Every credit system, no matter how modern, rests on a simple assumption: a payment will arrive in the future.

Invoices formalize that assumption. They convert commercial activity into enforceable financial claims. Invoice financing exists to make those claims liquid.

As institutions explore RWA tokenization platform development, the discussion moves beyond what tokenization is in financial services and toward implementation. In invoice financing, tokenization is not about digitizing documents. It is about reinforcing ownership clarity, eligibility enforcement, and capital transparency.

When designed properly, invoice tokenization becomes infrastructure. It strengthens legal certainty, improves data integrity, and enables scalable on-chain credit infrastructure without compromising compliance.

Key Takeaways

- Traditional invoice financing is slow, opaque, and expensive due to intermediaries, manual verification, and limited investor access.

- Businesses face a massive working capital gap in invoice financing, with many SMEs waiting weeks or months for payments and struggling to access liquidity.

- RWA tokenization converts invoices into on-chain assets, enabling automated verification, smart contract–driven payments, and real-time settlement.

- Tokenized invoices unlock faster funding, improved cash flow, and access to global capital with yields often 8–20% APR for investors.

- SoluLab builds compliant RWA tokenization platforms for invoice financing by covering asset onboarding, smart contracts, investor dashboards, and on-chain credit infrastructure to unlock scalable revenue models.

Why Does Invoice Tokenization Become Complex at Scale for Fintech Platforms?

Invoice financing appears simple: a supplier issues an invoice, receives early payment, and the buyer pays later. What complicates this model is operational coordination.

Fintech applications must verify that invoices represent real transactions. They must ensure receivables are not financed multiple times. They must track collections, manage disputes, and report performance to capital providers.

As transaction volume grows, data fragments across ERPs, servicing systems, document repositories, and audit workflows. Reconciliation becomes continuous.

This is where invoice tokenization begins to change the equation.

Tokenization does not eliminate underwriting or servicing. It restructures how critical facts are recorded. When asset state, ownership transfers, and eligibility rules are anchored to a shared ledger, participants operate from a common reference point.

For tokenization fintech platforms, scaling credit becomes less about automation and more about controlled visibility.

That visibility is the foundation of a durable on-chain credit infrastructure.

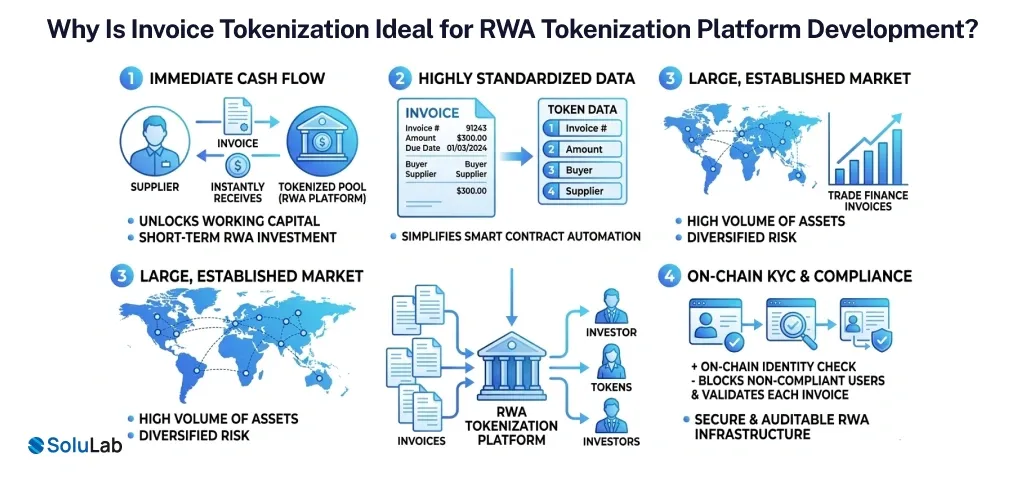

Why Is Invoice Tokenization Ideal for RWA Tokenization Platform Development?

Not every asset translates cleanly into tokenized environments. Invoices do, but only when discipline is preserved.

Invoices are short-duration, continuously generated, and tied to identifiable obligors. These characteristics make them structurally compatible with RWA tokenization platform development.

However, weaknesses surface quickly when governance is weak.

Common breakdown points include:

- Delayed verification

- Incomplete ownership mapping

- Dispute-driven repayment delays

- Limited transparency across capital providers

These risks typically emerge after capital deployment.

Invoice tokenization introduces earlier control points.

When issuance, financing events, and ownership changes are registered in a shared system, inconsistencies surface closer to origination. This reduces post-funding surprises and strengthens institutional trust.

