Key Takeaways

- Move from T+3 to real-time liquidity via SEPA Instant and FedNow. Leverage FAPI 2.0 for credential-free, tokenized payment authorization.

- A2A payments enable real-time, direct bank transfers, eliminating intermediaries and significantly improving transaction speed and reliability for neo banks.

- Cost reduction is a major advantage, as A2A payments bypass card networks, helping neo banks save up to 30–50% in transaction fees.

- Improved user experience through instant settlements, seamless checkout, and fewer payment failures leads to higher customer retention.

- Enhanced security and compliance, as A2A payments operate within regulated banking systems with strong authentication protocols.

- A2A payments support scalable neo banking ecosystems, enabling integration with fintech services, wallets, and embedded finance platforms.

- Partnering with an experienced fintech and payment solutions provider– SoluLab ensures seamless A2A integration, secure infrastructure, and faster go-to-market for white-label neo bank platforms.

If you’re investing in white label neo bank development, the real differentiator today is not UI or onboarding. It’s a payment infrastructure.

Card rails are becoming a liability. They introduce delays, increase costs, and expose systems to rising fraud risks. At the same time, enterprise clients expect instant settlement, lower fees, and seamless user experience.

Account-to-Account (A2A) payments are emerging as the default payment rail for high-performance fintech systems. By enabling direct bank-to-bank transfers without intermediaries, A2A payments reduce costs, accelerate settlements, and improve reliability.

For businesses focused on scalable white label neo bank development, integrating A2A payments is no longer optional; it’s a strategic necessity to deliver faster, more secure, and cost-efficient financial services.

Why Are A2A Payments The “Margin-Saver” For Neobanks In 2026?

A2A payments enable direct bank-to-bank fund transfers, eliminating the need for card networks or intermediaries.

Instead of entering card details, users authenticate directly through their crypto banking app, typically using biometrics. This creates a seamless and secure payment experience.

What is an A2A Payment Method?

An A2A payment method is a Pay-by-bank system where funds move directly between accounts through APIs powered by open banking frameworks.

Unlike cards:

- No interchange fees

- No card network dependency

- No risk of expired credentials

What is A2A Banking?

A2A banking refers to a financial ecosystem where payments, subscriptions, and settlements are executed directly through bank rails using APIs, tokenization, and real-time infrastructure.

The convergence of blockchain-based payments and A2A rails is eliminating the need for traditional correspondent banking.

- Open Banking 2.0 (PSD3 / PSR frameworks)

- Account-on-File (AoF) tokenization

- Real-time settlement systems

- Programmable payment logic

This evolution is central to modern white label neo banking solutions, aiming to deliver faster and cheaper financial services.

Real-Time Settlement Is The New Liquidity Standard: How A2A Bypasses The T+3 Delay

Margins are tightening across fintech. Card networks continue to introduce layered fees, from interchange to scheme charges and digital service costs.

A2A eliminates most of these.

1. Direct Cost Advantage

By adopting white label neo bank development services that prioritize A2A rails, businesses can:

- Avoid card scheme fees entirely

- Shift to flat API-based transaction pricing

- Improve revenue predictability

This can reduce transaction overhead by up to 80%, making A2A one of the most powerful levers for profitability.

Case Insight: Amazon x TrueLayer

Amazon integrated “Pay by Bank” across Europe to reduce card fees and checkout friction.

What changed:

- Users no longer enter card details

- Payments were authorized via banking apps with biometrics

- Refunds were processed instantly instead of 5–7 days

Business impact:

- Lower processing costs

- Reduced dependency on stored card data

- Higher conversion rates through faster refunds

This shows how A2A is not just cost-saving. It directly improves user experience and retention.

A2A solves this.

2. From T+3 to Instant Settlement

Traditional card payments follow delayed settlement cycles. A2A enables:

- T+0 or real-time settlement

- Immediate balance updates

- Faster cash flow for businesses

Note: To achieve true T+0, leading platforms are using RWA tokenization services to create a 1:1 digital representation of account balances, allowing for atomic settlement.

3. Infrastructure Behind It

Modern white-label neo bank development company stacks integrate:

- SEPA Instant (Europe)

- FedNow (USA)

- ISO 20022 messaging standards

ISO 20022 adds structured data like invoice IDs and tax references, enabling automated reconciliation.

How does Open Banking 2.0 enhance A2A Security and User Trust?

Security is no longer about protecting data. It is about eliminating exposure.

How A2A Improves Security

With A2A:

- No sharing of sensitive card details

- Tokenized bank credentials replace raw data

- Transactions are authenticated via biometrics

FAPI 2.0 and Tokenization

By integrating AI agents monitoring into the FAPI 2.0 flow, we move from reactive security to proactive defense against APP fraud.

- Secure communication between banks and apps

- Encrypted authorization flows

- Reduced attack surface

This is a critical upgrade for any white label neo banking solution targeting enterprise clients.

As A2A adoption grows, so does the need for proactive fraud prevention.

