Tokenisation has been discussed for years. Often framed as a future-facing innovation that lives mostly in pilots, sandboxes, and proofs of concept. What has changed recently is not the technology, but the policy environment around it. For the first time, tokenised money is moving out of controlled experiments and into regulated financial infrastructure.

The USA started the tokenisation and stablecoins shift with the new SEC regulations under the GENIUS Act; the UAE followed closely, and the EU MiCA. And now a new corridor is going to take shape between Hong Kong and Singapore. Together, they are shaping what can best be described as a credible Hong Kong–Singapore token model for cross-border finance.

This matters because banks, payment firms, and large enterprises do not adopt new financial infrastructure on promise alone. They move when risk, regulation, and return are aligned. That alignment is now visible.

Key Takeaways

- The problem: Unclear regulations derail token models, delay launches, and scare institutional capital.

- The status quo: Most projects still “build first, fix compliance later”—leading to rework, penalties, or stalled adoption.

- The solution: Regulation-first token architecture, strong governance, and audit-ready smart contracts.

- How SoluLab helps: SoluLab designs Hong Kong– and Singapore-aligned token models—combining compliance, scalable tokenomics, and enterprise-grade development to unlock long-term ROI, not short-term hype.

From Regulatory Uncertainty to Policy-Grade Money

Until recently, tokenised money sat outside the regulatory perimeter in most jurisdictions. That made it difficult for banks, payment firms, and listed companies to participate.

That changed with two decisive moves:

- In August 2023, the Monetary Authority of Singapore (MAS) published its stablecoin regulatory framework, defining rules for Single-Currency Stablecoins (SCS) pegged to SGD or G10 currencies.

- On August 1, 2025, the Hong Kong Monetary Authority (HKMA) made the issuance of fiat-referenced stablecoins a licensed activity under Hong Kong law, with the first licences expected in early 2026.

These frameworks define:

- 1:1 reserve backing

- Asset quality and custody rules

- Guaranteed redemption timelines

- Ongoing disclosure and supervision

This is what turns crypto development into something banks can actually use. It also enables sustainable token development, where tokens are backed by legal rights, not market sentiment.

Why Banks Care More About Tokenised Deposits Than Stablecoins?

Public narratives around what is stablecoin often frame it as the future of money. Inside banks, the conversation is more nuanced.

1. What tokenised deposits actually are?

Tokenised deposits are traditional bank deposits represented on a distributed ledger infrastructure. They remain on the bank’s balance sheet and retain their legal status as deposits.

This distinction matters.

2. Why banks prefer tokenised deposits?

There are multiple factors why banks favour tokenised deposits:

- Preserve existing deposit regulation

- Keep customer funds inside the banking system

- Support atomic Payment-versus-Payment (PvP) and Delivery-versus-Payment (DvP) settlement

- Reduce reliance on correspondent banking and nostro accounts

In Hong Kong, this approach is being tested through Project Ensemble, launched by HKMA in 2024 and expanded into a sandbox in 2025. The project focuses on:

- Tokenised deposits

- Interbank settlement

- Integration with existing banking workflows

From a transaction banking and treasury perspective, tokenised deposits solve real balance-sheet problems, especially in FX, funds, and collateral settlement.

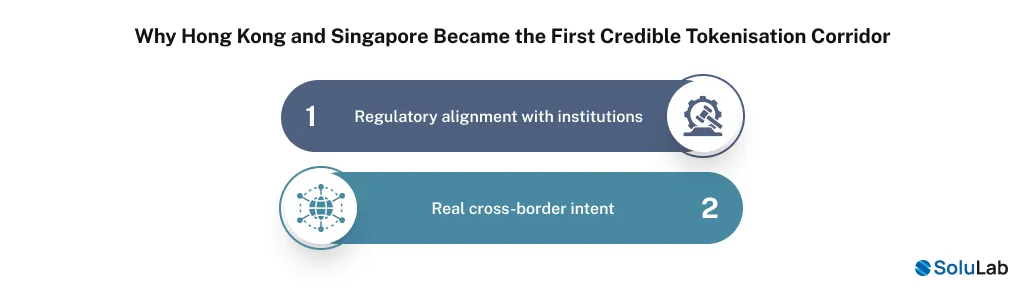

Why Hong Kong and Singapore Became the First Credible Tokenisation Corridor?

Many jurisdictions have tokenisation pilots. Very few have aligned regulation, infrastructure, and bank participation. Hong Kong and Singapore did all three.

1. Regulatory alignment with institutions

Both regulators explicitly designed frameworks that incumbents could adopt. This is why global banks, payment networks, and infrastructure providers are active participants rather than observers.

2. Named programs, not abstract policy

- Project Guardian (Singapore, launched 2022) focuses on cross-border tokenisation of:

- Funds

- FX

- Tokenised bank liabilities

- Interoperability across blockchains

By 2025, it will involve 20+ global financial institutions.

- Project Ensemble (Hong Kong, sandbox phase 2025) targets tokenised deposits and wholesale settlement use cases.

This is not theoretical Blockchain Development in Singapore or Hong Kong. It is production-oriented infrastructure work.

3. Real cross-border intent

Both markets are designing tokenised money specifically for cross-border use, where friction, cost, and settlement risk remain highest. That is why this corridor matters globally.

The Missing Layer: Wholesale CBDC as Neutral Settlement Infrastructure

Even with regulated stablecoins and tokenised deposits, one critical layer is needed: neutral settlement money.

