In February 2026, the Central Bank of the UAE finally approved First Abu Dhabi Bank’s dirham-backed stablecoin, the DDSC. And honestly, this isn’t just another crypto gimmick; it’s a big deal for how regulated stablecoins can actually sit alongside traditional finance.

| Look at the numbers: Zerohash says stablecoin transactions jumped 690% in 2025 compared to the year before, and enterprises moved $33 trillion on-chain. That’s huge, almost what Visa and Mastercard move together. |

From our side, having worked with banks and startups across three continents, we’ve seen the same thing over and over. Most banks either get stuck in red tape or rush into crypto experiments that regulators hate, but FAB did something different. They figured out a way for stablecoin development that ticks all the boxes for trust and compliance, while still letting them play in the blockchain space.

For crypto banks or anyone thinking about launching a coin, there’s a lot to unpack here. It shows that you don’t have to choose between being fully compliant and actually innovating. And the way FAB structured the DDSC gives you a blueprint for doing just that.

Key Takeaways

- The Problem

- Most banks want in on stablecoins, but they hit the same walls – regulations are unclear, blockchain tech is tricky to integrate, and they worry about looking risky while experimenting. Everyone sees competitors moving fast, but there’s no simple playbook that balances compliance with innovation.

- The Solution

- FAB’s AED stablecoin shows it can work if you get a few things right: start with regulatory alignment, pick solid blockchain infrastructure (like ADI Chain’s Layer-2), and team up with trusted sovereign partners. It proves you don’t need to throw out your risk frameworks; stablecoins can extend them into programmable finance.

- How SoluLab Can Help

- We’ve built institutional crypto banking solutions for 10+ years, so we help banks do everything from regulatory planning and tech setup to smart contract audits and pilots. With our white-label platform, regional banks have launched compliant digital asset services in months, not years, while keeping the enterprise-grade security they need.

What Is FAB’s AED Stablecoin?

FAB’s DDSC, or Dubai Digital Stablecoin, is the first AED-backed stablecoin approved to run on institutional-grade blockchain infrastructure in the UAE. It came to life through a partnership between First Abu Dhabi Bank (the country’s largest lender), International Holding Company (IHC), and the sovereign fund ADQ, running on ADI Chain – a Layer-2 blockchain built specifically for regulated financial services.

What sets DDSC apart is its design. Every token is backed 1:1 by UAE dirham held in segregated accounts under Central Bank oversight, which tackles the concerns that usually keep traditional banks away from crypto.

As Futoon Hamdan AlMazrouei, Group Head at FAB, put it, this proves that “stablecoins can be integrated responsibly into the financial system when built to meet rigorous regulatory and risk requirements.”

The tech side matters too. By using ADI Chain’s enterprise Layer-2 instead of public chains like Ethereum, FAB ensures banks get payment rails with governance, scalability, and audit standards on par with traditional systems, as banks want programmable stablecoins but still need control and compliance.

According to WEF 2026 Davos analysis, stablecoins have moved from experimental tech to essential infrastructure. The FAB AED stablecoin shows this shift, aiming at institutional use cases like high-value settlement, treasury operations, trade finance, and even future machine-to-machine payments as autonomous economies grow.

Comparing FAB’s Enterprise Stablecoin Platform with UAE Alternatives

The UAE has really become a playground for banks testing stablecoins, with four major projects already approved or live. Seeing how each one works makes it clear which approach fits which type of bank or use case.

1. RAKBANK Stablecoin

RAKBANK got in-principle approval from CBUAE in January 2026 to launch an AED-backed stablecoin mainly for retail payments and tokenization. Unlike FAB, which focused on institutional clients first, RAKBANK is aiming at everyday consumers through its existing digital banking apps.

Their plan is to make it feel seamless for regular users while keeping full 1:1 dirham backing in segregated accounts, verified in real time with smart contracts.

Raheel Ahmed, RAKBANK’s CEO, called this setup public trust and compliance baked in.

2. Zand Bank & AE Coin

Zand Bank rolled out its Zand AED token in November 2025, while AE Coin from AED Stablecoin LLC launched in October, both fully approved under the Payment Token Services Regulation.

