Key Takeaways

- Banking is shifting from static workflows to real-time decisions.

- Agentic AI orchestration for banking connects data, decisions, and actions across systems.

- The focus is on intelligent decision flows in banking, not linear processes.

- Strong systems rely on data layers, decision engines, agents, and orchestration.

- Key use cases include credit, fraud, AML, and customer intelligence.

- AI-driven banking operations need built-in governance and auditability.

- Regulatory alignment, including the EU AI Act, is essential.

- Most banks follow a hybrid build vs partner approach, using AI agent development services.

- Implementation works best through phased rollout and scalable infrastructure.

- This shift leads to autonomous financial decision systems.

Banking was never meant to run on static workflows; it just adapted to them.

For decades, financial institutions have relied on rule engines and predefined processes to manage everything from credit approvals to fraud detection. But today’s reality is fundamentally different. Decisions are no longer linear, data is no longer static, and risk is no longer predictable. Every transaction, customer interaction, and market signal demands real-time interpretation and action.

This is where AI in banking begins to reshape the system.

Instead of automating steps, banks are now moving toward AI decision automation in banking systems that can interpret context, reason across variables, and execute actions autonomously. The focus is shifting from workflows to intelligent decision flows in banking, where outcomes are continuously optimized rather than predefined.

The question is no longer how to automate processes but how to orchestrate decisions.

What is Agentic AI Orchestration in Banking?

At its core, agentic AI orchestration for banking is not about deploying smarter models – it’s about coordinating systems that can think, decide, and act within defined boundaries.

Traditional AI in banking has largely been predictive: models score risk, detect anomalies, or recommend actions. But agentic AI in banking introduces a new layer – AI agents that can independently interpret context, choose actions, and interact with other systems or agents to complete tasks.

To understand this, it helps to break the stack into three distinct layers:

- AI Models → Generate predictions (e.g., credit risk scores, fraud probabilities)

- AI Agents → Use those predictions to make decisions and take actions

- Orchestration Layer → Coordinates multiple agents, data sources, and workflows into a unified decision system

This orchestration layer is what transforms isolated intelligence into intelligent decision flows in banking.

For example, a loan approval is no longer a sequence of checks; it becomes a coordinated process where multiple agents:

- Evaluate borrower risk

- Cross-check compliance requirements

- Adjust pricing dynamically

- Trigger approvals or escalations

All in real time.

This is where AI orchestration platforms for banks play a critical role. They provide the infrastructure to manage:

- Multi-agent interactions

- Context sharing across systems

- Decision sequencing and governance

The result is not just automation but AI-powered decision intelligence for banks, where systems continuously adapt to new data, regulatory constraints, and business objectives.

In this model, artificial intelligence is no longer embedded in isolated models, it is orchestrated across the entire banking system.

Why Traditional Banking Automation is Failing?

For years, banks have invested heavily in automation, but most of it was designed to optimize processes, not decisions.

Rule engines, BPM tools, and workflow systems brought efficiency, but they were built for a world where conditions were predictable, and exceptions were rare. Today, that assumption no longer holds. Financial environments are dynamic, customer behavior is volatile, and regulatory expectations are continuously evolving.

The cracks are now visible.

- Rule-based systems don’t scale with complexity

Every new condition requires another rule, creating fragile, hard-to-maintain systems - Static workflows can’t adapt in real time

They follow predefined paths, even when context changes mid-process - Decision latency is increasing

Critical decisions still rely on manual reviews or disconnected systems - Siloed intelligence limits impact

Fraud models, credit models, and compliance systems operate independently, without shared context

As a result, banks end up automating steps—but not improving outcomes.

What’s missing is a system that can interpret context across multiple dimensions—risk, compliance, customer behavior, and market signals—simultaneously. This is why institutions are shifting toward AI-powered decision intelligence platforms, where decisions are not pre-coded but dynamically generated.

The transition toward AI-driven banking operations is less about replacing workflows and more about rethinking how decisions are made, coordinated, and executed at scale.