For fintechs building regulated credit products, invoice-backed RWAs serve as practical entry points into broader on-chain asset management strategies.

The value lies not in novelty, but in enforceability.

What Should Go On-Chain in RWA Tokenization Platform Development for Invoice Financing?

One of the most common architectural mistakes in tokenization fintech projects is placing excessive logic on-chain.

Not every workflow benefits from programmability.

Underwriting decisions, dispute resolution, and buyer communications require flexibility. They evolve with regulatory expectations and commercial practices.

Effective tokenization platform development defines a clear infrastructure boundary.

On-chain components should include:

- Unique invoice identifiers

- Asset state tracking

- Ownership records

- Transfer restrictions

- Eligibility enforcement rules

- Embedded on-chain KYC for real-world assets

- Discounting and payout logic

Embedding on-chain KYC for real-world assets directly into token contracts ensures only approved participants can hold or transfer exposure. Compliance shifts from manual review to infrastructure-level enforcement.

Off-chain components should include:

- Credit underwriting judgment

- Servicing workflows

- Buyer dispute handling

- Legal enforcement actions

By separating shared certainty from operational discretion, platforms achieve transparency without rigidity.

This distinction is what separates experimental tokenization from production-grade RWA tokenization platform development.

How Do Tokenization Fintech Platforms Ensure Compliance in RWA Tokenization Platform Development?

In regulated credit markets, technology is rarely the primary constraint. Legal enforceability and compliance design are.

For any tokenization of fintech building invoice-backed products, regulatory alignment must be embedded at the infrastructure layer, not added later.

Invoice receivables already sit within established legal frameworks governing assignment, creditor priority, bankruptcy treatment, and investor eligibility. RWA tokenization platform development must map cleanly onto those frameworks.

Three structural questions must be resolved early:

Who legally owns the receivable?

Tokenized exposure must correspond to enforceable off-chain rights. This often requires assignment agreements, SPV structures, or trust arrangements that legally recognize investor claims.

Tokens cannot represent economic exposure unless legal ownership pathways are clearly documented.

Who is permitted to hold tokenized exposure?

Invoice-backed credit products are typically restricted to accredited or institutional investors. This is where on-chain KYC for real-world assets becomes critical.

Instead of managing compliance through separate onboarding systems, mature platforms embed eligibility checks directly into token contracts. Transfer restrictions, jurisdictional rules, and accreditation requirements are enforced programmatically.

Compliance becomes infrastructure.

How is oversight maintained?

Regulators expect auditability. They expect traceable origination data, exposure reporting, and event transparency.

Well-designed on-chain credit infrastructure supports immutable event logs, permissioned supervisory access, and consistent reporting outputs aligned with existing financial disclosure standards.

Across jurisdictions, the direction is clear: tokenized financial products must meet the same standards as traditional ones.

Tokenization fintech teams that treat regulation as a design input rather than a barrier scale more efficiently across markets.

What Architecture Is Required for On-Chain Credit Infrastructure in Invoice Tokenization?

Once legal alignment is established, the conversation shifts to architecture.

RWA tokenization platform development is not about selecting a blockchain. It is about designing a coordinated infrastructure stack.

A compliant invoice tokenization system typically includes the following layers:

Identity & Access Layer (On-Chain KYC Enforcement)

Participants such as suppliers, investors, and servicers are verified and permissioned before interacting with assets.

This layer embeds:

- KYC/AML validation

- Accreditation checks

- Jurisdictional eligibility controls

- Role-based permissions

When integrated into token contracts, this becomes enforceable on-chain KYC for real-world assets, preventing unauthorized transfers at the infrastructure level.

Asset Registry Layer

The registry links each tokenized position to underlying invoice data:

- Invoice identifiers

- Obligor details

- Face value

- Due dates

- Hash references to supporting documentation

This creates a unique on-chain reference that reduces duplication and improves audit clarity.

Token Contract Layer

Token contracts encode:

- Economic exposure

- Transfer restrictions

- Discounting logic

- Repayment and default handling

- Fee distribution

Governance controls and documented upgrade paths are essential for institutional adoption.

Cash Flow & Settlement Layer

This layer manages:

- Discount calculations

- Accrual tracking

- Payout execution

- Fiat or tokenized settlement integration

It ensures capital providers receive predictable performance tracking aligned with credit terms.

Monitoring & Reporting Layer

Immutable, timestamped logs simplify:

- Audit processes

- Risk monitoring

- Regulatory reporting

- Investor transparency

Individually, these components are familiar. Together, they create a structured on-chain credit infrastructure capable of supporting institutional-scale invoice financing.

