Banks and financial institutions are spending more on compliance than ever before. According to recent industry analysis, compliance now represents 2.9% to 8.7% of non‑interest expenses for banks, and for some firms, compliance and related costs can reach as high as 19% of annual revenue. This means that for a large global bank, the compliance budget can easily exceed $200 million per year, just to stay on the right side of regulators.

Compounding this cost pressure is the 60% increase in compliance operating costs since the pre-financial-crisis era, driven by heavier reporting, more frequent audits, and increasingly complex AML/KYC frameworks as many of which are now being reimagined through blockchain technology, smart contracts, and decentralized identity solutions.

At the same time, regulatory fines for financial‑crime‑related failures have surged; global enforcement penalties jumped 417% in the first half of 2025 alone, reaching $1.23 billion compared to $238.6 million in the same period of 2024.

Let’s see how blockchain compliance automation lowers costs, which use cases matter most, and how your firm can practically implement this, if you’re serious about reducing compliance costs in banking over the next 3–5 years.

Key Takeaways

- The problem: Compliance costs keep rising, while manual KYC and AML processes stay slow, fragmented, and expensive to run.

- The solution: Blockchain automation simplifies KYC, AML, and reporting by reducing manual work, cutting errors, and easing audit pressure.

- How SoluLab helps: SoluLab builds blockchain compliance automation with KYC, AML, and monitoring systems, which is designed to fit your regulatory setup and operational reality.

What is Blockchain Automation?

In simple terms, blockchain automation is the use of blockchain and smart contracts to run repetitive, rules‑based compliance tasks like checking identities, screening transactions, or generating audit reports without constant human intervention.

At its core, a blockchain is a shared, immutable ledger; every transaction or record is time‑stamped and cryptographically secured, so neither customers nor regulators need to trust the data, they just need to read it.

When you add smart contracts, the system can automatically enforce business‑logic rules, for example:

- If a customer’s ID is verified, issue a digital credential that other institutions can trust.

- If a transaction exceeds a certain threshold or hits a sanctions list, trigger an alert or freeze flag.

- If a regulatory report is due, automatically compile the required data from the ledger and send it to the relevant authority.

This kind of blockchain automation is especially powerful for compliance automation services that banks, fintechs, and crypto‑focused firms are now adopting.

Here is how Blockchain automation is utilised in every industry-

The Compliance Cost Problem in Banking and Financial Services

For many decision‑makers, the compliance budget is no longer a small line item – it’s a strategic cost center competing with product development, marketing, and international expansion.

Yet, the way most firms deliver compliance today is still deeply manual and fragmented.

- KYC and onboarding often require re‑checking identities at every institution, even when the same customer has already been verified elsewhere.

- AML systems rely on batch‑style transaction monitoring, long‑tail manual reviews, and error‑prone data entry, which together drive up labor‑intensive compliance costs.

- Regulatory reporting is mostly handled by separate teams, spreadsheets, and legacy tools, which not only raise costs but also increase the risk of mistakes and late submissions.

Studies show that KYC onboarding costs alone can reach $20–$30 per user, with average onboarding times of 3–10 days and dropout rates of up to 40% during the KYC phase.

Meanwhile, mid‑size and large banks are spending hundreds of millions of dollars annually on compliance, even though only a fraction of this is technology‑driven automation.

In this context, blockchain app development for compliance automation lowers costs not just by reducing headcount, but by eliminating redundant checks, shortening cycle times, and cutting the risk of regulatory fines.

How Blockchain Compliance Automation Lowers Costs in Financial Institutions?

When blockchain layers sit underneath compliance workflows, a lot of unnecessary work simply goes away. Not because it’s flashy, but because the system stops doing the same checks over and over.

1. Shared KYC and identity

It is the clearest example. Today, every institution re-verifies the same user, even when nothing has changed. With blockchain-based KYC, a customer can be verified once and reuse that proof elsewhere, as long as they consent.

In practice, this often drops onboarding costs from roughly $20–$30 per user to about $3–$5, while cutting onboarding time from days to minutes and reducing duplicated checks.

2. AML and transaction monitoring

It has become cheaper because they’re no longer driven by noisy, rule-based alerts. Blockchain monitoring reads transactions directly from the ledger in real time and flags risky patterns on-chain.

When paired with AI-driven risk management, teams spend less time on false positives, which can make up close to 40% of alerts and more time on real risk, lowering headcount and investigation costs.

3. Audits get simpler too.

Instead of reconciling data across systems, transactions and identity events live on an immutable, time-stamped ledger. Auditors can trace activity directly, reports are generated automatically, and firms rely less on manual checks and external consultants. Over time, that’s where a large part of compliance cost savings actually show up.

Real-World Implementation of Blockchain Compliance Automation Lowering Costs in Banking

1. Blockchain for AML and KYC Automation

Many institutions are now using blockchain for AML compliance and KYC automation to connect identity verification, sanctions screening, and transaction monitoring into a single flow.

