Key Takeaways

- Tokenization for boutique investment banks can reduce settlement timelines by up to 60%, improving deal execution speed and post-trade efficiency.

- Fractional digital issuance can expand investor reach by 2x–3x, especially across family offices and cross-border accredited investors.

- Partnering with an asset tokenization development company like SoluLab accelerates go-to-market while reducing technical and compliance risk.

Boutique Investment Banks are now seeing the balance sheet size of global bulge-bracket firms. But they do have something equally powerful: agility.

This is where tokenization in investment banking becomes strategic. By using blockchain infrastructure to digitally represent ownership of assets, boutique firms can design flexible, fractional, and programmable securities. This allows them to create new structures, access wider investor pools, and reduce settlement friction.

Industry research from major consulting firms estimates that asset tokenization could represent a multi-trillion-dollar value by the end of this decade. That signals a structural shift, not a trend.

The question is no longer whether tokenization matters. The question is how boutique banks can use it intelligently.

Why Does Tokenization Matter for Boutique Investment Banks?

Traditional deal structuring often involves multiple intermediaries, manual reconciliations, and long settlement cycles. Blockchain in banking introduces programmable securities and near real-time settlement.

Tokenized securities can:

- Automate dividend and coupon payments

- Embed transfer restrictions directly into smart contracts

- Reduce post-trade reconciliation

For boutique firms, this lowers operational overhead while maintaining regulatory compliance.

1. Expanding Investor Access

Tokenization allows fractional ownership. Instead of a $10 million minimum ticket, deals can be structured in smaller digital units.

This opens doors for:

- Family offices

- Smaller institutional investors

- Cross-border accredited investors

Tokenization for Capital Raising enables boutique banks to reach investor segments that were previously inaccessible due to high minimum thresholds.

2. Competing Without Scale

Large banks compete on distribution networks. Boutique Investment Banks can compete on innovation.

A strong Boutique investment bank tokenization strategy allows them to:

- Offer differentiated deal structures

- Shorten execution timelines

- Provide transparency and digital reporting

In many cases, being faster and more flexible becomes a competitive advantage.

Are Best Suited for Tokenized Deals and How Can Banks Structure Them?

Not every asset benefits equally from tokenization. Boutique banks should focus on where blockchain technology adds measurable value.

1. Private Credit

Private credit has grown significantly in the past decade, crossing over a trillion dollars globally. However, it remains operationally complex.

Tokenized private credit structures can:

- Digitally represent loan participation

- Automate coupon payments

- Enable partial secondary transfers

This makes it one of the most promising use cases for asset tokenization in investment banking.

2. Real Estate and Infrastructure

Real estate tokenization allows fractional ownership of income-generating properties.

Boutique firms can:

- Structure SPVs holding assets

- Tokenize equity shares

- Offer yield distributions on-chain

For infrastructure funds, long-term cash flows make programmable distribution especially useful.

3. Alternative Funds

Hedge funds, venture funds, and private equity funds can tokenize limited partner interests.

This provides:

- Digital cap table management

- Simplified onboarding

- Transparent reporting

For mid-sized asset managers, partnering with a bank offering digital asset tokenization services creates a new distribution channel.

4. Emerging Market and Cross-Border Assets

Tokenization can reduce friction in cross-border investment by standardizing digital issuance.

While regulatory compliance remains jurisdiction-dependent, digital structures improve documentation transparency and tracking.

This strengthens blockchain in boutique investment banking as a tool for global deal execution.

How Can Boutique Investment Banks Use Tokenization to Create New Deal Structures?

Private equity and private credit are natural starting points. Banks can:

- Tokenize equity in special purpose vehicles (SPVs)

- Issue tokenized private debt instruments

- Structure hybrid instruments combining equity and yield

Because digital tokens can be programmed, waterfalls, voting rights, and lock-ups can be embedded at issuance.

This transforms tokenization for deal structuring from a marketing idea into a legal and operational tool.

