Key Takeaways

- Problem: Institutions want DeFi lending, but anonymous wallets, weak controls, and compliance risks make open protocols difficult to trust fully today.

- Solution: A permissioned DeFi lending platform verifies users, whitelists wallets, automates lending, and keeps institutional transactions compliant, transparent, secure, and auditable.

- What SoluLab Offers: SoluLab builds enterprise DeFi lending solutions with smart contracts, KYC workflows, compliance dashboards, wallet integration, and scalable architecture for businesses.

Institutional capital does not move only because a technology looks new. It moves when the market has security, compliance, operational control, liquidity, and a clear business case. That is exactly why permissioned DeFi lending platform development is gaining attention among banks, asset managers, fintech companies, private credit firms, and enterprise lenders.

Traditional DeFi opened the door to automated lending and borrowing through smart contracts. But for institutions, open access also created a serious problem: anonymous wallets, unclear counterparties, weak compliance controls, and regulatory uncertainty.

Permissioned DeFi, as DeFi applications can add access controls and identity verification directly into smart contract architecture, allowing only verified participants to interact with the protocol. This guide explores why institutions are choosing permissioned DeFi lending platforms over traditional ones.

What is Permissioned DeFi Lending?

It is a blockchain-based lending model where only approved users can participate. Unlike permissionless DeFi, where anyone with a crypto wallet can enter a lending pool, permissioned lending requires identity checks, compliance screening, and platform-level access control.

With KYC-compliant DeFi lending, institutions can use blockchain-based lending without giving up the controls they need. They can lend, borrow, manage collateral, settle faster, and access digital credit markets inside a controlled environment.

Permissioned DeFi can support more verifiable financial transactions and may reduce average cross-border transaction costs by 60%–80% in their proposed model. This model makes sense for regulated institutions because they cannot lend to unknown wallets. They need to know who the borrower is, where funds come from, whether the counterparty is sanctioned, and whether the transaction meets internal risk rules.

That is why permissioned DeFi lending platforms are becoming the safer middle path between open DeFi and traditional finance.

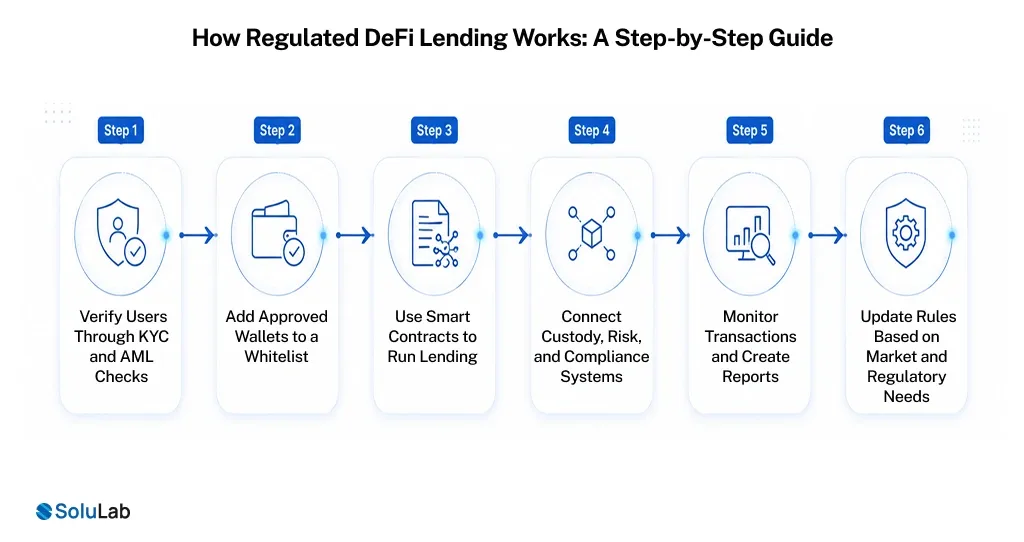

How Regulated DeFi Lending Works: A Step-by-Step Guide

A permissioned DeFi lending platform works by combining blockchain automation with institutional-grade identity checks, risk controls, and compliance workflows. Each step helps enterprises create a safer and more controlled lending environment.

Step 1: Verify Users Through KYC and AML Checks

The platform must use blockchain-powered KYC and AML checks for participant verification. This helps to confirm user identity and risks associated with it and prevent suspicious activity before anyone accesses the platform. KYC-compliant deFi lending is highly suitable for banks, fintech firms, credit platforms, and enterprise investors.

