AI Summary

- To start a Neobank in 2026, choose your regulatory path early (own license vs Banking-as-a-Service), because it decides your cost, time-to-market, and compliance obligations.ericaai.

- Use a BaaS or White-label Neobank Solution for a faster digital bank setup, then layer your own UX, niche features, and monetization on top (interchange, subscriptions, FX, lending, and value-added services).

- Build your tech stack around mobile-first onboarding, robust KYC/AML/fraud controls, card issuing, payments, and real-time monitoring so that compliance and UX reinforce not fight each other.

- Start narrow: pick a specific segment (SMBs, freelancers, creators, Web3 users, migrants, etc.), solve one painful financial workflow extremely well, and only then expand into stablecoins, cross-border rails, or prediction-market style features.

- Partner with an experienced White-label Neo bank development company like SoluLab, which combines digital banking platform development, Web3 and stablecoin expertise, and end-to-end Neobank development to help you design, develop, and launch a Neobank with lower risk and faster execution.

How to start a Neobank in 2026 is no longer a theoretical question for founders; it is a tactical one shaped by licensing, BaaS partnerships, user experience, and compliance execution. If you want to start a Neobank in 2026 successfully, you need a clear Neobank setup guide that covers the business model, product scope, tech stack, launch cost, and go-to-market logic from day one.

In this guide, we break down the exact steps to start a Neobank, what it really takes to develop and launch a Neobank, and how to think about the right regulatory path for a modern digital bank setup. We will also cover where white-label neo bank development and custom development fit, what compliance teams expect, and how Web3 and crypto-native founders can build banking rails without overbuilding the first version.

What a Neobank really is?

A neobank is a digital-first financial brand that offers banking-like services through software rather than a legacy branch network. In practice, most neobanks today are not full charter banks; they operate through partner banks or a Banking-as-a-Service platform that provides the regulated infrastructure underneath the customer experience.

That distinction matters because it changes your timeline, cost to start a Neobank, and compliance burden. For founders, the real product is not “a bank” in the old sense; it is a mobile-first financial operating system with cards, accounts, payments, transfers, onboarding, and intelligent customer support layered on top of licensed rails.

Neobank Business Model

The neobank business model is usually built on a mix of interchange, subscription revenue, premium plans, FX fees, payment revenue, lending margin, and partner distribution economics. The most important rule is simple: if your monetization depends on one revenue stream, your business is fragile.

Most early-stage neobanks start with a narrow wedge, such as freelancers, SMBs, immigrants, creators, crypto users, or cross-border professionals. That niche gives you clearer onboarding logic, sharper product-market fit, and a stronger acquisition story than a generic “better banking” pitch.

Licensing paths in 2026

There are three realistic regulatory paths when you start a Neobank in 2026: full banking license, EMI/e-money authorization in some markets, or a BaaS partnership model. For most startups, especially in the US, BaaS is the fastest and most capital-efficient path because it lets you launch in months rather than years.

A full license gives you maximum control, but it also requires heavy capital, deep compliance, and long regulatory review cycles. If you are building for Europe or a crypto-financial use case, you also need to evaluate MiCA and adjacent licensing implications early, especially if stablecoins or custody features are part of the roadmap. Many businesses are now prioritizing MiCA-compliant neo bank solutions to align with evolving EU crypto regulations while ensuring long-term scalability and regulatory readiness.

Fast decision rule

- Choose BaaS if you want to validate demand quickly and ship a focused MVP.

- Choose a license-first path if you already have scale, capital, and a long-term regulated roadmap.

- Choose a hybrid approach if you are launching a digital wallet or crypto-enabled banking product with future license expansion in mind.