Zand focuses on fast settlements and cross-border payments, pairing blockchain with regulated reserves. AE Coin went broader, aiming at public and private sector use, which shows a key lesson – banks should let the use case decide the tech and regulatory setup, not the other way around.

| Bank / Token | Launch / Approval | Focus / Use Case |

| RAKBANK | Jan 2026 (in-principle) | Retail payments, tokenization, consumer apps |

| Zand Bank | Nov 2025 | Fast settlement, cross-border banking |

| AE Coin | Oct 2025 | Public & private sector, broader enterprise use |

What connects all these projects is clear regulatory backing from CBUAE, which is the base any crypto banking software needs to scale.

Al Maryah Community Bank showed that getting in early with regulators gives a serious advantage in the stablecoin space, especially for crypto banks looking to build trust and operate at scale.

Key Lessons for Crypto Banks Launching Stablecoins

1. Regulatory Compliance & Risk Management

The first big takeaway from FAB’s AED stablecoin is simple: start with regulatory approval, not the tech. They spent almost ten months, from April 2025 to February 2026 getting operational approval, which let them build a crypto bank platform that ticked all the Central Bank boxes around reserves, consumer protection, and AML/CFT rules.

This matters because most banks jump into stablecoin tech first, then try to squeeze it into compliance frameworks, and that almost always fails.

TRM Labs’ 2025 white paper stresses that banks need dedicated crypto compliance officers, FATF Travel Rule adherence, and clear policies on supported stablecoins before going live.

Risk management goes beyond compliance. Deutsche Bank’s 2026 digital assets outlook points out that while traders needed stablecoins to rebalance positions 24/7, institutional use requires extra controls. Banks should:

- Build liquidity risk frameworks for redemption scenarios

- Monitor reserve ratios and peg stability in real time

- Prepare for smart contract or blockchain network failures

- Define counterparty limits when connecting to DeFi

FAB handled this by staying close with CBUAE during development, weaving stablecoin liquidity into overall risk governance, and deploying on infrastructure that meets institutional audit standards.

2. Blockchain Integration Considerations

Picking the right blockchain determines if your crypto banking solution can scale. FAB put DDSC on ADI Chain’s Layer-2 instead of the Ethereum mainnet, balancing sovereignty, compliance, and performance.

Public chains have liquidity and composability, but transaction finality, gas fees, and validator uncertainty are tricky for banks. Layer-2s inherit security while letting regulators and banks tweak governance.

The World Economic Forum’s 2026 report even notes that institutional adoption accelerates when blockchain meets traditional finance standards for governance, scalability, and audits.

Key things for teams looking at white-label crypto bank solutions:

- Throughput & latency: Can it handle peak transactions with sub-second finality?

- Compliance: Permissioned access, transaction monitoring, pause functions

- Interoperability: Can the stablecoin move across chains or banking rails?

- Custody & keys: Are wallets institutional-grade with multi-sig?

FAB built DDSC to support automated treasury flows, conditional payments, and smart contract logic that banks’ traditional transfers can’t. This makes it ready for future use cases like AI-driven payments or machine-to-machine commerce.

3. Partner Strategy & Institutional Trust

No regulated stablecoin is launched alone. FAB partnered with sovereign-backed entities (ADQ, IHC) and the CBUAE-approved ADI Foundation, which sends a clear signal: this isn’t a speculative crypto project, it’s real financial infrastructure.

For banks thinking of launching stablecoins, partnerships matter as much as tech. Look at JPMorgan: they rolled out JPM Coin on Coinbase’s Base blockchain after teaming with Mastercard and Coinbase, which gave instant credibility.

HSBC’s tokenized deposits worked because they partnered with custodians and payment networks instead of doing everything themselves.

When choosing partners, consider:

- Regulatory standing: Do they have licenses and regulatory relationships?

- Technical credibility: Have they delivered blockchain systems in production?

- Market reach: Can they reach your target customers?

- Risk alignment: Do they match your security, compliance, and operational standards?

Institutional trust also demands transparency. RAKBANK, for instance, used independent reserve audits and real-time smart contract attestations. These aren’t optional, they’re table stakes for any bank stablecoin.