From Workflows to Intelligent Decision Flows?

Traditional banking automation is built on workflows. A request enters the system, moves through predefined steps, and exits with an outcome. This structure works when scenarios are predictable and inputs are stable.

But modern banking does not operate in that environment anymore.

What’s emerging instead are intelligent decision flows in banking. These are not fixed paths but adaptive systems where each step depends on real-time context. Decisions are continuously recalibrated based on new data, changing risk signals, and evolving regulatory constraints.

The difference is structural:

- Workflows execute instructions

- Decision flows evaluate situations

In a workflow, a loan application follows a sequence of checks. In a decision flow, multi AI agent system evaluates the application simultaneously, adjusting risk scores, pricing, and compliance flags as new information becomes available.

This shift enables:

- Real-time decisioning instead of delayed approvals

- Continuous learning from outcomes

- Dynamic prioritization of risk and opportunity

For example, in fraud detection, a static system flags transactions based on predefined rules. In an AI-driven banking operation, agents continuously analyze behavior patterns, transaction context, and network signals to decide whether to block, approve, or escalate a transaction instantly.

This is where AI workflow automation in banking evolves into something more powerful. It becomes a system that does not just move data forward but actively interprets and acts on it.

The result is a banking model where decisions are not steps within a process. They are the process itself.

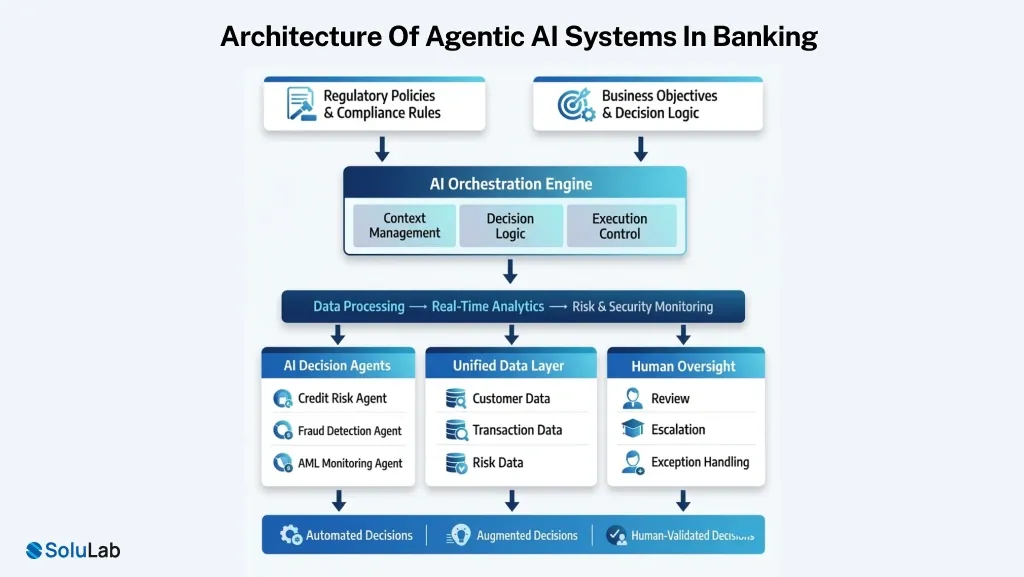

Architecture of Agentic AI Systems in Banking

To move from automation to decision intelligence, banks need more than models.

They need a structured system that can coordinate data, reasoning, and execution in real time.

At the core of agentic AI orchestration for banking is a layered architecture designed to support continuous, context-aware decisioning.

1. Data and Context Layer

This layer aggregates and normalizes data from across the bank:

- Core banking systems

- Transaction streams

- Customer profiles

- External data sources

The goal is to create a unified, real-time context. Without this, even the most advanced models operate in isolation.

2. Decision Engine Layer

This is where AI decision engines for banks operate. It combines:

- Machine learning models

- Business constraints

- Risk and compliance rules

Instead of producing a single output, the engine evaluates multiple possible actions and their implications.

