Central banks across the world are accelerating digital currency pilots. According to the Bank for International Settlements, over 90% of central banks are researching Central Bank Digital Currencies. However, CBDC development is not one-size-fits-all.

There are two primary models:

- Wholesale CBDC (wCBDC)

- Retail CBDC (rCBDC)

Many enterprises use these terms interchangeably. That is a mistake. Wholesale and retail CBDCs serve completely different economic layers. One modernizes financial market infrastructure while the other transforms consumer payments through an enhanced blockchain development framework.

If you are a bank, fintech, capital market institution, or enterprise technology provider, understanding Wholesale CBDC vs Retail CBDC is not theoretical. It directly impacts infrastructure decisions, compliance design, and long-term strategy.

Key Takeaways

- Wholesale CBDC targets trillion-dollar interbank flows, unlocking 15–25% liquidity efficiency improvements in pilot environments.

- Real-time settlement and atomic DvP reduce reconciliation overhead by nearly 30–40% in controlled financial infrastructure tests.

- Enterprise rollout demands 12–24 months of planning, but can deliver 10–20% long-term operational cost optimization.

What Is the Structural Difference Between Wholesale and Retail CBDC?

The primary structural difference between wholesale and retail CBDCs lies in who can access the system and how the currency circulates within the financial ecosystem.

1. Wholesale CBDC (wCBDC)

Wholesale Central Bank Digital Currency (wCBDC) is designed exclusively for:

- Commercial banks

- Regulated financial institutions

- Clearing houses

- Capital market participants

It operates inside the financial system.

Wholesale CBDC replaces or upgrades existing interbank settlement systems like RTGS. It focuses on improving:

- Interbank payments

- Securities settlement

- Cross-border corridors

- Liquidity management

According to industry pilots reviewed by the International Monetary Fund, wholesale CBDC initiatives have shown settlement time reductions from T+2 to near real-time in controlled environments.

2. Retail CBDC (rCBDC)

Retail CBDC (rCBDC) is issued to:

- Individuals

- Businesses

- Merchants

- Consumers

Retail Central Bank Digital Currency functions like digital cash backed by the central bank. It is designed for:

- Daily digital payments

- Government disbursements

- Financial inclusion

- Peer-to-peer transfers

For enterprises, the structural difference matters:

- Wholesale CBDC upgrades financial infrastructure

- Retail CBDC upgrades consumer payment ecosystems

Access Layer

| Model | Transaction Volume Profile |

| Wholesale CBDC (wCBDC) | High-value, low-frequency |

| Retail CBDC (rCBDC) | Low-value, high-frequency |

Transaction Size Comparison

- Average interbank settlement: $1M–$25M+ per transaction

- Average retail digital payment: $20–$150 per transaction

This is the first big divide in Wholesale CBDC vs Retail CBDC.

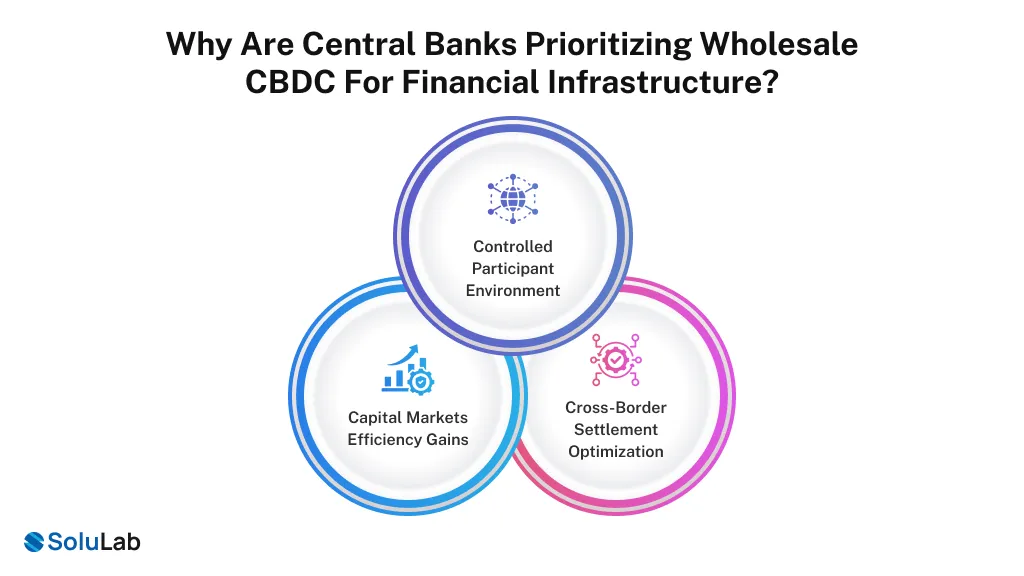

Why Are Central Banks Prioritizing Wholesale CBDC for Financial Infrastructure?

