Key Takeaways

- Blockchain for Regulatory Compliance enables real-time auditability and automated enforcement

- Regulated decentralized finance (DeFi) requires identity, governance, and transaction controls

- Blockchain-based KYC reduces duplication while maintaining verification integrity

- Enterprises need a specialized Blockchain development company to build compliant systems at scale

Most projects fail because someone assumed Blockchain Regulatory Compliance could be handled later. Financial institutions have grown considerably more deliberate in how they evaluate blockchain vendors. Procurement teams ask harder questions. Legal departments push back earlier. Regulators across the globe are now enforcing new guidelines to build blockchain-based solutions. If a blockchain is unable to handle identity, transaction monitoring, data governance, and audit reporting, it is not regulatory compliant.

This shift has changed what enterprise blockchain development actually involves. Writing smart contracts is the easier part. The harder part is building a system that a compliance officer, an external auditor, and a regulatory examiner can all look at and find satisfactory. This guide explores what enterprises need to build regulated decentralized finance (DeFi) and blockchain solutions in 2026.

The Regulatory Landscape Is Not Uniform, but the Pressure Is

One of the more common misconceptions is that Blockchain for Regulatory Compliance is still vague or unsettled. In some jurisdictions, it is. But for enterprises operating in financial services, healthcare, real estate, or cross-border trade, the obligations are largely identifiable.

A tokenized securities platform faces different requirements than a supply chain ledger. A DeFi lending protocol operating in the EU must contend with MiCA in a way that a private enterprise identity network does not. What they share is the underlying pressure: demonstrate control over identity, transactions, data, and risk.

ESMA has already signaled that after July 2026, not every crypto-asset service provider will hold authorized status under MiCA. For enterprises building on or integrating with third-party blockchain infrastructure, that matters. Counterparty compliance status is now a due diligence item.

The areas that consistently require attention across most blockchain development solutions include KYC, AML, sanctions screening, Travel Rule obligations, data privacy, token classification, custody controls, smart contract security, tax reporting, and applicable licensing — not all of these in every case, but enough that they need to be mapped before architecture decisions are made.

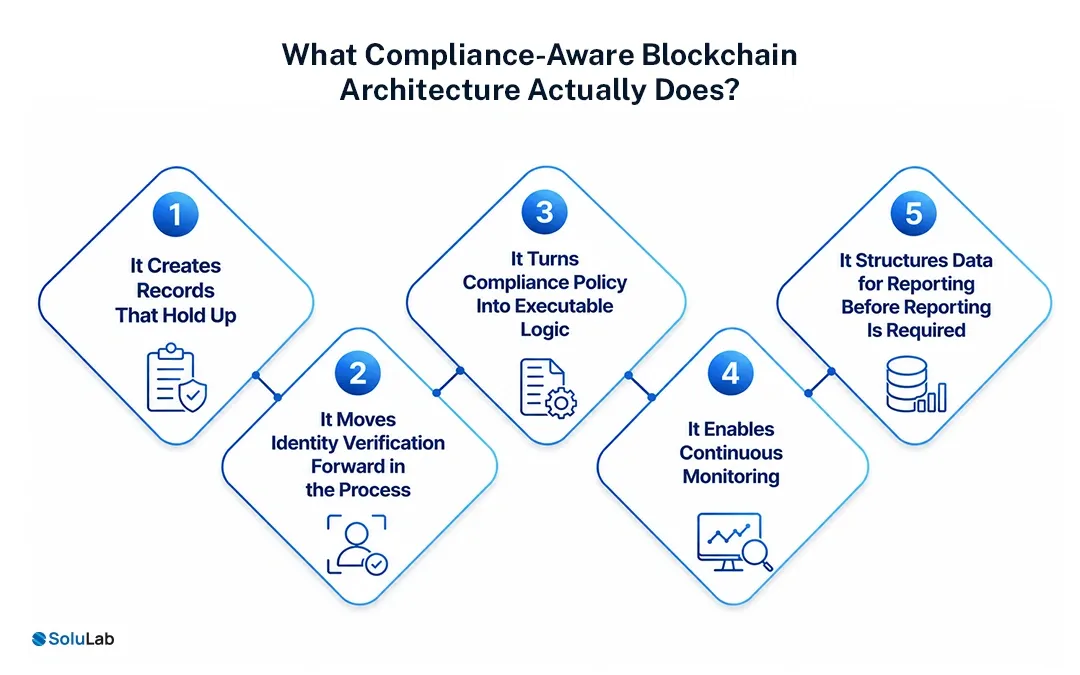

What Compliance-Aware Blockchain Architecture Actually Does?