Step 2: Add Approved Wallets to a Whitelist

After KYC and AML verification, approved users are added to a wallet whitelist and get access to execute transactions. This keeps unknown users out of the lending pool and gives institutions better platform access.

Step 3: Use Smart Contracts to Run Lending

Smart contracts handle the lending rules by eliminating the manual work and keeping every action visible on-chain. For enterprises, smart contracts make the secure DeFi lending process faster and more secure.

Step 4: Connect Custody, Risk, and Compliance Systems

A compliant DeFi lending platform should connect with custody providers, identity tools, risk engines, analytics systems, and compliance dashboards. These integrations help institutions protect assets, review borrower activity, and track platform health. For businesses building enterprise DeFi lending solutions, this layer makes the DeFi platforms more reliable for legal, finance, and risk teams.

Step 5: Monitor Transactions and Create Reports

Admins track transactions, lending pool activity, collateral status, repayments, defaults, and suspicious behavior. They also create audit-ready reports for regulators, investors, auditors, and internal teams. This reporting layer supports DeFi lending compliance solutions and gives institutions the visibility they need before deploying serious capital into blockchain lending.

Step 6: Update Rules Based on Market and Regulatory Needs

Platform teams can update rules depending on the market trends and regulatory requirements. One pool can act as a verified enterprise, and another can allow for only qualified investors from approved regions. This ensures the speed, transparency, and automation of blockchain lending.

Why Compliance Must Be Built Into the Permissioned DeFi Lending Platform?

For institutional lending, compliance cannot be added after DeFi development. It must be part of the platform architecture from day one.

- DeFi lending compliance solutions help businesses manage KYC, AML, wallet whitelisting, access control, reporting, and risk monitoring in one secure system.

- A compliant DeFi lending platform gives institutions confidence because every lender, borrower, and liquidity provider is verified before entering the ecosystem.

- Built-in compliance also supports audit trails, transaction monitoring, jurisdiction-based rules, and investor eligibility checks.

- This is why enterprises prefer permissioned DeFi lending platforms over anonymous DeFi models. They get blockchain speed, smart contract automation, and better regulatory control together.

Unlike open DeFi, only approved users can interact with the lending pools. Here is how permissioned DeFi ensures compliance with KYC and AML.

- The platform verifies users through KYC-compliant DeFi lending workflows.

- AML screening checks suspicious activities, sanctioned entities, and risky fund flows.

- Approved crypto wallets are whitelisted, so only verified participants can borrow, lend, supply liquidity, or claim returns.

- Smart contracts apply transaction limits, collateral rules, credit limits, user permissions, and repayment terms automatically.

- Admins can restrict access by geography, investor type, borrower category, risk level, or asset class.

- Real-time dashboards help institutions monitor activity, generate reports, and maintain compliance records.

This is why secure DeFi lending for enterprises works better in a permissioned model. It reduces counterparty risk while keeping the core benefits of blockchain lending, including transparency, automation, faster settlement, and programmable finance.

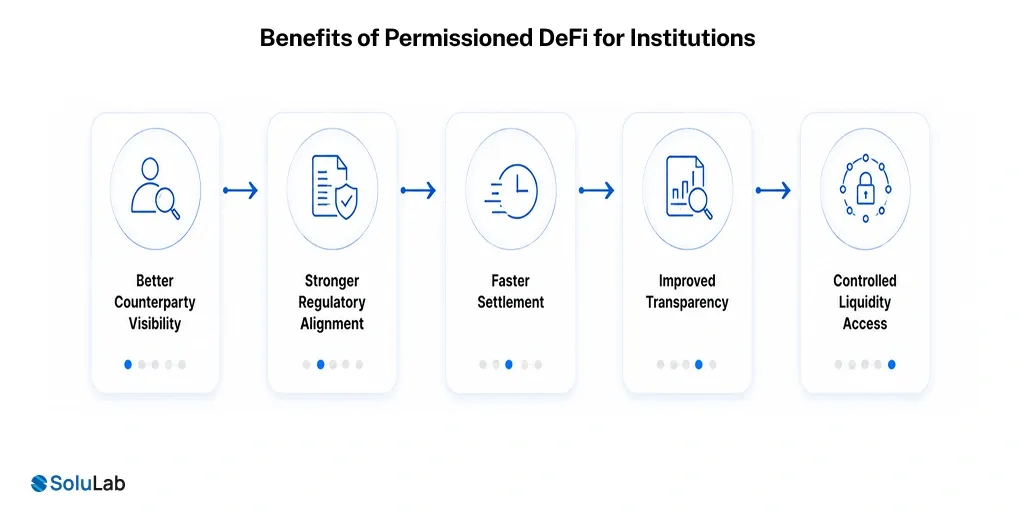

Benefits of Permissioned DeFi for Institutions

The benefits of permissioned DeFi for institutions go beyond compliance. A well-built platform can improve capital movement, transparency, settlement, reporting, and lending efficiency.