3. Agent Layer

AI agents sit on top of decision engines and are responsible for:

- Interpreting outputs

- Taking actions

- Interacting with other agents

For example, a credit agent may coordinate with a compliance agent before finalizing a decision.

4. Orchestration Layer

This is the backbone of the system. It manages:

- Multi-agent coordination

- Task sequencing

- Context sharing across decisions

This is where banking AI agent orchestration becomes critical. Without orchestration, agents remain disconnected and decisions become inconsistent.

5. Execution Layer

The final layer connects decisions to real systems:

- Payment systems

- Loan management platforms

- Fraud prevention tools

- Customer communication channels

Actions are executed through APIs and integrated services in real time.

Key Use Cases of Agentic AI in Banking

From all the AI use cases popular among, the real value of agentic AI in banking becomes visible when applied to high-stakes, decision-heavy functions. These are areas where speed, accuracy, and context directly impact revenue, risk, and compliance.

These use cases reflect how agentic AI banking solutions are moving from experimentation into production across core functions.

- Credit Decisioning

Traditional underwriting relies on sequential checks and static risk models. With AI decision automation in banking, agents can:

- Continuously reassess borrower risk

- Adjust pricing dynamically

- Incorporate alternative data sources

Hence, the use of AI for underwriting leads to faster approvals and more accurate risk segmentation.

- Fraud Detection and Prevention

Fraud systems have historically been reactive. Agentic systems shift this to real-time decisioning:

- Analyze transaction context, user behavior, and network signals simultaneously

- Decide whether to approve, block, or escalate instantly

This is a core example of AI-driven banking operations where decisions must happen in milliseconds.

- AML and Compliance Automation

Compliance processes are complex and resource-intensive. With AI workflow automation in banking, agents can:

- Monitor transactions continuously

- Flag suspicious patterns dynamically

- Generate audit-ready reports

This improves both efficiency and regulatory alignment.

- Customer Intelligence and Personalization

Banks sit on vast amounts of customer data, but rarely use it in real time. Agentic systems enable:

- Context-aware product recommendations

- Dynamic engagement strategies

- Personalized financial insights

This AI solution transforms customer experience from reactive to proactive.

- Treasury and Liquidity Management

Liquidity decisions depend on multiple moving variables. Agentic AI can:

- Predict cash flow requirements

- Optimize fund allocation

- Adjust strategies based on market signals

This creates more resilient and adaptive financial operations.

Across these AI agent use cases, the common pattern is clear. Banks are no longer just automating tasks. They are building intelligent decision flows in banking that continuously evaluate, adapt, and act.

This is what turns isolated automation into a coordinated, system-wide capability.

Operating Model and Risk & Compliance Foundations

Designing agentic AI orchestration for banking is one challenge. Running it in a regulated environment is another.

Banks are not just deploying AI solutions; they are introducing systems that actively make decisions. That changes how operations, risk, and control functions are structured.

- Defining Levels of Autonomy

Not every decision should be treated the same.

In practice, banks segment decisions based on risk:

- Low-risk → fully automated (e.g., transaction approvals within limits)

- Medium-risk → AI-led with human validation

- High-risk → human-led with AI support

This layered approach keeps control intact while still enabling AI decision automation in banking.

- Embedding Governance into the System

Governance cannot sit outside the system. It has to be built into it.

That means:

- Policy constraints are part of the decision logic

- Approval thresholds are coded into workflows

- Escalation paths are predefined and traceable

Instead of reviewing decisions after the fact, the system enforces rules in real time.

- Auditability as a Core Requirement

Every decision needs a trail.

Banks must be able to answer:

- What data was used?

- Which model influenced the outcome?

- Why was this decision taken?

This is where AI decision engines for banks need to go beyond prediction and support full traceability. Logs, versioning, and decision histories become critical infrastructure.

- Managing Bias and Model Drift

AI systems change over time. So does their behavior.

To manage this, banks typically introduce:

- Continuous monitoring of outputs

- Periodic model validation

- Alerts for unusual decision patterns

This ensures that AI-driven banking operations remain stable and fair across different customer segments.