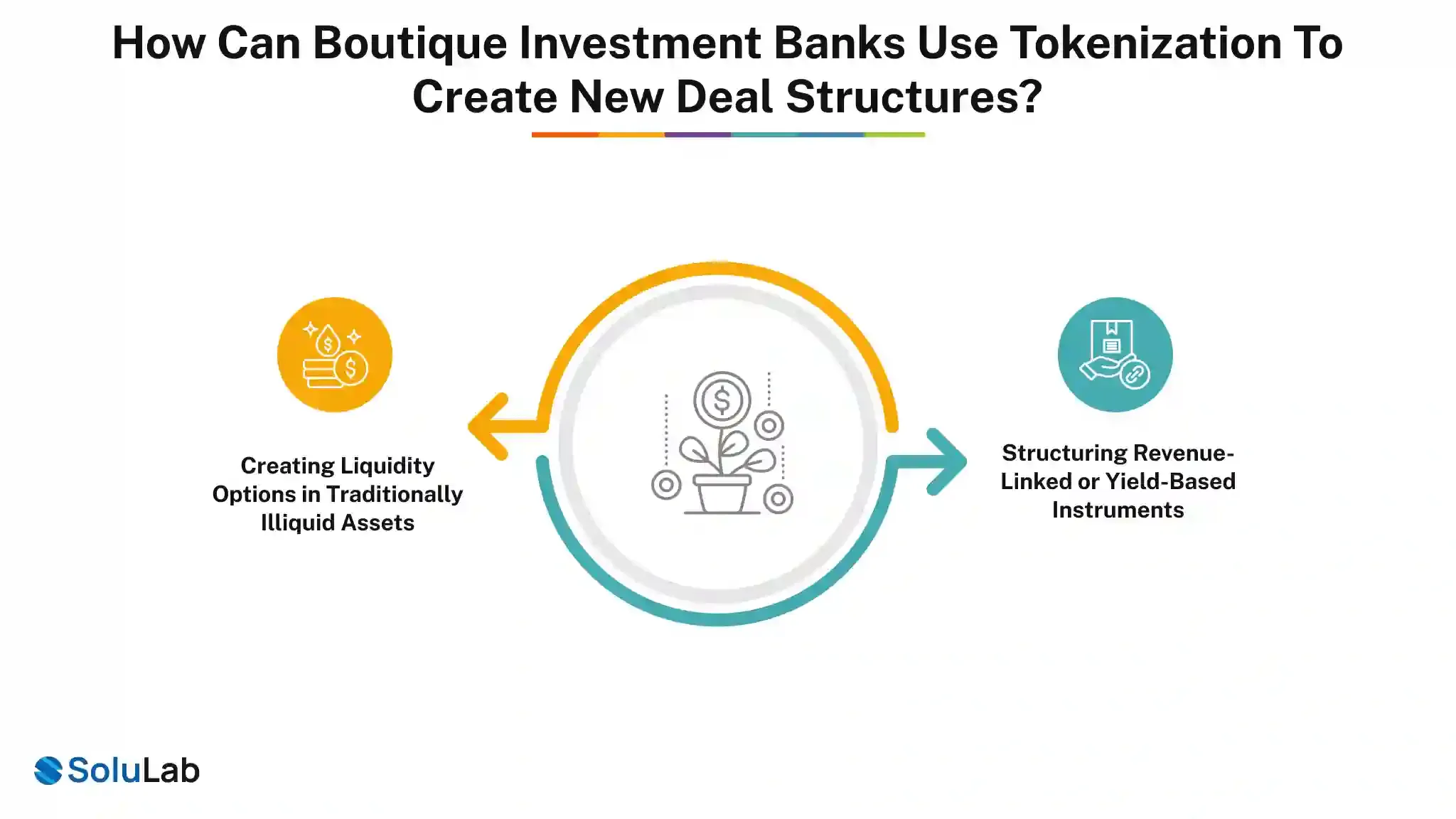

1. Creating Liquidity Options in Traditionally Illiquid Assets

Private market investors often face 5–10 year lock-ups. Tokenized securities can introduce controlled secondary trading through regulated digital platforms that can reduce time by 80%.

While liquidity is not guaranteed, structured secondary markets can:

- Improve price discovery

- Provide partial exit pathways

- Increase investor confidence

This makes asset classes more attractive during capital raising discussions.

2. Structuring Revenue-Linked or Yield-Based Instruments

Boutique firms advising growth-stage companies can tokenize revenue-sharing agreements or structured notes tied to cash flow performance.

This allows:

- Flexible capital raising without equity dilution

- Transparent payout tracking

- Automated distribution logic

In practice, digital asset tokenization enables new hybrid financial products that sit between debt and equity.