- Better Counterparty Visibility

Institutions know who they are dealing with. This helps credit teams, compliance teams, and treasury teams manage risk better.

- Stronger Regulatory Alignment

A KYC-compliant DeFi lending model helps platforms follow identity verification, AML, sanctions, and investor eligibility requirements.

- Faster Settlement

Smart contract development can automate lending, borrowing, collateral movement, repayments, and liquidation logic without slow manual processing.

- Improved Transparency

On-chain records give institutions a clearer view of transactions, balances, collateral positions, and pool activity.

- Controlled Liquidity Access

Businesses can create lending pools for selected institutions, verified investors, corporate borrowers, or approved liquidity providers.

These are some benefits of permissioned DeFi for institutions that unlock blockchain efficiency without unnecessary regulatory exposure.

Why Enterprises Choose Permissioned Blockchain Lending?

Permissioned blockchain lending comes down to control. Enterprises do not want a lending system where anyone can enter, borrow, and exit without identity checks. They want automation, but they also want governance. A permissioned model gives them both.

For example, a fintech company can build a lending pool for verified SME borrowers. A private credit platform can tokenize loan exposure and allow only qualified investors to participate. A bank can use blockchain technology for collateralized lending while keeping internal compliance rules intact.

Enterprises want blockchain lending, but they want it in a form that legal teams, compliance officers, and institutional clients can actually approve.

Institutional DeFi Lending Use Cases

Several institutional DeFi lending use cases make strong business sense.

- Private Credit Lending

Tokenized private credit is becoming a major institutional blockchain category. Chainlink explains that tokenized private credit represents off-chain debt assets, such as corporate loans or real estate debt, as digital tokens on blockchain, improving liquidity, transparency, and operational efficiency.

- SME and Business Lending

A platform can connect verified businesses with institutional liquidity providers. Smart contracts can manage repayment schedules, collateral, and lender returns.

- Real-World Asset Lending

Tokenized real estate, invoices, commodities, bonds, or receivables can be used as collateral inside permissioned lending pools.

- Treasury and Liquidity Management

Enterprises can use permissioned lending infrastructure to optimize idle capital, short-term borrowing, and treasury operations.

- Cross-Border Institutional Lending

Permissioned DeFi can support faster, more transparent lending between verified entities across markets.

What Makes a Secure DeFi Lending Platform for Enterprises?

A platform built for institutional users must feel reliable from the first screen itself. It cannot look like a crypto experiment.

A secure DeFi lending for enterprises product should include:

- KYC and AML verification

- Wallet whitelisting

- Smart contract audits

- Role-based access control

- Institutional-grade custody integration

- Collateral management

- Real-time risk monitoring

- Lending pool configuration

- Automated interest calculation

- Liquidation rules

- Admin dashboards

- Reporting and audit trails

- Multi-chain or private blockchain support

Security is not only about smart contracts. It also includes business logic, identity management, access permissions, custody setup, Oracle reliability, and user operations.

Why Businesses Build a White Label Permissioned DeFi Platform?

Not every company wants to start from zero. Many fintechs, credit platforms, and blockchain startups prefer a white-label permissioned DeFi platform because it can reduce development time and cost.

A white-label model gives businesses the base infrastructure for lending, borrowing, wallet integration, user onboarding, admin control, and compliance workflows. The company can then customize branding, lending rules, token standards, collateral assets, and revenue models. This is useful for:

- Fintech lenders

- Crypto lending startups

- Private credit platforms

- RWA tokenization companies

- Enterprise blockchain firms

- Banks exploring DeFi products

- Investment platforms

- Lending marketplaces

For fast-moving businesses, a white-label model can help test the market faster while still keeping room for customization.

