Key Takeaways

- The “Last Mile” Solution: Stable cards bridge the gap between digital assets and real-world utility, enabling instant PoS transactions.

- Yield-on-Spend: Enterprises can maintain capital in yield-bearing DeFi protocols until the exact millisecond of a transaction.

- Regulatory Clarity: Frameworks like the US GENIUS Act and Canada’s Bill C-15 have de-risked stablecoin cards for institutional use.

- Native Settlement: The shift from “off-ramping” to on-chain settlement via networks like Visa and Stripe (Bridge).

Finance teams could move millions in USDC within seconds, yet paying vendors, SaaS invoices, travel expenses, or contractor payroll still required off-ramping into legacy banking systems.

That friction created a gap between digital finance and real-world commerce.

In 2026, that gap will finally disappear through stablecoin development solutions like stablecoin-linked debit/credit cards… Instead of converting stablecoins into fiat days before spending, businesses can keep treasury funds on-chain, earn yield continuously, and settle transactions in real time through stablecoin debit cards.

Visa and Stripe-owned Bridge are expanding stablecoin settlement infrastructure across more than 100 countries. Western Union has entered the ecosystem through the Western Union stablecoin initiative and the Western Union USDPT rollout. Meanwhile, governments in the United States, Canada, and the UAE are introducing frameworks that make institutional adoption possible at scale.

Why Are Stablecoin-Linked Debit/Credit Cards Becoming a Treasury Tool for Enterprises?

The biggest reason enterprises are adopting stablecoin-based payment cards is simple: idle capital is expensive.

Traditional corporate banking leaves treasury funds sitting in low-yield accounts while inflation, FX exposure, and banking delays reduce efficiency. Stable coins and cards completely change that model.

Today, enterprises can keep treasury reserves in tokenized money market funds, DeFi vaults, or yield-generating stablecoin protocols earning 5%–8% APY. With Stablecoin cards, those funds only convert at the exact moment a transaction occurs.

1. Real-time liquidity management

Instead of pre-funding multiple bank accounts across countries, businesses can operate from a unified stablecoin treasury.

2. Instant vendor settlement

Global vendors receive payments within seconds instead of waiting through SWIFT settlement cycles.

3. Reduced FX dependency

Companies dealing with Latin America, Africa, or Southeast Asia avoid volatile local currency exposure.

4. Programmable spending controls

Enterprises can issue employee cards with smart contract restrictions tied to:

- Geography

- Merchant category

- Spending limits

- Subscription approvals

- Vendor-specific usage

This level of automation is why many fintech firms are partnering with a Stablecoin development company to build internal treasury systems directly connected to corporate spending cards.

The result is a payment infrastructure where money remains productive until the exact millisecond it gets spent.

How Is the Western Union USDPT Launch Changing Cross-Border Payments?

The biggest validation for the market came when legacy remittance players stopped resisting blockchain technology and started integrating it directly.

The USDPT stablecoin launch by Western Union marked one of the strongest signals that stablecoin infrastructure had become commercially unavoidable.

Rather than treating blockchain as an external settlement layer, Western Union integrated Western Union USDPT into its remittance operations to reduce settlement delays and liquidity costs.

Why this matters globally?

Previously, remittance flows looked like this:

Sender → Bank → Intermediary Bank → FX Conversion → Local Settlement → Receiver

That process could take 2–5 business days.

Now, the Western Union Stable Card ecosystem enables the following:

- Instant remittance settlement

- 24/7 cross-border transfers

- Stablecoin-native spending

- Direct merchant payments

- Reduced intermediary banking fees

In regions like Argentina, Colombia, and Mexico, this has become especially important.

Citizens are increasingly using stablecoin-linked debit/credit cards to hold savings in USD-backed digital assets while continuing to spend locally in pesos. For many families and freelancers, stablecoins are becoming more practical than local banking products.

Western Union’s move also created pressure on fintech competitors, accelerating the broader stablecoin-linked card expansion happening across emerging markets.