While retail CBDCs receive media attention, many central banks are moving faster on Wholesale CBDC (wCBDC). By using blockchain technology, distributed ledger technology (DLT), and tokenized assets, wholesale CBDCs can make interbank transactions faster, safer, and more transparent.

Why? Because the systemic risk is lower and the impact on infrastructure efficiency is immediate.

1. Controlled Participant Environment

Wholesale CBDCs and retail CBDCs operate under different exposure levels. Wholesale CBDC involves:

- A limited number of licensed banks

- Existing compliance frameworks

- Institutional-grade identity controls

Retail CBDC involves:

- Millions of users

- Wallet security risks

- Large-scale KYC operations

This makes wholesale pilots easier to deploy first.

Read Also: How CBDC Development is Transforming Global Economies ?

2. Capital Markets Efficiency Gains

According to research published through collaborative initiatives coordinated by the Bank for International Settlements, tokenized bond settlement using wholesale CBDC reduced reconciliation overhead by up to 30% in pilot environments.

For banks, this means:

- Lower operational costs

- Reduced settlement risk

- Faster collateral turnover

3. Cross-Border Settlement Optimization

Blockchain-based cross-border payments currently take minutes in many corridors and involve less mediations.

However, Wholesale Central Bank Digital Currency projects are testing:

- 3%–7% per transaction on average

- Atomic settlement

- Real-time FX conversion

- Reduced correspondent banking layers

For a bank moving $10B daily in securities, even 1-day faster capital reuse can materially impact returns.

This is why Wholesale CBDC vs Retail CBDC debates increasingly favor wholesale from an infrastructure-first perspective

How do Risk, Privacy, and Compliance Differ Between the Two Models?

While both wholesale and retail CBDCs aim to modernize financial infrastructure, they introduce different challenges in terms of risk management, data privacy, and regulatory compliance. For financial institutions and governments exploring cryptocurrency development for CBDC infrastructure, understanding these differences is critical:

1. Retail CBDC Risk Landscape

Retail CBDC introduces:

- Mass user data handling

- Consumer privacy debates

- Political scrutiny

- Cybersecurity at national scale

Large-scale retail systems require:

- Advanced fraud detection

- Digital wallet lifecycle management

- Population-scale identity verification

Technology providers such as Microsoft emphasize cloud-scale resilience and zero-trust architecture for retail-grade digital currency environments.

Retail CBDC becomes a public infrastructure project.

2. Wholesale CBDC Risk Landscape

Wholesale CBDC (wCBDC) focuses on:

- Institutional-grade cybersecurity

- Transaction auditability

- Regulated network participation

- High-availability settlement nodes

Because only financial institutions participate, compliance structures already exist.

From a B2B perspective, this means: Retail CBDC demands consumer-grade scale. Wholesale CBDC demands financial-grade precision. Enterprises must design accordingly.

For central banks and financial institutions, investing in robust blockchain development solutions will be essential to address these challenges

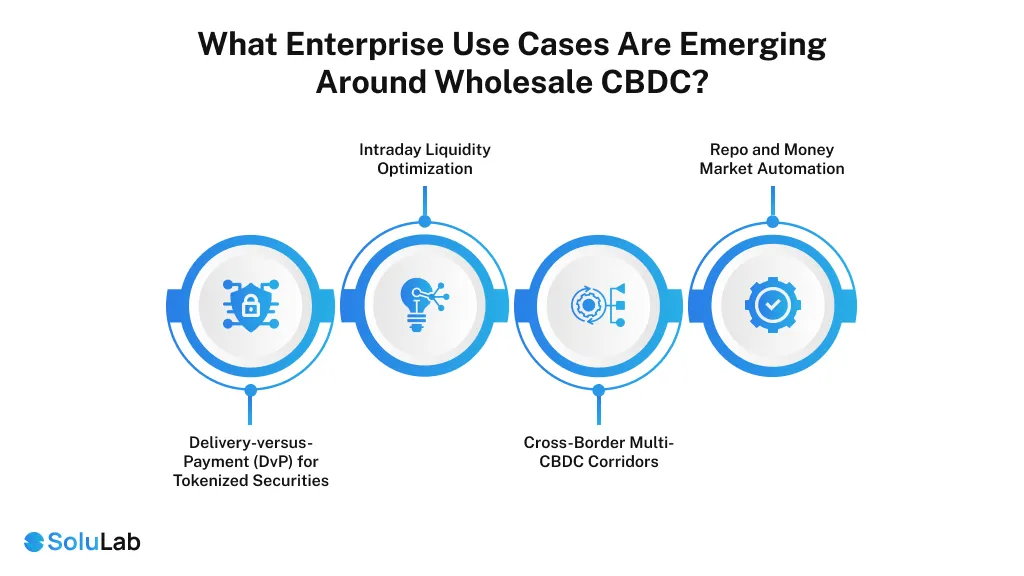

What Enterprise Use Cases Are Emerging Around Wholesale CBDC?