Architecture is not complex for its own sake. It is risk containment by design.

How Do You Ensure Data Integrity in Invoice Tokenization Platforms?

In invoice financing, confidence rarely breaks because of pricing. It breaks because of data integrity failures.

Every invoice tokenization platform depends on a foundational question:

Is this receivable authentic, unique, and enforceable?

Traditional systems rely on ERP integrations, document verification, buyer confirmations, and periodic audits. These mechanisms work, but they are fragmented.

Tokenization shifts where validation becomes visible.

In production-grade RWA tokenization platform development, key invoice attributes are anchored at the point of approval:

- Unique identifiers

- Invoice amounts

- Issuance dates

- Obligor information

Supporting documents remain off-chain for privacy and flexibility, but their integrity can be validated through cryptographic hashes.

This structure enables:

- Early duplication detection

- Double-pledge prevention

- Clear ownership tracking

- Event-level traceability

Instead of relying primarily on retrospective audits, verification becomes embedded within the operating workflow.

For institutional investors, this transparency strengthens trust. For fintech operators, it reduces reconciliation overhead.

For regulated markets, it is the foundation of sustainable on-chain credit infrastructure.

What Risks Must Be Managed in On-Chain Credit Infrastructure for Invoice Tokenization?

Tokenized invoice platforms are credit systems first. Blockchain does not remove risk. It restructures how risk is observed and controlled.

In invoice tokenization, three categories of risk require deliberate design.

1. Credit Risk

Buyer defaults, delayed payments, and dispute-driven cash flow interruptions remain fundamental risks.

Short-duration invoices limit exposure windows, but underwriting discipline is still required. Concentration limits, obligor diversification, and exposure caps must operate independently of the blockchain layer.

On-chain systems improve visibility. They do not replace credit judgment.

2. Operational Risk

Operational breakdowns, delayed servicing updates, reconciliation gaps, reporting errors can erode investor confidence even when assets perform.

Well-designed on-chain credit infrastructure reduces these risks by anchoring financing events, ownership transfers, and repayment milestones to immutable records.

But servicing discipline must remain strong. Infrastructure enhances process; it does not compensate for weak execution.

3. Smart Contract & Governance Risk

Smart contracts introduce new systemic considerations:

- Contract logic errors

- Poorly controlled upgrade mechanisms

- Ambiguous administrative permissions

- Inadequate incident response planning

Institutional participants expect documented governance models, third-party security reviews, and transparent upgrade paths.

For tokenization fintech teams, risk exposure is not purely financial. It is architectural.

Platforms that expose risk indicators early through structured reporting, consistent data flows, and clearly defined controls maintain institutional trust even under stress.

Visibility is the unifying theme across all risk categories.

How Are Invoices Structured into Onchain Asset Management Products?

Once infrastructure and risk controls are in place, product design determines scalability.

Invoice-backed RWAs can be structured in multiple ways depending on capital provider preferences and regulatory treatment.

1. Pool-Based Structures

Multiple invoices are aggregated into diversified pools. This approach:

- Reduces obligor concentration

- Simplifies investor allocation

- Supports tranche-based risk segmentation

For institutional capital, this aligns closely with traditional private credit models.

Tokenization here enhances transparency and transferability within the pool structure.

2. Invoice-Level Exposure

Each invoice is tokenized individually, allowing granular selection. This model increases transparency but introduces operational complexity as transaction volumes scale.

It may suit specialized funds or sophisticated investors seeking selective exposure.

3. Structured Credit Instruments

Some platforms issue structured notes or private credit instruments backed by receivables.

This approach mirrors conventional credit markets and may simplify regulatory classification, especially for banks and asset managers already operating within defined mandates.

Across all models, the objective is consistent:

Transform invoice receivables into investable, transparent on-chain asset management products without disrupting underlying legal frameworks. Tokenization does not dictate structure. It enhances enforceability and reporting within chosen structures.

Alignment between product design and operating capacity is what determines durability.