1. What a wholesale CBDC is?

Wholesale Central Bank Digital Currency (wCBDC) is digital central bank money used only by financial institutions for settlement.

Unlike retail CBDCs, it avoids consumer adoption challenges and focuses purely on:

- Interbank settlement

- Cross-border clearing

- Liquidity efficiency

Therefore, wCBDCs ensure smooth transactions.

2. Global proof point: mBridge

The Bank for International Settlements (BIS) led mBridge, a multi-CBDC platform involving:

- Hong Kong

- Mainland China

- Thailand

- UAE

In 2024, mBridge reached Minimum Viable Product (MVP) status, demonstrating:

- Cross-border settlement in seconds

- Reduced FX settlement risk

- Lower liquidity requirements

The BIS then stepped back, allowing participating central banks to operationalise it. This model complements private tokens rather than replacing them.

Read More: How to build an MVP using Blockchain or Generative AI?

3. How other corridors are already reacting?

When two global hubs align on tokenised money and licensing, it doesn’t stay local anymore. Already, global changes started.

Gulf ↔ Asia

Treasury teams in energy, commodities, and infrastructure finance are closely watching how mBridge, the UAE’s Digital Dirham, and Hong Kong tokenised money intersect.

The attraction is simple:

policy-grade instant settlement with FX transparency.

Europe ↔ Asia

European banks navigating MiCA increasingly view Asia as the testbed for:

- Tokenised fund distribution

- Cross-time-zone collateral management

- Atomic settlement outside TARGET2 hours

The collaboration between HKMA and European central banks is not symbolic. It is preparatory.

US ↔ Latin America

Stablecoins already move real volume in LATAM. What is missing is regulatory symmetry.

For US banks and listed fintechs, the Hong Kong–Singapore model shows what a compliant version of stablecoin-based cross-border finance looks like: licensed issuers, clear redemption SLAs, and bank-grade controls.

Read Our Blog Post: RWA Tokenization Platform Development in Hong Kong

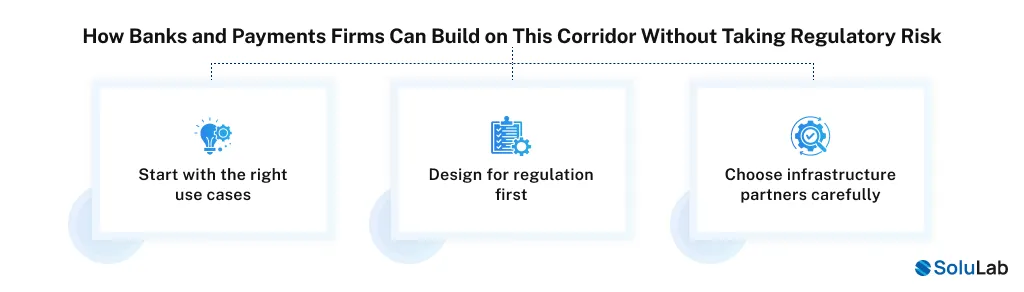

How Banks and Payments Firms Can Build on This Corridor Without Taking Regulatory Risk?

For banks, payment service providers, and enterprises, the question is no longer whether tokenisation matters. It is how to participate without increasing regulatory exposure.

1. Start with the right use cases

Not every flow needs tokenisation. Existing instant payment rails already work well for low-value retail transactions.

Tokenised money delivers the most value in:

- Cross-border B2B payments

- Trade settlement

- Fund subscriptions and redemptions

- FX and treasury operations

- Collateral and liquidity management

Mapping these use cases clearly helps institutions adopt tokenisation where it actually improves outcomes.

2. Design for regulation first

The Hong Kong-regulated stablecoin framework and Singapore’s approach show that compliance is not a blocker. It is a design input.

Successful tokenisation strategies:

- Embed KYC and AML at the token level

- Enforce transfer rules programmatically

- Support auditability and reporting by default

This reduces operational burden rather than increasing it.

3. Choose infrastructure partners carefully

Building in this environment requires experience across blockchain, regulation, and enterprise systems. This is where working with an experienced Blockchain Development Company matters.

Firms offering Tokenization Development Services must understand not just smart contracts, but banking workflows, regulatory expectations, and cross-border settlement mechanics.

This is especially important for institutions operating in or connecting to Singapore and Hong Kong, where expectations are high, and supervision is active.

Conclusion

As mentioned, the Hong Kong–Singapore corridor shows what happens when regulation, technology, and institutional demand align. It offers a reference model for regulated tokenised money that other regions are already studying and, in many cases, preparing to replicate.

For enterprises, banks, and payment firms, the opportunity is not to move fast and break things. It is to build deliberately, using frameworks that are designed to last. Tokenisation is no longer a question of if. It is a question of where and how. To make this vision come true, all you need is the perfect support of a blockchain development company, like SoluLab.

Our 250+ developers with 10+years industrial expertise help you with advanced blockchain development solutions, for example:

- Crypto Wallet Development

- Crypto Exchange Development

- Coin & Token Development

- Launchpad Development

- Prediction Market Platform Development

- AI × Crypto Solutions

To avail more details on the latest blockchain integrations and solutions, contact us today!

FAQs

Shipra Garg is a tech-focused content strategist and copywriter specializing in Web3, blockchain, and artificial intelligence. She has worked with startups and enterprise teams to craft high-conversion content that bridges deep tech with business impact. Her work translates complex innovations into clear, credible, and engaging narratives that drive growth and build trust in emerging tech markets.