Compliance-aware blockchain architecture helps businesses build blockchain technology ecosystems aligned with evolving regulatory, security, and governance expectations across global markets. It supports secure digital asset operations, transparent transaction management, identity verification, and enterprise-grade risk control frameworks.

- It Creates Records That Hold Up

Blockchain’s most immediately practical compliance contribution is the audit trail. These records reduce the effort required to respond to regulatory inquiries and internal audits. They also reduce the risk of disputes about what happened, when, and who authorized it. For enterprises that currently manage compliance through a combination of internal logs, emails, and manually maintained spreadsheets, this is a material operational improvement.

- It Moves Identity Verification Forward in the Process

In Traditional onboarding, users are required to repeat a similar process across platforms. This increases the business cost and causes duplication errors. Blockchain-based KYC fixes those issues by allowing verified credentials for users and allowing them to be shared selectively and with consent. The result is faster onboarding, lower operational overhead, and an identity record that is traceable and consistent rather than fragmented across systems.

- It Turns Compliance Policy Into Executable Logic

Instead of depending upon the manual processes to enforce regulations on transaction limits, restrict counterparties, and review workflows, with Blockchain Regulatory compliance, businesses can write these rules directly into the contract logic. They execute consistently and do not require the human to remember them always.

- It Enables Continuous Monitoring

Traditionally, businesses require multiple steps for batch processes, which is time-consuming. But with top blockchain platforms, they can run these checks in real time and flag the problems during transactions. For financial platforms operating in real-time, functionality can create a huge difference between catching a problem and reporting one.

- It Structures Data for Reporting Before Reporting Is Required

Regulatory reporting is frequently slow because the underlying data is unstructured, stored in multiple systems, or requires manual reconciliation. When reporting requirements are considered during platform design, the data can be structured to meet them from the start. That makes compliance cycles faster, reduces error rates, and frees compliance teams to focus on judgment calls rather than data gathering.

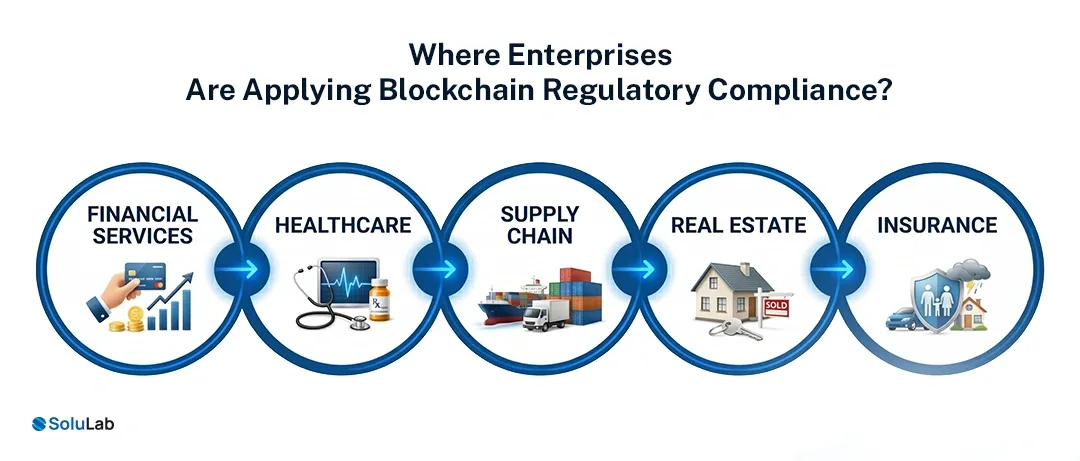

Where Enterprises Are Applying Blockchain Regulatory Compliance?

The enterprises are applying blockchain regulatory compliance across numerous sections, as mentioned below:

- Financial services– This involves tokenized assets, settlement infrastructure, digital custody, and regulated DeFi products designed for institutional participants.

- Healthcare- Regulatory compliance results in consent management, data access logs, and integrity assurance for clinical records.

- Supply chain- This unlocks provenance documentation, customs compliance, ESG reporting, and counterfeit prevention.

- Real estate– It provides access to the fractional ownership structures, investor verification, and transparent payment records.

- Insurance– It automates claims workflows, reducing fraud exposure and maintaining auditable policy records.