How Banks Are Launching Stablecoins Globally?

The UAE isn’t the only one exploring institutional stablecoins. Big banks around the world are testing similar ideas, each with slightly different angles, which shows where the market is headed.

JPMorgan’s JPM Coin moved from private blockchain rails to Coinbase’s Base network in 2025, which tells you even the biggest US banks see the value of public blockchain liquidity.

Naveen Mallela, JPMorgan’s global co-head of blockchain, calls deposit tokens a compelling alternative to stablecoins since they stay inside the usual regulatory rules, including reserve requirements. That’s important for banks thinking about crypto services because it proves you can innovate without stepping outside the rules.

HSBC is tokenizing deposits for corporate clients in the US and UAE, planning yield-bearing deposits that settle in seconds but keep full bank guarantees. Most stablecoins don’t pay interest, so this is a big deal for treasury management. It shows that regulated stablecoins, when paired with traditional banking perks, can actually offer better value than plain crypto tokens.

Citigroup, European banks, and others are looking at euro stablecoins and crypto-dollar settlements, and the Wall Street Journal noted that JPMorgan, Bank of America, Citigroup, and Wells Fargo talked about a shared stablecoin back in May 2025 – basically a bank-owned alternative to USDC or USDT. It hasn’t launched yet, but just having that discussion shows banks are taking crypto competition seriously.

And the numbers back it up, Forbes reports mentions of stablecoin in SEC filings jumped 726% from 2023 to 2025, while enterprise inquiries to infrastructure providers grew 400%. These aren’t just pilots anymore; companies are putting real money into AED-backed stablecoins and similar models because the business case is clear – faster settlements, fewer middlemen, and round-the-clock operations that normal banking can’t touch.

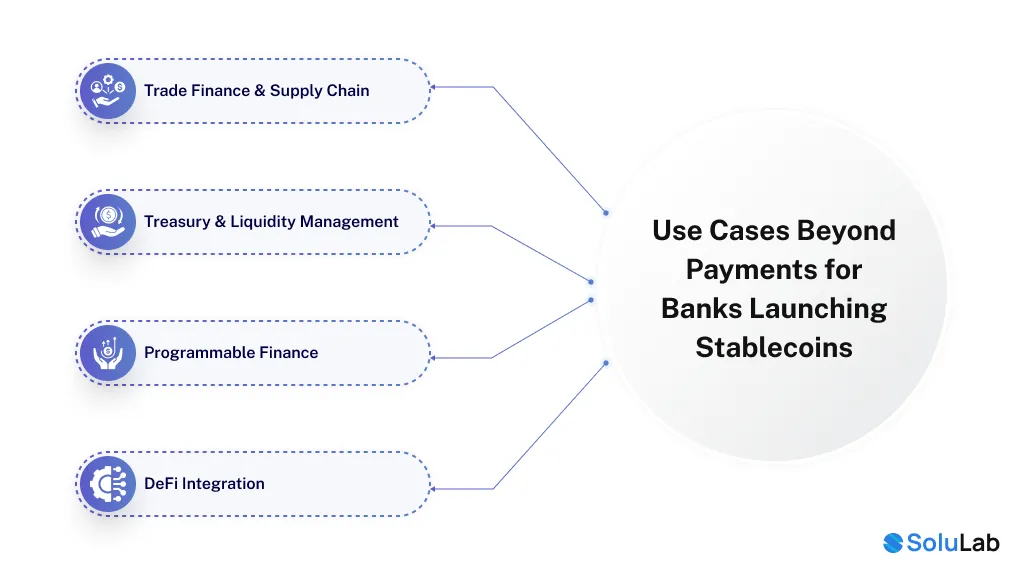

Use Cases Beyond Payments for Banks Launching Stablecoins

People usually talk about stablecoins for cross-border payments, but honestly, that’s just the start. The real shift happens when you can make money programmable in ways old systems just can’t handle.

1. Trade Finance & Supply Chain:

Back in January 2026, WSPN showed that stablecoins can fund actual shipments using blockchain Bills of Lading. An Australian exporter got financing tied directly to the cargo – no corporate guarantees, or long letters of credit. FAB’s DDSC stablecoin proves that smart contracts can handle collateral automatically, which means banks can cut costs without losing security.