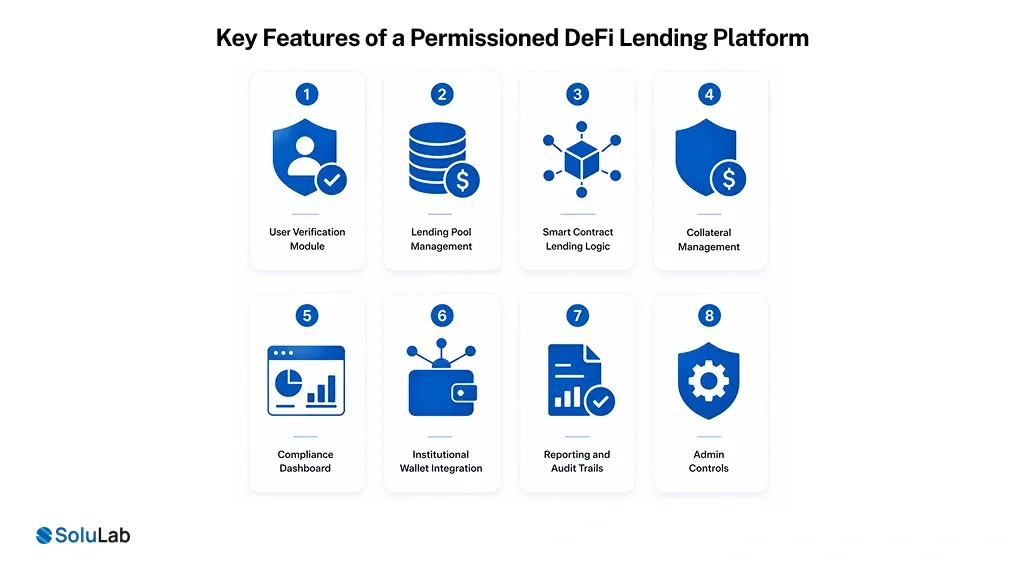

Key Features of a Permissioned DeFi Lending Platform

A business-ready permissioned DeFi lending platform should include features that satisfy users, compliance teams, and platform owners.

User Verification Module

This handles KYC, AML, sanctions screening, and wallet approval.

Lending Pool Management

Admins can create pools based on asset type, borrower category, risk level, interest model, and investor eligibility.

Smart Contract Lending Logic

Smart contracts automate deposits, borrowing, repayments, rewards, collateral checks, and liquidations.

Collateral Management

The platform should support crypto collateral, tokenized assets, stablecoins, RWAs, or approved enterprise assets.

Compliance Dashboard

Teams can monitor user status, transactions, risk flags, jurisdiction rules, and reporting data.

Institutional Wallet Integration

Custodial, non-custodial, and MPC wallet support helps enterprises manage assets securely.

Reporting and Audit Trails

Institutions need clean records for internal audits, regulators, investors, and financial reporting.

Admin Controls

Platform owners need control over users, pools, interest rates, approvals, limits, and emergency actions.

Revenue Models for Permissioned DeFi Lending Platforms

A permissioned lending platform can generate revenue in multiple ways.

The business can charge origination fees, lending pool management fees, transaction fees, withdrawal fees, performance fees, subscription fees, white-label licensing fees, or enterprise onboarding fees.

For a white-label permissioned DeFi platform, the company may also charge setup fees, monthly platform maintenance, compliance module fees, API integration costs, and custom blockchain development charges.

The best model depends on the target customer. A private credit platform may prefer management fees. A fintech lending marketplace may prefer transaction fees. A bank-grade platform may prefer licensing and enterprise support.

Future of Permissioned DeFi Lending

The future of DeFi lending will not be only permissionless or only centralized. The more realistic future is hybrid. Institutions want the efficiency of DeFi, but they also need compliance. Enterprises want automation, but they also need control. Investors want yield access, but they also need risk visibility.

Permissioned DeFi lending platforms will be providing financial players a way to use blockchain lending without ignoring legal, operational, and reputational risk.

As tokenized private credit, RWAs, stablecoins, and on-chain collateral markets grow, compliant DeFi lending platform development will become a bigger opportunity for fintech companies, banks, credit firms, and Web3 startups.

Build a Permissioned DeFi Lending Platform With SoluLab

Choose Solulab as your trusted partner for permissioned DeFi lending platform development. As a leading DeFi development company, SoluLab offers DeFi development services for secure lending platforms, smart contract development, token creation, crypto wallet integrations, liquidity pools, and compliant infrastructure.

Whether you need a custom platform or a white-label permissioned DeFi platform, our experts can help you to design enterprise DeFi lending solutions aligned with your business model, compliance needs, and growth plan.

FAQs

Shipra Garg is a tech-focused content strategist and copywriter specializing in Web3, blockchain, and artificial intelligence. She has worked with startups and enterprise teams to craft high-conversion content that bridges deep tech with business impact. Her work translates complex innovations into clear, credible, and engaging narratives that drive growth and build trust in emerging tech markets.