Why Are Stablecoin Credit Cards Becoming Important for Global Liquidity?

The next evolution is not debit infrastructure. It is a credit infrastructure.

Stablecoin credit cards is introducing a model where enterprises use tokenized assets as collateral while maintaining ownership of their treasury positions.

That changes corporate finance in several important ways.

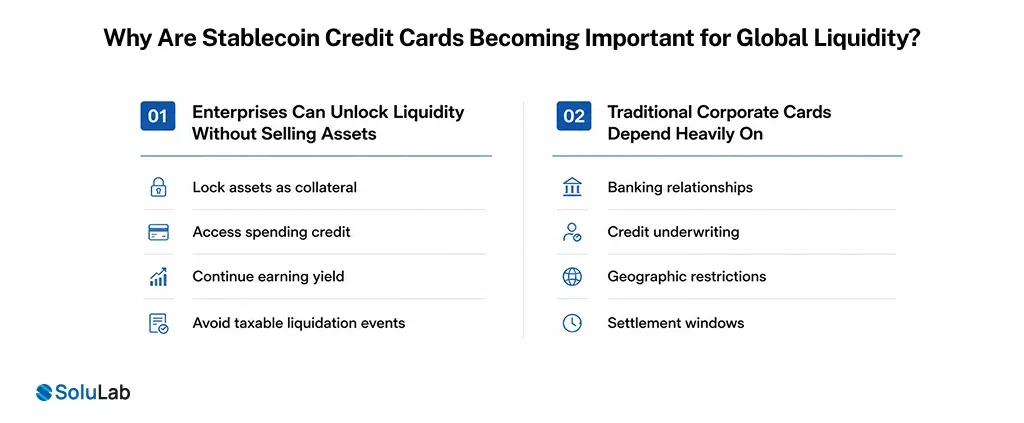

1. Enterprises no longer need to liquidate core holdings

Instead of selling stablecoins or tokenized RWAs to fund operations, companies can:

- Lock assets as collateral

- Access spending credit

- Continue earning yield

- Avoid taxable liquidation events

This is becoming increasingly attractive for:

- Web3 startups

- Remote-first businesses

- Global SaaS companies

- AI infrastructure firms

- Digital asset funds

Platforms like Rain are already building vertically integrated systems where crypto payment cards for everyday transactions settle directly through Visa infrastructure while remaining connected to on-chain liquidity.

2. Why Enterprises are paying attention

Traditional corporate cards depend heavily on:

- Banking relationships

- Credit underwriting

- Geographic restrictions

- Settlement windows

By contrast, a stablecoin debit card for global payments infrastructure allows businesses to operate globally from day one without waiting months for international banking approvals.

That flexibility is becoming essential for modern distributed companies.

How Are the US GENIUS Act and Canada’s Bill C-15 Accelerating Stablecoin Cards Development?

Regulation was once the biggest reason enterprises hesitated to adopt stablecoin infrastructure.

That changed dramatically after the US passed the GENIUS Act in 2025.

The legislation created a legal framework treating payment stablecoins as regulated digital cash rather than speculative securities. For institutions, this reduced uncertainty around issuing and operating stablecoin-based payment cards for consumers and businesses.

1. What changed after the GENIUS Act?

1.1 Banks gained regulatory clarity

Financial institutions could now custody and interact with stablecoins under clearer compliance rules.

1.2 Fintech issuance accelerated

Companies like Ramp and Rain expanded corporate card offerings connected directly to USDC treasuries.

1.3 Treasury operations modernized

Startups began paying:

- AWS invoices

- Ad spend

- Payroll

- SaaS subscriptions

directly through Stablecoin cards.

2. The Canadian Market

Under Bill C-15, Canada officially authorized oversight of stablecoin issuers, creating legal pathways for fintech innovation across North America.