2. Treasury & Liquidity Management:

CFOs hate having cash scattered across currencies and banks. Stablecoins let money move anytime, anywhere. Zero Hash saw transaction volume jump 690% in 2025, mostly from companies using stablecoins to shift cash between subsidiaries or pay international suppliers in under a minute, cutting up to 97% of SWIFT fees.

3. Programmable Finance:

Things get really interesting when you mix stablecoins with smart contracts. Payroll that pays people across 50 countries instantly at real-time rates, or insurance claims that automatically pay out when IoT sensors confirm damage, this needs infrastructure that can handle conditions, not just move money.

4. DeFi Integration:

Banks can tap into decentralized lending, earning yield on idle cash or borrowing when short on liquidity, without traditional counterparties. Rules are fuzzy in a lot of places, but some banks are already preparing for when regulators give the green light.

The IMF noted in December 2025 that stablecoins could bypass capital controls, which is why regulators are careful. But that same programmability, when done right lets banks do things old systems can’t. That’s the sweet spot any crypto bank trying to innovate has to find.

How Banks Can Address Regulation, Liquidity, and Peg Stability?

Three big technical things make or break a stablecoin platform: regulations, liquidity, and keeping the peg stable. FAB’s approach actually gives a lot of hints on all three.

1. Regulatory Compliance

Regulations matter, even if your bank is in a country without clear stablecoin laws. Look at the US GENIUS Act or Europe’s MiCA from 2025—they basically laid out reserve rules, transparency standards, and consumer protections.

This made institutions jump on board fast because it removed uncertainty. Even if your jurisdiction isn’t explicit, aligning policies with these frameworks is smart – AML/CFT rules, capital buffers, disclosure stuff, they all apply no matter what kind of asset you’re handling.

2. Liquidity Management

Keeping the peg means either full reserves, like DDSC, or fancy algorithmic fixes (which, let’s be honest, mostly fail). For banks, the safe move is full backing with audited reserves. The tricky part is being ready for huge redemption requests at any moment, especially when the market is panicking.

TRM Labs says banks should stay in close touch with issuers or ecosystem partners to catch early warning signs like reserve hits or regulatory moves. Basically, you need monitoring systems tracking reserve ratios, redemptions, and market pricing all the time.

3. Peg Stability

Even if a coin is fully backed, confidence is everything. USDC fell to $0.87 in March 2023 because some reserves were stuck in Silicon Valley Bank.

Lesson – Spread reserves, be transparent, avoid panic.

FAB uses segregated accounts under Central Bank oversight – banks can learn from that model. It’s about institutional custody that regulators can audit, which keeps the peg reliable.

Banks also face a choice: plug into DeFi for extra liquidity or stay in traditional rails with deposit-style tokens. JPMorgan’s Mallela points out that deposit tokens are safer but less flexible for broader crypto use. There’s no single right answer, depends on who you’re targeting and how much risk you’re willing to take.

Conclusion

FAB’s DDSC launch in February 2026 proves stablecoins in crypto banking aren’t some far-off experiment – they’re real, regulated, and built like proper financial infrastructure. It works because FAB focused on compliance first, picked a blockchain that regulators trust, and partnered with sovereign-backed entities to build confidence.

For banks and crypto firms looking at partnerships or building in-house, the lesson is simple:

- start with compliance, not tech

- choose blockchain infrastructure auditors approve

- Focus on institutional use cases that actually deliver ROI.

The numbers back it up – $33 trillion in stablecoin transactions, 690% enterprise adoption growth, and regulators from the GENIUS Act to MiCA clarifying rules in 2026.

The winners will be those who move fast but smart, using white-label crypto bank solutions to extend their strengths into programmable finance.

FAB showed the path; the question is whether your institution will follow it.

FAQs

With over 3 years of experience, I specialize in breaking down complex Web3 and crypto concepts into clear, actionable content. From deep-dive technical explainers to project documentation, I help brands educate and engage their audience through well-researched, developer-friendly writing.