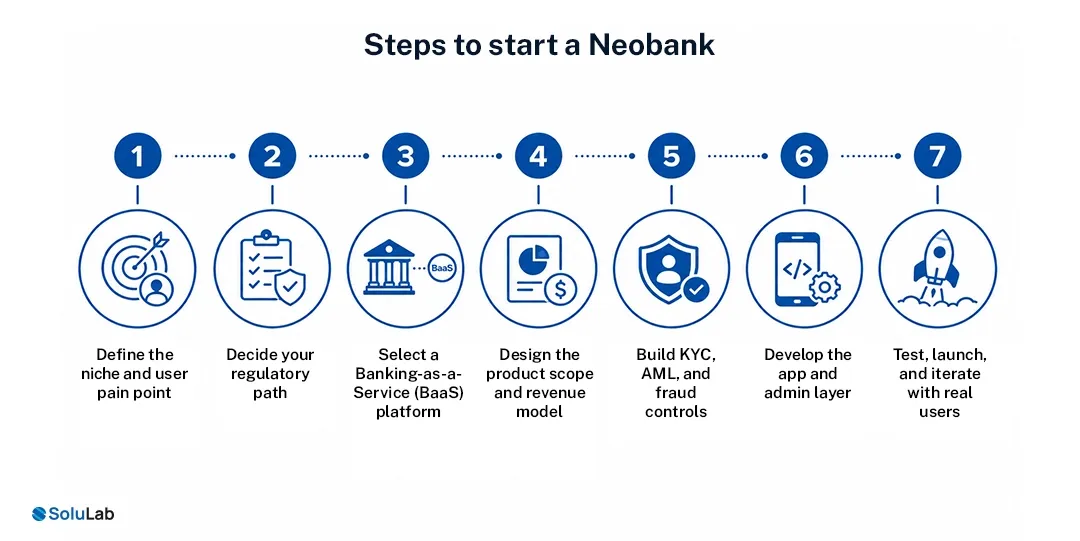

7 Easy Steps to Start a Neobank

The steps to start a Neobank should follow a sequence, not a brainstorming loop. The biggest mistake founders make is designing features before they choose the operating model.

- Define the niche and user pain point.

- Decide your regulatory path.

- Select a Banking-as-a-Service (BaaS) platform.

- Design the product scope and revenue model.

- Build KYC, AML, and fraud controls.

- Develop the app and admin layer.

- Test, launch, and iterate with real users.

This is the point where a strong Neobank software development company becomes valuable, because the product is not just front-end design; it is a compliance-aware system architecture, payment orchestration, and onboarding optimization wrapped into one.

Tech stack and product scope

A strong crypto banking platform development plan starts with the minimum viable set of features: account creation, identity verification, card issuance, payments, transfers, transaction history, notifications, support, and admin controls. Anything beyond that should earn its way into version 2.

Your tech stack for digital banking should be built for scale, observability, and regulatory traceability. That usually means a mobile app layer, API-driven backend, secure identity and fraud tooling, event logging, compliance dashboards, and a cloud setup that can support transaction-level auditing. Modern platforms are also increasingly integrating A2A payments in white-label neo bank solution architectures to enable faster, low-cost bank-to-bank transfers and seamless real-time payment experiences.

A well-structured build should also support future modules such as savings, lending, rewards, stablecoin rails, or merchant services. That is where digital banking solutions outperform generic app development, because the architecture is shaped for financial workflows rather than just software delivery.

Read More- Questions to ask White-label Neobank Development Company

Compliance and risk

KYC, AML, fraud monitoring, sanctions screening, and suspicious activity workflows are not optional add-ons; they are part of the core product. Even when a partner bank or BaaS provider handles the regulated plumbing, the startup still needs a compliant user journey and an audit-ready operating model.

This means onboarding design must balance conversion and risk. A slow or clumsy identity flow hurts growth, but a weak one creates regulatory exposure and partner-bank friction. In 2026, the winning teams treat compliance as a UX and infrastructure problem, not just a legal one.

White-label vs Custom build: Neo Banking Gaining Edge

White-label Neobank Solutions can accelerate launch for founders who need speed, a lower initial budget, or a proof-of-concept for investors. They are especially useful when your main value proposition sits in niche positioning, distribution, or a unique financial workflow rather than in building every layer from scratch.

