Key Takeaways

- For neobanks, it reduces operational expenses (OpEx) by automating reconciliation, compliance, and multi-party settlements.

- High-growth businesses are moving toward “always-on” treasury management, making programmable payments a must-have feature for white-label platforms.

- White-label neo banking solutions gain a competitive edge through embedded payment logic, and Smart Money technology is shaping the future of neo banking platforms.

Today, White-Label Neo Banking Solutions are integrating smart money technology directly into their DNA. But what exactly is programmable money? At its core, it is money that knows what to do. By using Smart Money Technology, businesses can embed logic, if/then statements, into the currency itself.

Whether it’s a self-executing escrow, an automated tax split, or a supply chain payment triggered by an IoT sensor, programmable money is transforming white label Neo banking platforms from passive storage units into active, autonomous financial engines. For enterprises looking to launch their own branded financial services, understanding this shift is not just an advantage; it’s a survival requirement.

For enterprises, this is not a feature upgrade. It is a 180-degree change in how financial systems operate.

Why is Programmable Money the Strategic Core of Modern White-Label Neobanking?

Traditional banking systems were built for storage and transfer. Today’s financial ecosystems demand execution and intelligence.

Programmable money is a digital form of value, typically hosted on a distributed ledger or a high-speed blockchain server that has executable logic (smart contracts) embedded directly into the unit of value itself.

Unlike traditional electronic money, which requires manual external instructions to move, programmable money is “self-governing.”

1. Financial Logic Becomes a Product Feature

With Programmable Money in Banking, companies move beyond vanilla accounts to design how money behaves.

- Automated Tax Deductions: Real-time withholding at the point of transaction.

- Intelligent Salary Splitting: Instant distribution into savings, insurance, and spendable tax-advantaged buckets.

- Funds that unlock only when project KPIs are verified via API. This turns a white-label Neo bank app into a bespoke financial engine tailored for specific industry verticals (e.g., Gig Economy, Construction, or SaaS).

2. Atomic Settlement: Eliminating the Liquidity Gap

Legacy systems suffer from settlement delays that trap billions in capital. Programmable Payments enable atomic transactions, where the payment and the transfer of asset ownership happen simultaneously.

- Reduced counterparty risk and immediate capital availability.

- For entrepreneurs, this directly improves working capital efficiency and removes the need for expensive short-term credit lines to cover “in-transit” funds.

While these capabilities define the future, their immediate impact is already visible in enterprise finance operations, especially in how treasury functions are evolving

3. Integration with Machine-Driven Economies

As AI agents begin making financial decisions, money must be controllable.

With smart money technology, businesses can:

- Restrict how funds are spent

- Assign budgets to AI systems

- Enable autonomous transactions with defined limits

This is where programmable money in neo banking becomes essential, not optional.

Scaling Enterprise Treasury: Use Cases for Programmable Payments in B2B Solutions

Enterprise adoption is driven by efficiency, and solutions lie in optimizing how capital is deployed, not innovation hype. This is why programmable money delivers measurable ROI.

1. Just-in-Time (JIT) Liquidity Management

Idle capital is one of the biggest inefficiencies in enterprise finance.

With digital money automation:

- Funds are deployed only when needed

- Central treasury remains optimized

- Interest-earning potential increases

This is a direct cost-saving lever for CFOs.

2. Automated Revenue Distribution

Marketplaces and multi-party platforms benefit significantly.

- A single customer payment is split mid-stream: 80% to the vendor, 15% to the platform, and 5% to the tax authority.

- This results in zero manual reconciliation and zero payout delays.

This removes operational complexity from neo banking platforms.

3. Conditional Trade Finance

Traditional escrow slows down transactions.

With programmable logic:

- Funds remain locked but visible

- Release happens automatically on delivery confirmation

- No third-party escrow dependency

This reduces both cost and friction.

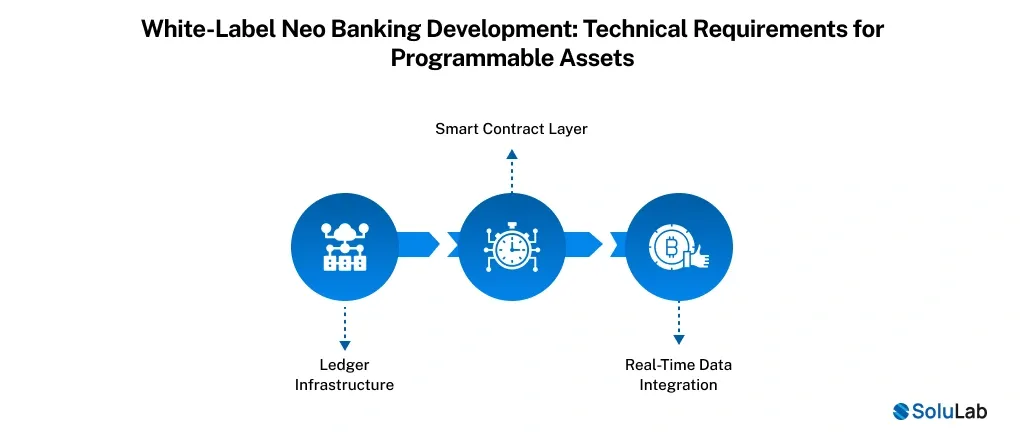

White-Label Neo Banking Development: Technical Requirements for Programmable Assets

Building white-label neo bank solutions with programmable capabilities requires a composable and scalable architecture.