For example:

- A fintech using blockchain KYC solutions can verify a customer once, issue a tamper‑proof digital credential, and share only the necessary attributes (e.g., KYC status, risk score) with partner banks or exchanges.

- A crypto‑first bank or VASP can integrate blockchain analytics tools to screen wallet addresses in real time, reducing the risk of onboarding illicit actors.

This approach strengthens role of blockchain in AML and KYC automation, while also reducing the cost of each verification and every subsequent check.

2. Blockchain for Cross‑Border Payments

In 2025 alone, blockchain‑enabled stablecoins and payment rails have reduced cross‑border transaction costs by up to 96%, with average settlement times under 10 mins.

From a compliance perspective, this matters because:

- Funds move faster and with full on‑chain traceability, which makes it easier to monitor and report.

- Blockchain compliance automation can be built directly into payment rails, so sanctions screening and beneficiary checks happen automatically before settlement.

3. Blockchain Compliance Management System

In 2025, leading financial firms are moving toward blockchain compliance management systems that combine:

- KYC/AML workflows

- Real‑time transaction monitoring

- Regulatory‑reporting modules

all sitting on a shared blockchain‑based infrastructure.

Such systems typically deliver:

- Stronger financial compliance automation

- Lower manual effort in both front‑office (onboarding) and back‑office (reporting)

- A clear path to blockchain compliance automation ROI for banks as they scale.

Quantifying Cost Savings Through Blockchain Compliance Automation

Several industry reports suggest that blockchain compliance automation can lower costs by 20–50%, depending on the use case and maturity of the organization.

For example:

- Surveys show that institutions using blockchain‑based KYC/AML solutions report around 50% reductions in compliance‑related costs while improving accuracy and audit‑readiness.

- AI‑driven blockchain compliance tools can cut manual labor costs by 30–32%, reduce consultancy and auditing expenses by about 24%, and lower data storage and maintenance costs by roughly 25–30%.

From a CFO’s perspective, the equation is simple:

- Traditional compliance costs are rising at 60%+ compared to pre‑financial‑crisis levels.

- Blockchain compliance automation offers a credible path to reduce compliance costs in banking by 20–50%, depending on how deeply you integrate automation into KYC, AML, and reporting.

How Blockchain Compliance Automation Lowers Costs vs Traditional Financial Compliance?

Here’s how the two models compare in practice

| Aspect | Traditional Compliance | Blockchain Compliance Automation |

|---|---|---|

| Identity checks | Re‑done at every institution, high cost per user ($20–$30) | Verified once, reusable credentials, cost often drops to $3–$5/user |

| Transaction monitoring | Batch‑style, many false positives, heavy manual review | Real‑time, AI‑enhanced, fewer false positives, lower labor cost |

| Reporting | Manual, fragmented, error‑prone | Automated, audit‑ready, single‑source‑of‑truth |

| Audit process | Time‑consuming, relies on spreadsheets and disparate systems | Fast, based on immutable ledger and smart‑contract‑driven reports |

| Overall cost posture | High, rising | Lower, with clear blockchain compliance automation ROI for banks |

From a blockchain development cost vs traditional compliance cost comparison standpoint, the data shows that blockchain compliance automation lowers costs while improving both speed and transparency

Challenges and Best Practices in Blockchain KYC and AML Compliance Automation

Of course, moving to blockchain-based compliance automation isn’t something you turn on overnight. It usually starts with friction.

- Regulations still vary by region, and what’s acceptable for blockchain digital identity or blockchain-driven KYC in one country may not pass in another, which forces teams to design with multiple rulebooks in mind.

- On top of that, most banks and fintechs are running on legacy systems that were never built for blockchain-first workflows, so integrations with existing KYC, AML, and core banking tools can get messy before they get better.

- Then there’s data privacy. Even with blockchain, firms still have to respect GDPR, local data-protection laws, and internal governance, which means being deliberate about what goes on-chain and what stays off-chain.

The teams that get this right usually don’t try to boil the ocean.

- They start small, often with high-cost, high-volume areas like KYC onboarding or cross-border payments, where automation shows value quickly.

- They work with a blockchain development and consulting partner who understands financial compliance and has experience dealing with regulators or sandbox environments, because theory alone doesn’t survive real audits.

- Most importantly, they design for compliance from day one. When compliance logic is built directly into the architecture, instead of added later as a patch, automation actually reduces risk rather than creating new blind spots.