A custom build makes more sense when your differentiation depends on proprietary UX, complex payment logic, crypto-native features, or future licensing control. In reality, many founders use a hybrid approach: white-label foundations for speed, then custom modules as traction grows.

What is the Cost to Start a Neobank?

The cost to start a Neobank in 2026 varies widely based on licensing strategy, feature depth, geography, and compliance scope. A BaaS-based MVP is commonly estimated in the low six-figure range, while a full custom and compliance-heavy build can move much higher.

Here is a practical planning range:

The smarter question is not “what is the cheapest build?” but “what build gets us to product-market fit before capital runs out?”

Web3 and Crypto angle

For Web3 and crypto-native founders, the opportunity is no longer just a “crypto app with a bank-like UI.” The real opportunity is a compliant financial layer that can connect fiat rails, stablecoins, cards, and on-chain assets in one experience. That is where hybrid neobanks and crypto-enabled banking products are gaining traction in 2026.

A strong digital bank setup for this segment should consider stablecoin settlement, custody partnerships, card-linked fiat onramps, and regional regulation from the start. This is also where SoluLab-style strategic capabilities align well with offerings such as AI-powered stablecoin yield in neo banking apps, Build MiCA-compliant Neo Bank, and Integrate prediction markets into neo bank app, which can be positioned as future-facing extensions rather than core MVP distractions.

The Go-to-market Strategy for Neo Banking Solutions

A crypto-friendly neo bank does not win by being broadly available; it wins by being sharply relevant. The best launches usually begin with one audience, one painful financial job-to-be-done, and one clear promise.

Your early acquisition strategy should combine:

- A narrow niche message.

- Referral loops.

- High-intent content marketing.

- Founder-led distribution.

- Partnerships with communities, platforms, or ecosystems.

If you are building for SMBs, creators, or crypto users, your onboarding narrative must match their vocabulary, trust model, and transactional habits. That makes the product feel native instead of generic.

Why Founders Fail in 2026?

Most neobank failures do not come from bad ideas; they come from poor sequencing. Founders either overbuild before validating demand, choose the wrong licensing model, or underestimate compliance and payment integration complexity.

Another common mistake is hiring generalist teams that can design screens but cannot build financial systems responsibly. To develop and launch a Neobank, you need product, compliance, engineering, and banking operations to work together from day one.

When to Hire a Professional Development Partner like SoluLab?

If you are serious about launch speed, regulatory alignment, and investor confidence, a Neo bank development company can shorten the path from concept to MVP. The right partner should understand BaaS integration, identity workflows, card infrastructure, transaction monitoring, mobile banking UX, and emerging capabilities like programmable money for neo banking solutions, not just app coding.

That is why many founders look for a Neo bank app development services partner that can combine strategy, product design, engineering, and compliance-aware execution in one delivery model. In a crowded market, the advantage is not only shipping faster; it is shipping with fewer expensive mistakes.

Final Build Advice!

The real advantage in 2026 won’t come from launching faster; it will come from launching smarter, with a tightly scoped, compliance-ready product that can scale without rework. Founders who anchor their strategy around real user behavior, regulatory clarity, and modular infrastructure will consistently outperform those chasing feature-heavy builds from day one.

This is where the right development partner becomes critical. SoluLab, leading blockchain development solution provider, brings deep expertise in building compliance-native, BaaS-driven neobank architectures that are designed for speed, scalability, and regulatory alignment from the ground up.

Whether you’re targeting a niche segment or planning a multi-market rollout, SoluLab helps translate your vision into a production-ready neobank integrating core banking, KYC/AML, payments, and next-gen capabilities like stablecoins or cross-border rails without unnecessary complexity or cost overruns.

FAQs

Shipra Garg is a tech-focused content strategist and copywriter specializing in Web3, blockchain, and artificial intelligence. She has worked with startups and enterprise teams to craft high-conversion content that bridges deep tech with business impact. Her work translates complex innovations into clear, credible, and engaging narratives that drive growth and build trust in emerging tech markets.