Canadian enterprises dealing with US suppliers immediately saw the opportunity to reduce:

- FX conversion costs

- Settlement delays

- Banking intermediary fees

As a result, demand for enterprise integrations through a Crypto Payment Gateway Development Company increased significantly during early 2026.

Which Countries and Companies Are Leading Stablecoin-Linked Card Expansion?

The global rollout is not happening evenly. Adoption is strongest where existing financial systems are either expensive, slow, or inflation-prone.

1. Latin America

Latin America remains the largest real-world usage market for stablecoin debit cards.

Countries leading adoption include:

- Argentina

- Colombia

- Mexico

- Peru

- Chile

High inflation and currency instability pushed both consumers and enterprises toward USD-backed stablecoins.

Businesses now use stablecoin-based payment cards for:

- Contractor payouts

- Import settlements

- Remote payroll

- International subscriptions

2. Europe

Europe’s MiCA framework gave enterprises confidence to adopt a regulated stablecoin payment infrastructure.

Companies like Circle and BVNK are aggressively building compliant payment ecosystems around Stablecoin Credit Cards and euro-backed settlement networks.

3. Middle East

Dubai has rapidly positioned itself as a stablecoin infrastructure hub.

The launch of AE Coin, a licensed dirham-backed stablecoin, accelerated enterprise adoption of stablecoin-linked debit/credit cards across the UAE fintech sector.

Read more- dirham-backed stablecoin

4. Infrastructure companies shaping the market

Bridge (Stripe): Building global settlement infrastructure connecting stablecoins directly to Visa rails.

Rain: Leading enterprise-grade stablecoin corporate card programs.

Circle: Expanding the Circle Payments Network for compliant global settlements.

MetaMask and Phantom: Integrating non-custodial “card-as-a-service” features for direct wallet spending.

This ecosystem growth is making stablecoin spending feel increasingly invisible to end users.

Is Security the Biggest Challenge for Stablecoin-Based Payment Card Services?

Security is no longer optional for enterprise adoption.

The first generation of crypto cards relied heavily on custodial exchanges. Businesses had to trust centralized platforms to hold funds before transactions occurred.

That model created major risks. The new generation of stablecoin-based payment cards operates differently.

1. Non-custodial spending is becoming the standard

Instead of transferring treasury assets into a card provider’s custody:

- Funds remain in enterprise-controlled wallets

- Smart contracts authorize transaction spending

- Settlement happens only during card usage

- Enterprises maintain direct asset ownership

This drastically reduces counterparty risk.

2. Additional security features to include in your stablecoin cards platform

2.1 Real-time transaction monitoring

AI-based fraud systems flag abnormal spending instantly. This can cut 80% of your costs without any effort. A proper feature is all you need.

2.2 Smart contract permissions

Finance teams can control:

- Merchant access

- Spending categories

- Daily limits

- Geographic restrictions

2.3 Multi-signature treasury approvals

Large transactions require internal authorization before execution.

For enterprises operating globally, these protections are becoming critical components of treasury infrastructure.

This is why many businesses are now working closely with a Stablecoin platform development company to build secure internal payment ecosystems tailored to enterprise workflows.

Conclusion

For enterprises planning long-term treasury modernization, Stable Cards are the next operational standard. To achieve this, you need a partner like SoluLab, which provides cryptocurrency development services, including CBDC and stablecoins that enhance the

- yield retention,

- programmable spending,

- real-time settlement,

- global accessibility,

- and reduced dependence on legacy banking rails.

As Visa, Stripe-owned Bridge, Circle, Rain, and Western Union continue expanding global infrastructure, the distinction between traditional banking and on-chain finance is beginning to disappear.

This is high time you adopt these features into your system. Contact us today and stay at the top of the race in the $320.6 billion stablecoin market

FAQs

Deepika is a content writer who blends storytelling with strategic thinking. She explores topics across digital innovation, emerging tech, and the evolving blockchain industry. She enjoys breaking down complex ideas into simple, engaging narratives in the growing global markets.