lens of a CEO in 2026, the friction Musk faced was a liquidity and distribution failure of the old financial guard.

1. The “Toxic Debt” problem: From Bank Anchors to Liquid Fragments

Banks were stuck with $13 billion in debt because institutional investors found it too risky. This is a classic liquidity bottleneck.

The Tokenization Solution: If that $13 billion debt had been issued as tokenized private credit, it wouldn’t have sat on bank balance sheets for two years.

- Secondary Market Velocity: Instead of a few massive banks trying to offload “blocks” of debt, a private equity tokenization platform allows for 24/7 trading of debt fragments.

- Therefore, global secondary investors could have nibbled at the risk in $100k increments, creating a market-clearing price in months, not years.

2. Solving the Denominator Effect for Co-Investors

Musk had $31 billion in equity capital, much of it from co-investors (like Oracle’s Larry Ellison or Prince Alwaleed). In a traditional LBO, these investors are “trapped” until an exit event (IPO or Sale).

The Tokenization Solution: By digitizing private equity interests, these co-investors gain “Programmable Exit Rights.”

- If a co-investor needed liquidity in 2024 when revenues dipped, they could have sold 10% of their private equity tokens on a permissioned exchange without forcing Musk to sell the whole company.

3. Valuation Pivots: Real-Time Collateral Adjustment

The valuation pivot to AI in 2025 was a narrative move to save the debt’s value. In the old world, this valuation is opaque and only checked during rare audit cycles.

The Tokenization Solution: Smart Contracts integrated with Oracles could have linked the token’s value directly to X’s computing infrastructure or xAI’s growth metrics.

- Automated Risk Management: As X transitioned to an AI/Infrastructure model, the security tokens could have automatically adjusted their yield or collateral requirements based on real-time API data from xAI.

Deploying MiCA-Compliant Frameworks for Institutional PE Tokens Development

The regulatory environment changed dramatically from 2025 to 2026. Most developed markets now focus on enabling compliant security token ecosystems instead of restricting them.

1. European Union: MiCA and Electronic Securities Act

The European Union remains one of the strongest jurisdictions for private equity assets for tokenization.

MiCA implementation provided legal clarity for:

- Digital asset custody

- Stablecoin frameworks

- Transfer compliance

- Investor protections

Germany and Luxembourg became major hubs for tokenized fund certificates after amendments to the Electronic Securities Act allowed digital shares without traditional paper certificates.

This reduced operational friction for institutional issuers.

2. United States: GENIUS Act and SEC Guidance

The United States introduced clearer digital securities pathways under the GENIUS Act era.

The SEC also expanded support for regulated transfer frameworks involving accredited investors and permissioned networks.

As a result:

- Institutional blockchains now control nearly 51% market share

- Mainstream brokerages started supporting tokenized interests

- Custodians accelerated digital asset servicing infrastructure

Most institutional implementations still operate on permissioned blockchain networks due to banking compliance requirements.

3. Singapore and Hong Kong: Infrastructure Leaders

Singapore’s MAS standardized Project Guardian frameworks for institutional interoperability.

These models allow tokenized assets to interact with regulated banking systems more efficiently.

The region now leads in:

- Institutional settlement frameworks

- Cross-border interoperability

- Liquidity pool infrastructure

- Collateralized tokenized assets

This is becoming increasingly important for large-scale asset tokenization platforms.

4. UAE and Emerging Markets

Dubai continues positioning itself as a tax-neutral hub for tokenized private credit and alternative assets under VARA regulations.

Kenya also emerged as a notable jurisdiction for infrastructure-focused RWA frameworks.

These regions are attracting global funds looking for operational flexibility in tokenization in finance.