- Aligning with Regulatory Expectations

Regulation is evolving alongside AI adoption.

Frameworks like the EU AI Act and existing banking guidelines are pushing for:

- Transparent decision-making

- Clear accountability structures

- Strong data governance

Systems that are not designed with these expectations in mind often face delays at deployment stages.

What This Means in Practice?

Operating agentic systems is less about automation and more about control.

Banks that succeed here treat compliance, monitoring, and governance as part of the architecture itself. Not as an afterthought.

That is what allows intelligent decision flows in banking to move from pilot environments into real, production-grade systems.

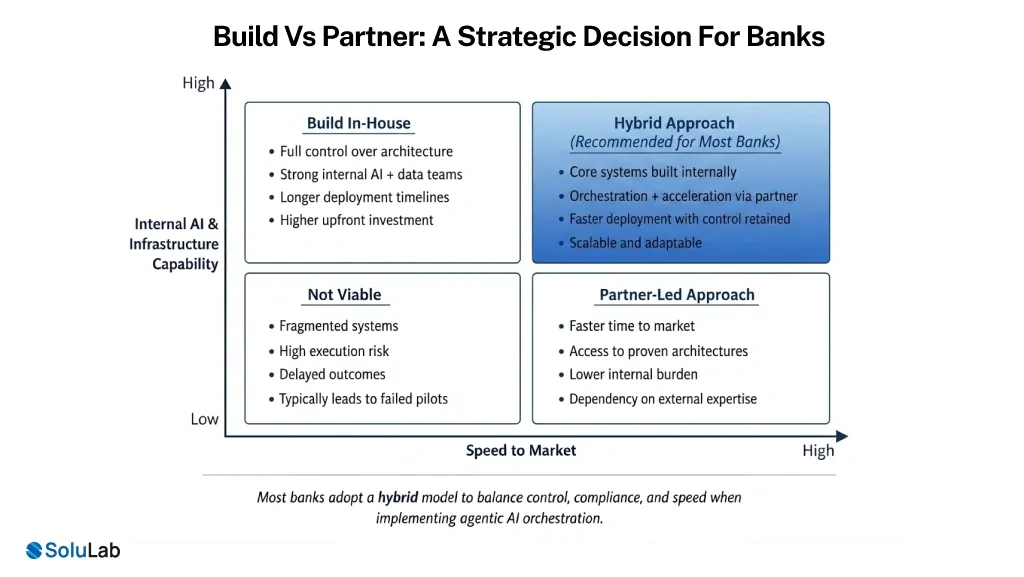

Build vs Partner: A Strategic Decision for Banks

Adopting agentic AI frameworks often starts as a technology discussion. It quickly turns into an infrastructure and capability question.

Most banks prefer to build internally. Control over data, models, and systems is a strong incentive. It also aligns with long-term digital transformation goals.

But the challenge shows up in execution.

Where Complexity Builds Up?

What looks manageable at the model level becomes harder at the system level:

- Coordinating multiple AI agents across functions

- Maintaining real-time data consistency

- Designing decision flows that remain stable under edge cases

- Ensuring every action is logged and explainable

Each layer adds operational overhead. Over time, this slows down deployment and increases risk.

The Compliance Layer Changes Everything!

In regulated environments, speed alone is not enough.

Systems must support:

- Audit trails for every decision

- Model monitoring and version control

- Policy enforcement within decision flows

This is where many in-house efforts struggle. The system works technically, but fails to meet compliance expectations.

What Experienced Partners Bring?

Many banks evaluate external AI agent development services to accelerate implementation while maintaining architectural control.

Common patterns include:

- Phased rollout instead of full-scale deployment

- Clear separation between decision logic and governance layers

- Architecture designed for auditability from day one

A professional AI development company, such as SoluLab, has deep-rooted expertise in compliance and scalability. The emphasis is on making systems production-ready, not just functional.

How Banks Typically Decide?

The decision is rarely binary.