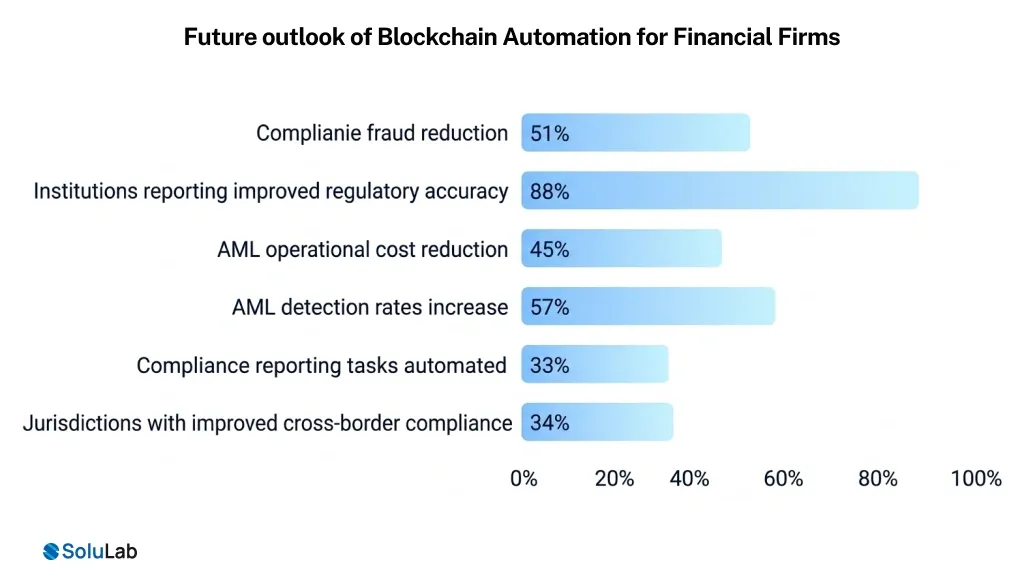

Future outlook of Blockchain Automation for Financial Firms

If you look ahead to 2026 and beyond, a few things are becoming pretty clear, especially if you’re close to compliance, ops, or product.

First, blockchain compliance SaaS is starting to feel less experimental and more inevitable. More vendors are rolling out cloud-based, API-first platforms that bundle KYC, AML, and transaction monitoring into one stack, which matters because teams are tired of stitching five tools together just to stay compliant.

At the same time, the blockchain vs traditional compliance cost gap is getting harder to brush off. As more firms publish real numbers, especially global banks and fintechs, the cost advantage of blockchain-based compliance isn’t theoretical anymore, it’s showing up in budgets, headcount, and audit timelines.

And finally, there’s real pressure at the board level. CFOs and compliance heads are being judged not just on staying safe, but on how effectively they reduce compliance costs in banking without risking regulatory trust.

That’s where automation stops being a nice to have and starts becoming a requirement.

How SoluLab Helps You Build and Deploy Blockchain Compliance Automation?

If you’re serious about reducing compliance costs in banking while maintaining regulatory rigor, you need more than off‑the‑shelf tools, you need custom‑built blockchain solutions integrated with your existing infrastructure. That’s where SoluLab comes in.

As a blockchain consulting company, SoluLab can:

- Map your current compliance workflow and identify the highest‑cost bottlenecks where blockchain compliance automation lowers costs the most.

- Design a roadmap from manual KYC/AML processes to blockchain‑based KYC automation, blockchain for AML compliance, and blockchain financial monitoring systems.

- Help you hire blockchain developers from our team or guide your internal hiring strategy so you can scale your in‑house capabilities without over‑engineering early on.

This kind of end‑to‑end support is why firms turning to us don’t just end up with a proof of concept they can’t maintain, they end up with a production‑ready, audit‑ready blockchain compliance stack that directly contributes to reducing compliance costs in banking and improving blockchain compliance automation ROI for banks.

Conclusion

Regulators are not going to slow down; if anything, they’re adding more layers of KYC, AML, and reporting requirements, especially in the crypto and cross‑border payment space. At the same time, markets are rewarding firms that can reduce compliance costs in banking without sacrificing safety or transparency.

Blockchain automation, especially blockchain compliance automation, blockchain KYC automation services, and blockchain financial monitoring systems is emerging as one of the most credible ways to achieve that balance. It lets you:

- Cut redundant KYC checks and onboarding time while improving conversion.

- Automate AML and transaction monitoring, reducing manual work and false positives.

- Create audit‑ready, immutable records that satisfy both internal and external auditors.

This is why blockchain compliance automation lowers costs in a way that’s measurable, repeatable, and aligned with the direction of global regulation.

If you’re a founder or head of compliance at a bank, fintech, or crypto-native firm, the real question is no longer whether to explore blockchain-driven compliance—it’s how fast you can move, how effectively you can integrate it into your existing stack, and whether you have the right expertise or need to hire blockchain developers to implement scalable, cost-efficient solutions without over-engineering or over-budgeting.

FAQs

With over 3 years of experience, I specialize in breaking down complex Web3 and crypto concepts into clear, actionable content. From deep-dive technical explainers to project documentation, I help brands educate and engage their audience through well-researched, developer-friendly writing.