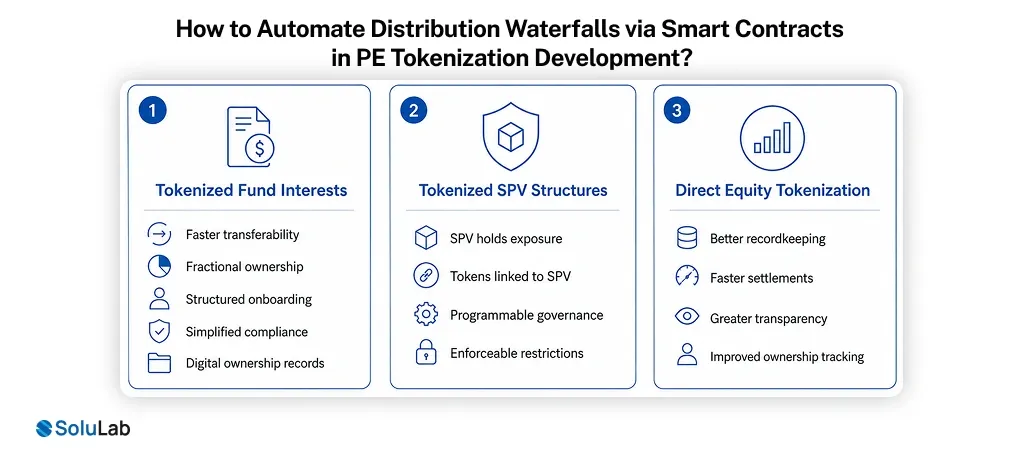

How to Automate Distribution Waterfalls via Smart Contracts in PE Tokenization Development?

One of the strongest operational use cases for private equity tokenization for investors is automation.

Private funds rely heavily on manual coordination across administrators, custodians, auditors, and LPs. This creates delays and reporting inconsistencies.

1. Smart Contract-Based Capital Calls

Traditional capital calls often create short-notice liquidity pressure for investors.

With smart contracts, fund managers can:

- Automate contribution schedules

- Send real-time notifications

- Lock transfers for non-compliant wallets

- Update ownership records instantly

This improves investor visibility significantly.

2. Automated Distribution Waterfalls

Distribution waterfalls can also operate through programmable logic.

This helps automate:

- Preferred return calculations

- Carry allocation

- Investor distributions

- Audit logs

- Payment tracking

For institutional funds, this reduces reconciliation errors and administrative workload.

3. Real-Time Ownership Visibility

A tokenized fund structure creates a synchronized ownership ledger accessible to all approved stakeholders.

This improves:

- NAV reporting

- Investor transparency

- Compliance monitoring

- Audit readiness

The operational advantage becomes even more valuable for funds managing multiple jurisdictions.

Safeguarding RWA Tokenization Against Prime-Brokerage Risks

Institutional investors entering real-world asset (RWA) tokenization markets prioritize security architecture first.

In 2026, the most accepted institutional framework follows a three-pillar security model.

1. Identity and Compliance Controls

Institutional-grade private equity tokenization platform infrastructure now supports wallet-level KYC and AML controls.

Tokens can freeze automatically when transferred to unauthorized wallets.

This protects funds from:

- Non-compliant transfers

- Sanction violations

- Unauthorized secondary activity

2. Oracle Integrity

Tokenized assets require accurate off-chain valuation inputs.

Modern RWA infrastructure connects audited NAV data directly into blockchain systems through secure oracles.

This improves:

- Asset pricing

- Collateral valuation

- Portfolio reporting

- Lending calculations

Without a strong Oracle architecture, institutional adoption becomes difficult.

3. Zero-Knowledge Proof Infrastructure

Zero-Knowledge Proof ZKP frameworks are becoming important for institutional privacy.

These systems allow investors to verify ownership without exposing full portfolio positions publicly.

For institutional participants, this improves confidentiality while maintaining regulatory verification standards.

Conclusion

The commercial value behind private equity tokenization is now tied directly to operational outcomes. For fund managers, asset issuers, and institutional investors, the discussion is now about execution quality:

- Regulatory compliance

- Secondary liquidity

- Smart contract automation

- Custody integration

- Institutional-grade security

To get all this ready in a shorter amount of time and be part of 44% CGAR, you need an experienced tokenization development company to support. Therefore, companies like SoluLab always provide deep technical and customized token solutions. Contact us now and design the private equity tokenization platform.

FAQs

Deepika is a content writer who blends storytelling with strategic thinking. She explores topics across digital innovation, emerging tech, and the evolving blockchain industry. She enjoys breaking down complex ideas into simple, engaging narratives in the growing global markets.