A common approach:

- Build core capabilities internally

- Partner for orchestration, architecture, or acceleration

This allows banks to retain control while reducing execution risk.

What Matters Most?

The real question is not whether to build or partner.

It is whether the system can:

- Scale across use cases

- Adapt to regulatory changes

- Maintain consistency in decision-making

That is what ultimately defines the success of AI-driven banking operations.

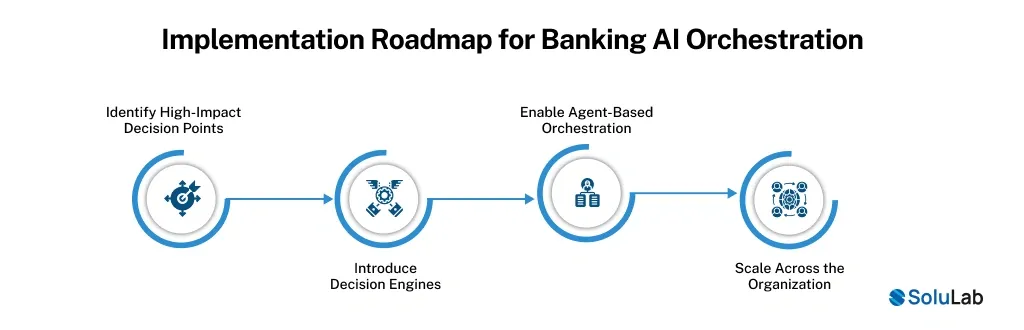

Implementation Roadmap for Banking AI Orchestration

Most banks do not fail because of poor models. They fail because they try to scale too early or without the right structure.

Implementing agentic AI orchestration for banking works best as a phased progression.

Phase 1: Identify High-Impact Decision Points

Start small, but start where decisions matter.

Typical entry points:

- Credit approvals

- Fraud detection

- AML monitoring

The goal is to introduce AI decision automation in banking in controlled environments where outcomes are measurable.

Phase 2: Introduce Decision Engines

Once use cases are defined, the next step is to move beyond isolated models.

This involves:

- Connecting models to real data pipelines

- Embedding business and compliance constraints

- Creating decision logic that can evolve over time

At this stage, banks begin building AI decision engines for banks that go beyond prediction.

Phase 3: Enable Agent-Based Orchestration

With decision engines in place, orchestration becomes the focus.

This is where:

- Multiple agents interact across functions

- Decisions are coordinated instead of siloed

- Context is shared across systems

This step transforms isolated automation into intelligent decision flows in banking.

Phase 4: Scale Across the Organization

Scaling is not about adding more models. It is about extending the system across domains.

Key priorities:

- Standardizing data and context layers

- Expanding governance frameworks

- Ensuring consistency across decision flows

This is where AI native strategy begins to take shape at an enterprise level.

Technology Foundations That Support This Journey

Across all phases, certain capabilities remain critical:

- Real-time data infrastructure

- API-driven system integration

- Model monitoring and observability

- Scalable orchestration frameworks

Without these, systems remain fragmented and difficult to scale.

Conclusion: The Shift Toward Autonomous Banking Systems

Banking is moving from process execution to real-time decisioning.

Agentic AI orchestration for banking enables systems that can interpret context, coordinate actions, and operate within regulatory boundaries. The advantage lies in how well institutions connect data, decision engines, and governance into a unified framework.

This is not a model upgrade. It is a shift in how decisions are made at scale.

Banks that treat this as infrastructure, not experimentation, will be better positioned to build resilient, adaptive, and truly intelligent operations.

SoluLab, a leading AI integration service provider, brings expertise in building AI orchestration layers, decision engines, and compliance-ready architectures that can operate reliably in regulated banking environments.

FAQs

Shipra Garg is a tech-focused content strategist and copywriter specializing in Web3, blockchain, and artificial intelligence. She has worked with startups and enterprise teams to craft high-conversion content that bridges deep tech with business impact. Her work translates complex innovations into clear, credible, and engaging narratives that drive growth and build trust in emerging tech markets.