AI Overview

- White-label neo banking platforms are moving toward Layer 2 blockchains to solve cost, speed, and scalability limitations

- A layer 2 blockchain neobank separates execution (Layer 2) from settlement (Layer 1)

- The real complexity lies in architecture, integrations, and operating model, not UI or features

- Layer 2 integrations involve transaction routing, rollups, bridging, and fee abstraction

- Compliance must be embedded into system design, not added later

- Success depends on infrastructure decisions early, not post-launch fixes

Banking infrastructure is quietly undergoing a shift. Not at the user interface level, where most fintech conversations still sit, but deeper, at the settlement and execution layers.

White-label neo banking platforms were originally built for speed.

Faster launches, lighter compliance lift, and modular product stacks. But as transaction volumes, cross-border use cases, and programmable finance demands increase,

the limitations of traditional rails and even Layer 1 blockchain systems are becoming visible.

This is where Layer 2 blockchain development solutions enter the picture.

A layer 2 blockchain neobank is not just a faster version of a crypto-first bank.

It represents a structural shift in how financial products are built, settled, and scaled. And for businesses exploring white label neo banking solutions, this changes both the architecture and the decision-making process.

Why White-Label Neo Banking Platforms Are Shifting to Layer 2?

The first wave of crypto neo banking focused on access. Wallets, exchanges, and fiat on-ramps. The second wave is about performance and programmability.

Layer 1 blockchains brought transparency and decentralization, but they also introduced friction:

- High transaction costs during peak demand

- Latency issues for real-time financial use cases

- Limited scalability for consumer-grade banking applications

For businesses building white-label neo banking applications, these limitations translate into real operational challenges.

Layer 2 blockchains address this by:

- Moving transaction execution off the main chain

- Compressing and batching transactions

- Reducing costs without compromising security guarantees

This makes them particularly relevant for:

- High-frequency payment systems

- Microtransactions and consumer apps

- Cross-border settlement flows

- Tokenized asset platforms

In short, building a white-label neo-bank on Layer 2 is less about adopting new technology and more about unlocking viable economics at scale.

The Evolution of Crypto Neo Banking Infrastructure

Early crypto neo banking models were built as overlays on existing systems:

- Custodial wallets connected to exchanges

- Fiat rails powered by banking partners

- Limited programmability beyond transfers

Over time, the stack evolved into:

- Multi-chain wallet infrastructure

- Smart contract-based financial products

- Embedded compliance tooling

Now, the next phase is emerging, where Layer 2-powered white-label neo banking platforms redefine how transactions and services are executed.

Key shifts include:

From custody to control

Users increasingly expect non-custodial or hybrid custody models.

From transactions to programmable flows

Payments are no longer isolated events. They are part of logic-driven systems like subscriptions, lending triggers, or yield strategies.

From backend abstraction to infrastructure visibility

Enterprises now care about how systems scale, not just how they look.

This is why blockchain app development is moving closer to infrastructure design than product assembly.

What “Layer 2 Blockchain Neobank” Actually Means in Practice

The term sounds straightforward, but in implementation, it involves multiple layers of coordination.

A white label neo bank designed on Layer 2 typically includes:

- A Layer 1 blockchain for security and settlement guarantees

- A Layer 2 network for execution and scalability

- Middleware for bridging, state synchronization, and data integrity

- Application layers for user-facing banking services

In practical terms, this means:

- Payments are executed on Layer 2 for speed

- Final settlement is anchored on Layer 1

- Fees are significantly reduced

- Throughput increases dramatically

For businesses exploring white-label neo-banking solutions on Layer 2 blockchains, this creates new design considerations:

- Which Layer 2 protocol to integrate

- How to manage bridging risks

- Where compliance checks are enforced

- How liquidity flows between layers

This is no longer just a fintech product decision. It is an infrastructure decision.