1. Ledger Infrastructure

A modern white-label neo-banking platform needs:

- High-throughput transaction processing

- Multi-asset support (fiat, stablecoins, tokenized deposits)

- Hybrid architecture (centralized + DLT integration)

This ensures scalability and interoperability.

2. Smart Contract Layer

Programmable logic must be accessible and secure.

Key requirements:

- Pre-built templates for common financial workflows

- Low-code interfaces for rule creation

- Integration with Banking as a Service (BaaS) providers

This accelerates go-to-market timelines.

3. Real-Time Data Integration

Programmable money depends on triggers.

Required integrations:

- Payment gateways

- ERP systems

- External data sources (APIs/oracles)

Without real-time data, automation loses its value.

Read Blog Post: AI Agents into Crypto Neo-Banking Solution

Ensuring Security and Reliability in Programmable Money Platforms

Automation introduces new risks. Institutional-grade platforms prioritize three security pillars:

1. Formal Verification of Logic

Smart contracts must behave exactly as intended

- Mathematical proof that the programmable logic cannot be exploited.

- Zero ambiguity in execution

- Reduced risk of financial errors

2. Multi-Party Authorization (MPC)

Enterprise-grade security requires distributed control.

- Eliminating “Single Points of Failure” by distributing signing authority across multiple parties.

- Shared transaction authorization

- Secure treasury operations

3. Built-in Risk Controls

Financial systems need safeguards.

- Transaction limits

- Automated triggers that freeze funds if anomalous behavior

- Fraud detection triggers

Security is not an add-on. It is core to programmable money solutions.

Case Study: Institutional Adoption of Programmable Money

Recently, J.P. Morgan’s Kinexys (formerly Onyx) and the Solana developer platform set the benchmark for white-label success.

- The project is integrating cross-border flows of Mastercard and Western Union, which have begun utilizing programmable “Bank-Side” logic.

- By embedding compliance and settlement logic directly into the payment rail, these entities have reduced settlement times from 3 days to under 10 seconds.

- This slashes OpEx by 30 to 40% through the removal of manual treasury interventions.

There are several adaptations of programmable money in banking solutions.

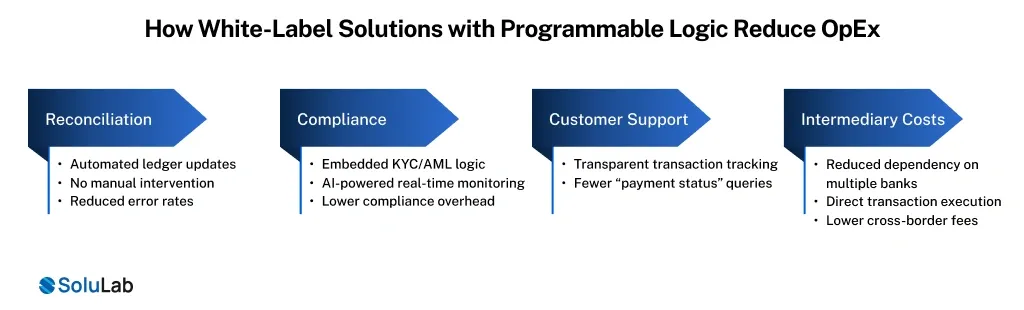

How White-Label Solutions with Programmable Logic Reduce OpEx?

Cost efficiency is where programmable systems deliver immediate value.

Reconciliation

- Automated ledger updates

- No manual intervention

- Reduced error rates

Compliance

- Embedded KYC/AML logic

- AI-powered real-time monitoring

- Lower compliance overhead

Customer Support

- Transparent transaction tracking

- Fewer “payment status” queries

Intermediary Costs

- Reduced dependency on multiple banks

- Direct transaction execution

- Lower cross-border fees

For enterprises, this directly translates into leaner financial operations.

Final Words to Enterprises That Wish to Build a Neo Banking Platform

When you connect all these layers, you can say, programmable money gives businesses control over how money moves, when it moves, and why it moves.

This flexibility helps companies manage both short-term liquidity and long-term financial planning without adding operational complexity.

It brings practical advantages:

- Faster settlements

- Reduced financial risk

- Better cash flow visibility

- Lower operational overhead

But building this kind of infrastructure requires the right technical foundation and execution approach.

As a blockchain development company, SoluLab helps businesses turn programmable finance into real-world systems.

Our capabilities include:

- Smart contract development for programmable payments

- Stablecoin and digital asset integration

- AI-driven financial automation and analytics

- Secure, scalable neo banking platform development

Connect with our team to discuss your requirements and build a programmable banking system aligned with your business model.

FAQs

Deepika is a content writer who blends storytelling with strategic thinking. She explores topics across digital innovation, emerging tech, and the evolving blockchain industry. She enjoys breaking down complex ideas into simple, engaging narratives in the growing global markets.