None of these blockchain use cases requires blockchain to be present everywhere. They require it to be present where the integrity of a shared record is genuinely valuable, and where existing systems introduce risk or inefficiency that blockchain can credibly address.

What Are the Legal Regulations for Blockchain?

Regulations translate directly into product decisions, and understanding them early saves significant rework later:

KYC (Know Your Customer) sits at the foundation of most regulated blockchain deployments. Before granting users access to a platform, businesses must be able to confirm who those users actually are. This is what makes a platform defensible when regulators, auditors, or law enforcement come asking questions. Without reliable identity verification, everything built on top of it is exposed.

AML (Anti-Money Laundering) takes that a step further. Knowing who a user is matters less if the platform has no visibility into what they are doing. AML obligations require enterprises to monitor transaction activity on an ongoing basis, identify patterns that suggest financial crime, and report them through the appropriate channels. For blockchain platforms handling real financial flows, this needs to be a live capability.

Data Privacy is where blockchain’s core properties create a genuine tension. Immutable records are valuable for auditability, but privacy regulations like GDPR operate on the premise that individuals retain rights over their data. Enterprises cannot treat these as separate concerns. The architecture has to account for both, which means data privacy considerations need to be in the room when the data model is being designed.

Token Classification and Securities Law is frequently underestimated until it becomes a problem. Whether a token is treated as a security, a utility, or a commodity determines which regulatory framework applies, and that determination varies by jurisdiction. Getting it wrong does not just create legal exposure; it can fundamentally alter what the platform is permitted to do and who it can serve. Classification needs a legal opinion, not an assumption.

Licensing and Regulatory Approvals vary considerably by market; regulators are raising the bar for who can operate exchanges, custody services, and blockchain-based financial products. Launching without the right licenses is a business risk, not just a compliance one. Banking partners, institutional clients, and enterprise procurement teams increasingly treat licensing status as a prerequisite, not a follow-up item.

Regulated DeFi Is a Real Category Now

Two years ago, institutional interest in DeFi was largely exploratory. Today, banks, asset managers, and fintech firms are actively evaluating regulated decentralized finance (DeFi). What they need is programmable finance with compliance controls built into the architecture. Permissioned participant pools. Verified counterparties. Wallet screening before transactions settle. Smart contracts that have been audited. Governance frameworks with documented decision trails. Liquidity risk controls. Reporting that meets institutional standards.

For enterprises that want exposure to the efficiency gains of DeFi without the regulatory and reputational risk of uncontrolled protocols, this is where the opportunity sits.

The Work That Has to Happen Before Development Starts

The most expensive compliance mistakes in blockchain app development are architectural ones, decisions made early that become very difficult to unwind later. Choosing a data model that doesn’t support privacy regulation. Building transaction flows that weren’t mapped against Travel Rule obligations. Designing a token structure without confirming how it will be classified in target markets.

The groundwork that prevents these mistakes is not complicated, but it requires deliberate effort. Define the asset, the user journey, the custody model, the revenue structure, and the jurisdictions. Map the regulatory obligations attached to each element. Then give that map to the technical team before they write the first line of code.

The compliance stack that follows from that process of identity verification, AML screening, wallet monitoring, data privacy controls, smart contract permissioning, administrative governance, audit dashboards, incident response procedures, and reporting exports can then be designed as part of the product rather than bolted on afterward.

Conclusion

Compliance is not what slows blockchain projects down, but poor planning. Enterprises that treat regulatory requirements as constraints to work around tend to hit them hard and late. Those that build compliance into the platform architecture from the start find it considerably easier to enter regulated markets, maintain institutional relationships, and scale without disruption.

Partner with SoluLab To Build Blockchain for Regulatory Compliance!

Solulab has worked with enterprises across financial services, healthcare, supply chain, and digital assets to build blockchain platforms that meet these standards. Our company builds blockchain platforms that are designed for this reality- secure, auditable, and structured to meet the regulatory expectations of the markets enterprises actually want to operate in.The work includes compliant token platforms, KYC-integrated identity systems, regulated DeFi infrastructure, enterprise blockchain networks, smart contract audit workflows, and compliance dashboards built for real operational use.

FAQs

Shipra Garg is a tech-focused content strategist and copywriter specializing in Web3, blockchain, and artificial intelligence. She has worked with startups and enterprise teams to craft high-conversion content that bridges deep tech with business impact. Her work translates complex innovations into clear, credible, and engaging narratives that drive growth and build trust in emerging tech markets.