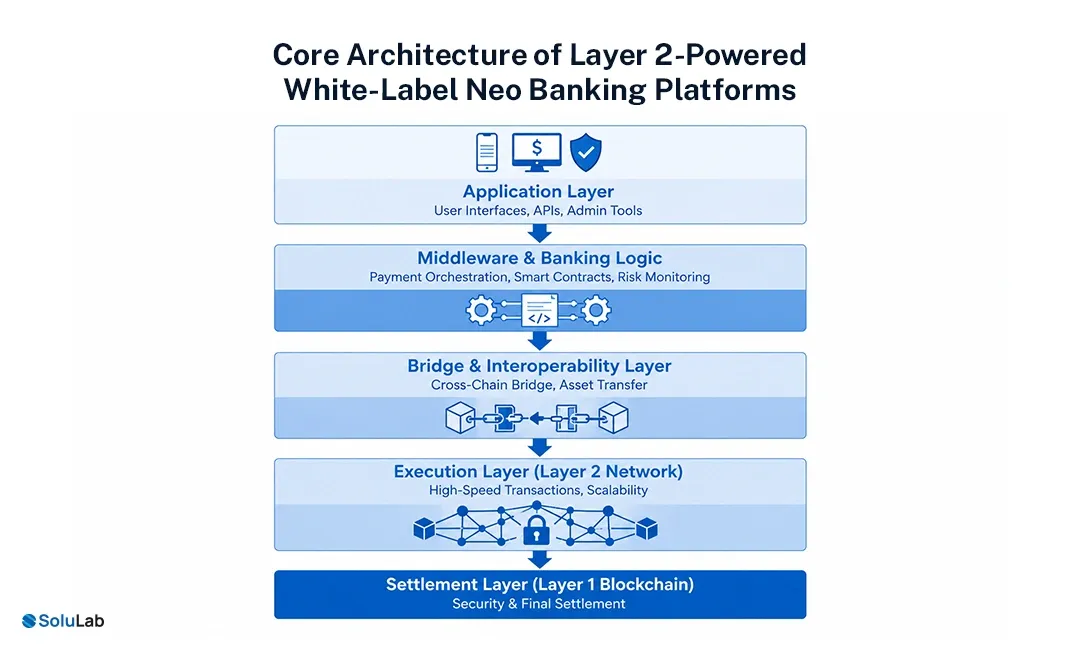

Core Architecture of Layer 2-Powered White-Label Neo Banking Platforms

At a high level, the architecture of a white-label neo-banking development solution built on Layer 2 blockchain can be broken down into five layers:

1. Settlement Layer (Layer 1 Blockchain)

- Provides security and immutability

- Stores final transaction states

- Acts as the trust anchor

2. Execution Layer (Layer 2 Network)

- Handles transaction processing

- Enables high throughput

- Reduces fees significantly

3. Bridge & Interoperability Layer

- Moves assets between Layer 1 and Layer 2

- Ensures liquidity continuity

- Manages cross-chain interactions

4. Middleware & Banking Logic

- Account management

- Payment orchestration

- Smart contract execution

- Risk monitoring

5. Application Layer

- User interfaces (apps, dashboards)

- APIs for partners

- Admin and compliance tools

This layered approach is what enables scalable white label digital banking solutions without compromising on control or compliance.

Key Components in White Label Neo Bank Development

When teams talk about white label crypto bank development, the conversation often starts with features. Cards, wallets, dashboards. But in reality, those are just outcomes.

What actually matters is how the system behaves underneath.

A white label digital banking solution, especially one built on Layer 2, is less like assembling modules and more like designing a controlled financial environment where every action has rules, dependencies, and consequences.

Let’s break that down.

Identity is no longer just onboarding

In traditional systems, KYC is a checkpoint. In a layer 2 blockchain neobank, identity becomes reusable infrastructure.

Users don’t just verify themselves once. Their identity flows across:

- transactions

- compliance checks

- smart contract interactions

This is where identity tokenization and persistent verification layers start becoming important. It reduces friction, but more importantly, it creates consistency in how compliance is enforced.

Wallets define control, not just storage

In most white-label neo banking applications, crypto wallet design becomes a strategic decision.

Do you control custody?

Does the user?

Or is it shared?

Each choice impacts:

- regulatory exposure

- user trust

- operational responsibility

Layer 2 adds another layer of nuance here. Because now, wallets must seamlessly interact across execution layers without exposing complexity to the user.

Payments are no longer simple transfers

In a crypto neo banking system built on Layer 2, a payment is rarely just a transfer.

It could trigger:

- a smart contract

- a compliance rule

- a liquidity movement across layers

Which means your payment engine is not just moving funds. It is orchestrating outcomes.

And this is where most white label neo banking solutions either become powerful or fragile.

Compliance becomes embedded, not external

Compliance cannot sit outside the system anymore.

It has to be woven into:

- transaction logic

- user behavior

- smart contract execution

Especially when you’re creating white-label neo-banking solutions on Layer 2 blockchain, where transaction speed is high, and reversibility is limited.

The real takeaway

A strong white label neo bank development approach doesn’t ask,

“What features do we need?”

It asks,

“How does the system behave under scale, risk, and regulation?”

That shift is what separates deployable platforms from unstable ones.

Layer 2 Integrations: What Actually Gets Built

“Layer 2 integrations” is one of those phrases that sounds deceptively simple.

In reality, it’s where most of the engineering complexity sits.

When you build white label neo bank on Layer 2 blockchain, you are not just connecting to a faster network. You are redesigning how transactions move through your system.