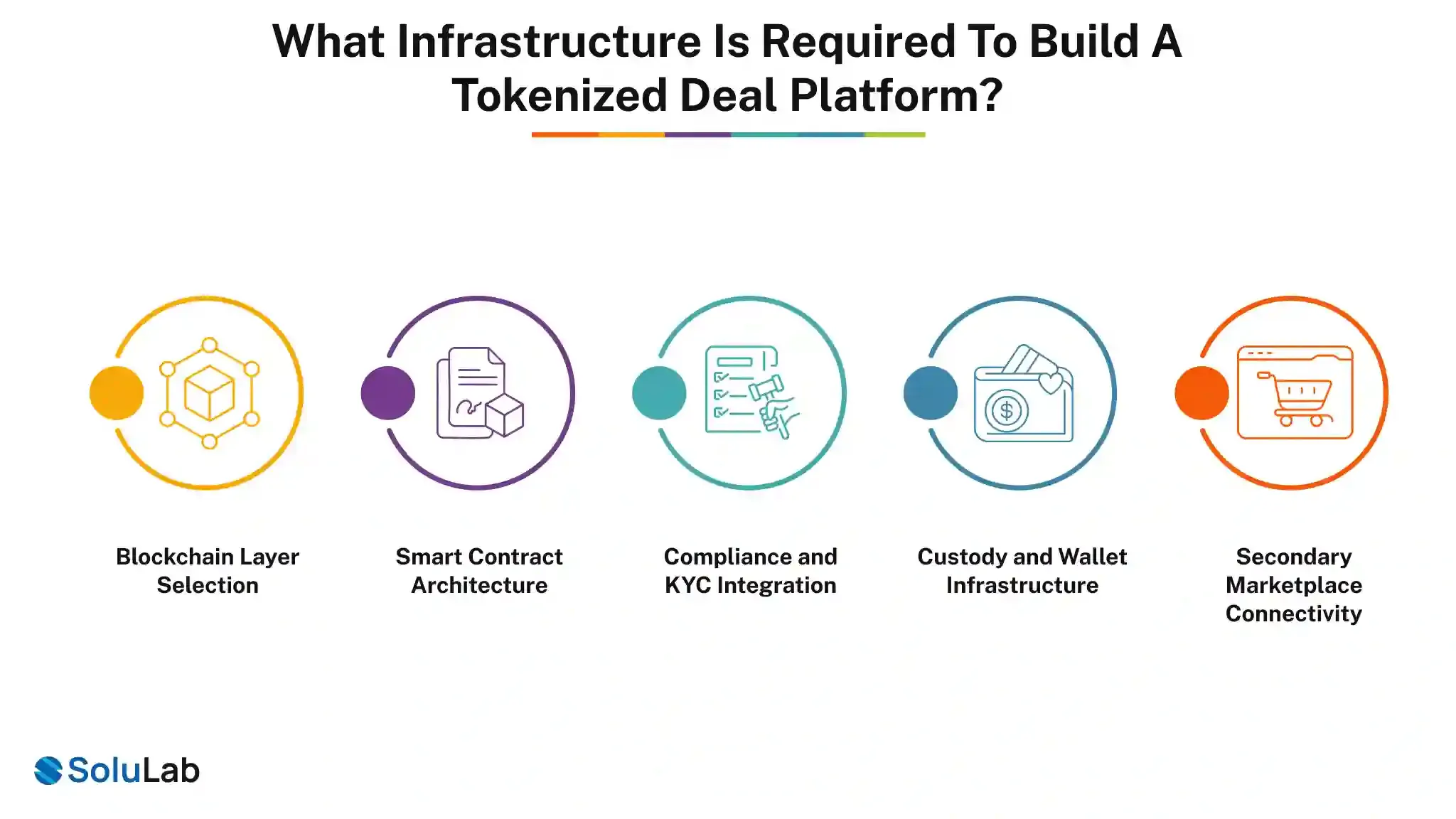

What Infrastructure Is Required to Build a Tokenized Deal Platform?

A serious tokenization initiative requires more than issuing digital tokens. It requires enterprise-grade architecture.

1. Blockchain Layer Selection

Banks must choose between:

- Public blockchains (greater transparency and liquidity potential)

- Permissioned networks (controlled access, institutional focus)

The decision depends on regulatory environment and investor profile.

2. Smart Contract Architecture

Smart contracts define:

- Ownership rights

- Dividend logic

- Transfer restrictions

- Compliance rules

Well-designed contracts reduce manual administration and improve trust.

3. Compliance and KYC Integration

Any tokenization for boutique investment banks strategy must integrate:

- KYC and AML onboarding

- Accredited investor verification

- Transfer compliance checks

Regulatory coding at the contract level ensures that only eligible investors can hold or transfer securities.

4. Custody and Wallet Infrastructure

Institutional investors require secure custody solutions. Infrastructure includes:

- Regulated custodians

- Multi-signature wallet security

- Institutional-grade key management

Without robust custody, tokenized issuance cannot scale.

5. Secondary Marketplace Connectivity

Liquidity requires regulated trading venues or alternative trading systems.

Banks can:

- Partner with digital securities exchanges

- Enable bulletin board-style secondary trading

- Structure-controlled liquidity windows

This expands the value proposition of digital asset tokenization beyond issuance.

Partner with a #1 Asset Tokenization Development Company!

Many boutique banks do not build infrastructure in-house. Instead, they collaborate with an experienced asset tokenization development company like SoluLab that offers:

- asset tokenization development services

- Smart contract design

- Platform integration

- Compliance workflow automation

This reduces time-to-market and lowers technical risk. Contact us today to bring your ideas to life.

FAQs

Deepika is a content writer who blends storytelling with strategic thinking. She explores topics across digital innovation, emerging tech, and the evolving blockchain industry. She enjoys breaking down complex ideas into simple, engaging narratives in the growing global markets.