Case Insight: Chime & Real-Time Risk (March 2026)

With rising A2A transactions, fraud patterns shifted toward authorized push payment (APP) scams.

Chime addressed this by integrating real-time behavioral risk analysis.

What changed:

- Detection moved from post-transaction to pre-authorization

- Systems analyzed device behavior and session activity

- Suspicious transactions were blocked before execution

Outcome:

- Millions saved in fraud losses

- Stronger trust in A2A infrastructure

For any white label crypto bank development company, embedding real-time risk engines is now essential.

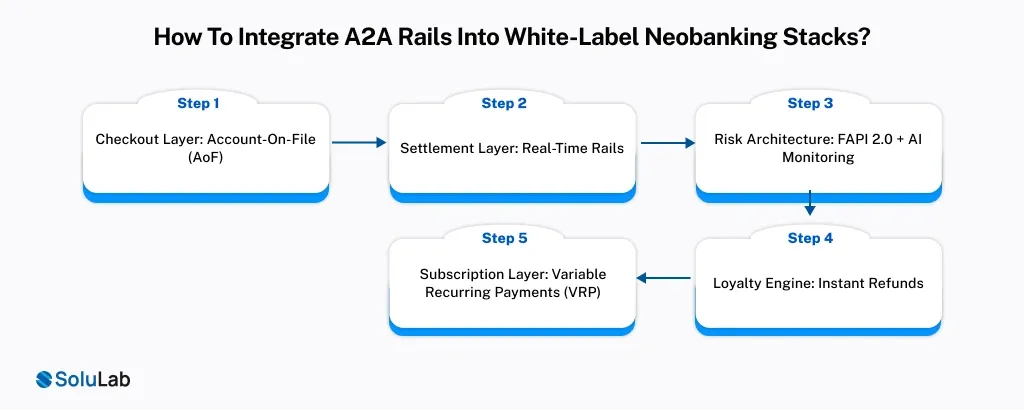

How To Integrate A2A Rails Into White-Label Neobanking Stacks?

Integration in 2026 is modular, not monolithic. Modern fintech systems are built like composable layers.

1. Checkout Layer: Account-on-File (AoF)

AoF allows users to save a tokenized version of their bank account.

Benefits:

- One-click checkout similar to cards

- No need to re-authenticate repeatedly

- Higher conversion rates

2. Settlement Layer: Real-Time Rails

Your system should support:

- SEPA Instant

- FedNow

- Local instant payment systems

This ensures global coverage and real-time liquidity.

3. Risk Architecture: FAPI 2.0 + AI Monitoring

Modern stacks include:

- Tokenized authentication

- Behavioral risk engines

- AI-driven fraud detection

4. Loyalty Engine: Instant Refunds

A2A enables instant refunds, which can be used as a growth lever.

This mirrors the Amazon strategy:

- Faster refunds increase customer trust

- Improves repeat purchases

- Reduces support overhead

5. Subscription Layer: Variable Recurring Payments (VRP)

VRP replaces outdated direct debit systems by allowing:

- User-controlled recurring payments

- Flexible billing structures

- Real-time authorization

This is a key feature in advanced white label neo banking app development solutions.

Is your Neobank ready for the “Pay-by-Bank” era? Diversifying payment methods for 2026

A2A is not limited to consumer payments. It is now entering institutional finance.

Case Insight: MoraBanc Tokenized Settlement Bridge (January 2026)

MoraBanc used A2A as an entry layer to tokenize fiat deposits.

What changed:

- Funds moved from traditional systems into tokenized environments

- Settlement time reduced from 48 hours to under 10 seconds

Impact:

- Eliminated cross-border delays

- Improved institutional liquidity

- Built a compliant bridge between traditional finance and digital assets

This demonstrates how white label neo bank development services can extend beyond retail into high-value enterprise applications.

Consumers prefer faster, safer, and simpler payment methods. Businesses want lower costs and instant liquidity.

A2A delivers both.

Neobanks that rely only on card infrastructure will face:

- Shrinking margins

- Higher fraud exposure

- Slower settlement cycles

On the other hand, platforms built on A2A rails can:

- Offer competitive pricing

- Deliver superior user experience

- Scale across retail and enterprise use cases

Conclusion

A2A payments are no longer an alternative. They are becoming the default infrastructure for modern fintech.

For businesses investing in white label neo bank development, the path forward is clear: build on real-time rails, prioritize tokenized security, and optimize for cost efficiency and liquidity.

The future of neobanking is not card-first but rail-agnostic, API-driven, and A2A-powered. At SoluLab, top blockchain solution development agency, we help enterprises turn this shift into a scalable advantage through end-to-end neo banking development services.

Our experts handle everything from A2A integration to compliant infrastructure design. If you’re planning to launch or upgrade your platform, connect with a trusted NEO Banking development company that understands 2026-ready fintech architecture. Contact us to get started.

FAQs

Deepika is a content writer who blends storytelling with strategic thinking. She explores topics across digital innovation, emerging tech, and the evolving blockchain industry. She enjoys breaking down complex ideas into simple, engaging narratives in the growing global markets.