It starts with decision-making, not execution

Every transaction needs a decision layer:

- Should this go through Layer 2?

- Does it require Layer 1 finality immediately?

- Is there a cost optimization opportunity?

This routing logic becomes critical as volumes grow.

Rollups are not plug-and-play

Whether it’s optimistic rollups or zk-rollups, each comes with trade-offs:

- latency vs security assumptions

- cost vs complexity

- dispute windows vs finality

A white-label neo-banking app development solution built on Layer 2 blockchain has to align these choices with its business model.

Bridging is where risk lives

Moving assets between layers sounds straightforward, but it introduces:

- liquidity fragmentation

- timing mismatches

- potential security vulnerabilities

This is why bridging is not just an integration problem. It is a risk management problem.

Fee abstraction shapes user experience

End users don’t think in gas fees.

So systems need to:

- abstract costs

- optimize routes

- sometimes subsidize transactions

This is where Layer 2 actually becomes invisible to the user, which is exactly how it should be.

What this really means?

Layer 2 integrations are not a technical add-on.

They redefine how your banking system thinks, routes, and settles value.

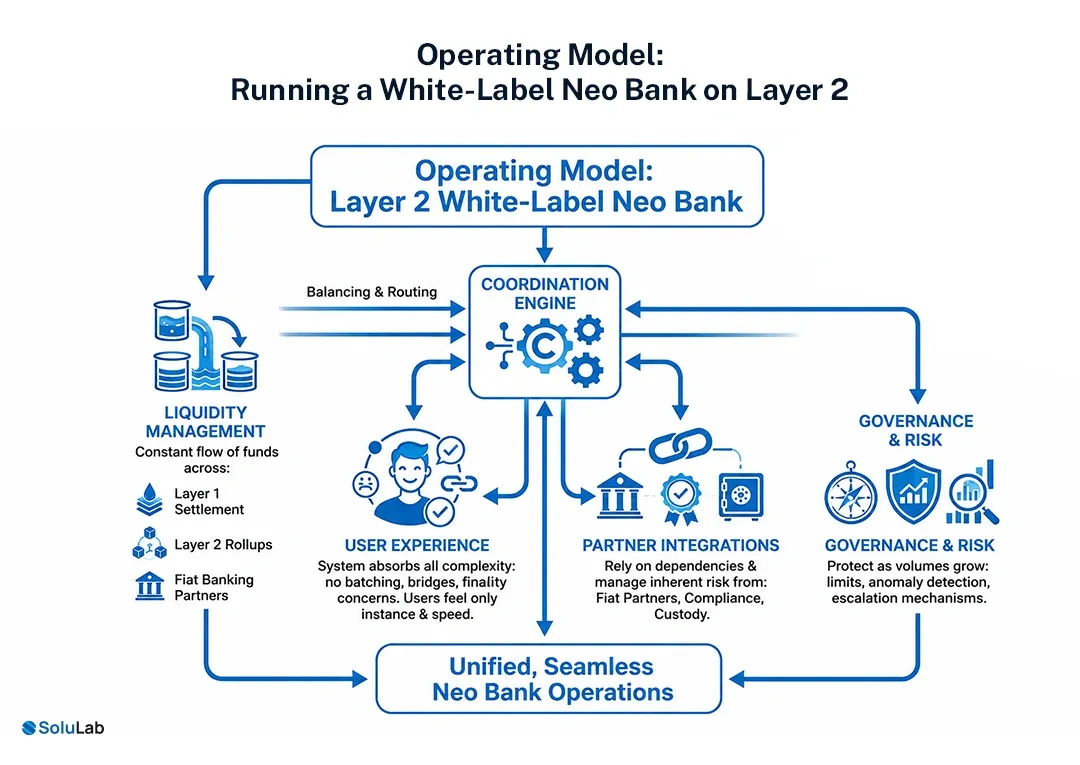

Operating Model: Running a White-Label Neo Bank on Layer 2

Launching is one milestone. Operating is another.

Many white-label neo banking platforms perform well in controlled environments but struggle when real-world complexity kicks in.

Because running a white label neo bank designed on Layer 2 is not just about uptime.

It is about coordination.

Liquidity is always moving

Funds are not sitting in one place anymore.

They exist across:

- Layer 2 environments

- Layer 1 settlement layers

- fiat banking partners

Managing this flow requires constant balancing.

Too much liquidity on Layer 2, and settlement gets delayed.

Too little, and transactions fail or slow down.

The user should never feel the complexity

Users expect instant, seamless experiences.

They should not care whether:

- a transaction was batched

- a bridge was used

- a rollup finalized

Which means your system must absorb all that complexity internally.