Wholesale CBDC use cases are blockchain technology infrastructure-driven and high-value. Here are the most relevant enterprise opportunities.

1. Delivery-versus-Payment (DvP) for Tokenized Securities

Capital markets still face settlement delays.

With Wholesale Central Bank Digital Currency:

- Securities tokens and cash settle simultaneously

- Counterparty risk reduces significantly

- Post-trade reconciliation layers shrink

Even a 20% reduction in settlement friction can materially improve capital efficiency. For institutions spending $200M annually on post-trade operations, that equals $30M–$40M in potential savings.

2. Intraday Liquidity Optimization

Banks lock up large amounts of capital to meet regulatory requirements. Wholesale CBDC pilots show:

- Real-time liquidity monitoring

- Programmable collateral transfers

- Reduced idle capital

This directly impacts return on capital metrics.

3. Cross-Border Multi-CBDC Corridors

Multi-country wholesale CBDC experiments aim to:

- Reduce FX settlement risk

- Enable atomic cross-border trades

- Shorten payment cycles from days to minutes

For multinational enterprises, this reduces treasury complexity and improves cash visibility.

4. Repo and Money Market Automation

Wholesale CBDC enables programmable repo contracts where:

- Collateral and cash exchange automatically

- Intraday funding becomes more flexible

- Manual reconciliation decreases

This is where Wholesale CBDCs and retail CBDCs clearly diverge in enterprise impact.

Retail CBDC supports merchant adoption. Wholesale CBDC transforms institutional capital markets.

Read more: Agentic AI for Retail Merchandising

What Should Enterprises Consider Before Engaging in CBDC Infrastructure Development?

If your organization is evaluating participation in Wholesale CBDC (wCBDC) or Retail CBDC (rCBDC) ecosystems, consider these five strategic filters.

1. Regulatory Readiness

Digital currency regulation varies by jurisdiction. This includes implementing robust KYC, AML, and identity verification frameworks similar to those used in regulated cryptocurrency development platforms.

Enterprises must:

- Align with central bank frameworks

- Integrate AML and reporting modules

- Prepare for evolving compliance standards

2. Core System Integration

Wholesale Central Bank Digital Currency platforms must integrate with:

- Core banking systems

- Treasury management systems

- ISO 20022 messaging frameworks

Legacy system compatibility often becomes the biggest bottleneck. Many CBDC pilots explore permissioned blockchain development models that allow central banks to control participation

3. Interoperability Strategy

Future financial infrastructure will likely include:

- Asset tokenization platform development

- Stablecoins payment framework

- Wholesale CBDC layers

- Existing RTGS systems

Interoperability determines long-term scalability. CBDC infrastructure must integrate with existing banking systems, payment networks, and fintech app development.

4. Security and Resilience Architecture

Enterprise-grade CBDC infrastructure requires:

- Multi-region redundancy

- Cryptographic key management

- Hardware security modules

- Disaster recovery planning

Financial downtime is not acceptable. Leveraging experience in cryptocurrency wallet development can help strengthen the reliability of CBDC platforms.

5. ROI Justification

Before investing, enterprises should quantify:

- Settlement time reduction

- Capital efficiency improvement

- Operational cost savings

- Liquidity release impact

If numbers do not justify deployment, pilots remain experiments. This is bottom-of-funnel thinking. Strategy must connect to measurable value.

Conclusion

As you have already seen, the distinction between Wholesale CBDC and Retail CBDC is not a branding one. There is a difference between:

- Consumer digital payments

- Institutional financial infrastructure

Retail CBDC modernizes money access. Wholesale Central Bank Digital Currency modernizes the plumbing that moves trillions daily.

If your organization operates in capital markets, treasury management, or interbank settlement, the numbers suggest that wholesale CBDC deserves priority evaluation.

The upside is measurable. The transformation is structural. The timeline is accelerating.

To make changes to your system and adapt to new evolutions, contact SoluLab, a top crypto development company, today.

FAQs

Deepika is a content writer who blends storytelling with strategic thinking. She explores topics across digital innovation, emerging tech, and the evolving blockchain industry. She enjoys breaking down complex ideas into simple, engaging narratives in the growing global markets.