Partners are part of your system

A crypto neo bank development company doesn’t operate in isolation.

You rely on:

- fiat banking partners

- compliance providers

- custody infrastructure

Each introduces dependencies. Each introduces risk.

The operating model must account for this, not treat it as an afterthought.

Governance is not optional

As transaction volumes grow, so does exposure.

You need:

- transaction limits

- anomaly detection

- escalation mechanisms

Because in Layer 2 environments, issues can scale very quickly if left unchecked.

Compliance, Risk, and Regulatory Design

There is a common misconception that blockchain simplifies compliance.

In reality, it redistributes it.

For white-label neo-banking solutions on Layer 2 blockchains, compliance becomes more dynamic, not less.

Visibility improves, but responsibility increases

Yes, transactions are traceable.

But:

- cross-layer movement complicates tracking

- smart contracts introduce new risk vectors

Which means monitoring systems must evolve alongside infrastructure.

Custody is still a regulatory anchor

No matter how advanced your system is, regulators will still ask:

- Who holds the assets?

- How are they secured?

- What happens in failure scenarios?

This is where wallet architecture decisions directly impact compliance posture.

Smart contracts introduce operational risk

They automate logic, but they also lock it in.

Errors are not easily reversible.

Upgrades require careful design.

This is why audits, testing, and fallback mechanisms are critical in blockchain development.

Bridges are under scrutiny

Given past exploits, regulators and enterprises alike are paying close attention to:

- how assets move between layers

- how liquidity is protected

This is no longer just a technical concern. It is a compliance concern.

The bigger picture

Compliance is not a layer you add later.

It is something you design into every part of your white label neo banking solutions from the beginning.

Build vs Partner: Choosing the Right White Label Neo Bank Development Company

At some point, every team reaches the same question:

Do we build this ourselves, or do we work with a partner?

The honest answer is that most systems today are hybrids.

Building gives you control, but at a cost

If you choose to build:

- you own the architecture

- you control the roadmap

- you carry the full execution risk

And in a layer 2 blockchain neobank, that risk is not trivial.

Partnering accelerates, but requires alignment

Working with a white label neo bank development company can:

- reduce time to market

- bring proven frameworks

- de-risk compliance integration

But only if the blockchain development partner understands infrastructure, not just interfaces.

This is where firms like SoluLab typically differentiate themselves. The focus is not on shipping an app quickly, but on:

- structuring the system correctly

- planning phased rollouts

- aligning compliance and architecture early

The real decision

It is not build vs partner.

It is:

Where do we need control, and where do we need certainty?

Cost, Time, and Go-to-Market Realities

One of the most underestimated aspects of building a white-label neo-bank on Layer 2 is not technology. It is sequencing.

Time is shaped by dependencies

Even if your engineering moves fast, progress depends on:

- compliance approvals

- banking partnerships

- infrastructure readiness

Which is why timelines often stretch beyond initial expectations.

Costs are not evenly distributed

Most budgets go toward:

- Layer 2 integration complexity

- compliance infrastructure

- security audits

Not UI or front-end experiences.

And this is where many teams misallocate resources early. Blockchain development cost varies as per requirement and business idea.

Go-to-market is not a launch event

Successful white-label neo-banking development solutions built on Layer 2 blockchain rarely launch fully formed.

They:

- start with a focused use case

- validate operational flows

- expand gradually

Because in financial systems, stability matters more than feature breadth.

What experienced teams understand

You are not launching a product.

You are launching a system that must hold under pressure.

And that changes how you plan everything.

Conclusion

The shift toward Layer 2-powered white-label neo banking platforms is not about adopting faster infrastructure. It is about rethinking how financial systems are designed, scaled, and governed.

For teams exploring white-label neo-banking solutions on Layer 2 blockchains, the real advantage lies in aligning three things early: architecture, compliance, and operating model. Miss that alignment, and even the most advanced stack struggles under real-world conditions.

What’s emerging is a new category of banking platforms. Systems that are not only digital-first, but infrastructure-aware. Where transaction logic, risk controls, and liquidity flows are designed as one cohesive system.

This is where experienced blockchain development company in USA begin to matter. Not just to accelerate development, but to ensure that what gets built can actually sustain scale, regulation, and complexity over time.

Because in the end, building a neo bank is not about launching quickly. It is about building something that holds.

FAQs

Shipra Garg is a tech-focused content strategist and copywriter specializing in Web3, blockchain, and artificial intelligence. She has worked with startups and enterprise teams to craft high-conversion content that bridges deep tech with business impact. Her work translates complex innovations into clear, credible, and engaging narratives that drive growth and build trust in emerging tech markets.