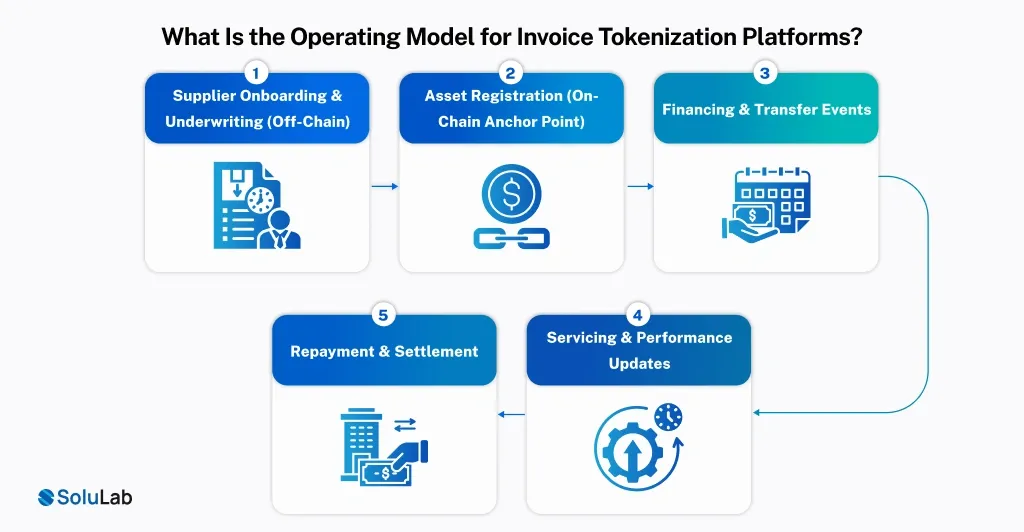

What Is the Operating Model for Invoice Tokenization Platforms?

Architecture and product design only succeed if the operating model holds under daily pressure. In invoice financing, that pressure emerges quickly onboarding volume, exceptions, buyer disputes, and collection delays.

A production-grade RWA tokenization platform development lifecycle typically unfolds as follows:

1. Supplier Onboarding & Underwriting (Off-Chain)

Suppliers are onboarded through traditional compliance and credit review processes. Invoices originate within ERP or invoicing systems.

Underwriting decisions remain discretionary.

2. Asset Registration (On-Chain Anchor Point)

Once approved for financing, critical invoice attributes are recorded within the asset registry.

This creates a permanent reference for:

- Ownership

- Financing events

- Exposure limits

- Eligibility enforcement

At this moment, operational workflows intersect with on-chain credit infrastructure.

3. Financing & Transfer Events

Tokens representing economic exposure are issued or allocated under defined eligibility rules. Transfer restrictions enforce on-chain KYC requirements automatically.

4. Servicing & Performance Updates

Collections, disputes, and buyer communications remain operational functions.

However, servicing outcomes feed structured updates back into the system, reducing lag between real-world performance and investor visibility.

5. Repayment & Settlement

Upon payment, the system executes payout logic and updates asset state.

Immutable records simplify audits and reporting.

Over time, this integrated feedback loop becomes one of the strongest advantages of invoice tokenization platforms.

For institutions evaluating tokenization fintech initiatives, operating consistency often matters more than transaction speed.

Predictability builds trust. Infrastructure sustains scale.

Should Fintechs Choose White-Label Tokenization or Build In-House?

Once the architecture and operating model are clear, execution becomes the defining decision. Should institutions pursue internal RWA tokenization platform development, or adopt a fintech white-label tokenization model?

The answer depends on regulatory exposure, internal capability, and long-term strategic control.

Building In-House

Internal development offers:

- Full architectural control

- Custom compliance integration

- Direct ownership of smart contract governance

- Deeper alignment with internal IT and risk systems

However, it also requires assembling expertise across:

- Smart contract engineering

- Blockchain security audits

- On-chain KYC implementation

- Regulatory structuring

- System integration

For many banks and fintechs, this extends timelines and increases execution risk.

White-Label Tokenization Platforms

White-label approaches accelerate go-to-market by providing pre-built infrastructure layers.

This can reduce:

- Early engineering overhead

- Security uncertainty

- Initial compliance structuring complexity

However, institutions must carefully evaluate:

- Customization limits

- Governance control

- Regulatory flexibility

- Long-term scalability

White-label tokenization infrastructure works best when it serves as modular infrastructure, not a closed system.

From its experience supporting regulated institutions, SoluLab has observed that successful programs treat implementation as phased infrastructure deployment.

Early stages focus on:

- Compliance alignment

- Asset registry design

- On-chain credit infrastructure integrity

Expansion follows only after legal and operational stability is validated.

Regardless of approach, clarity of scope and regulatory assumptions prevents costly rework later.

Is Invoice Tokenization a Sustainable Fintech Strategy?

For executive decision-makers, the core question is durability.

Does invoice tokenization create incremental operational value, or merely technical complexity?

In practice, sustainable platforms tend to generate value in measurable ways:

- Reduced reconciliation overhead

- Faster audit cycles

- Clearer ownership traceability

- Improved capital transparency

- More predictable funding cycles

The efficiency gains are rarely dramatic overnight. They accumulate as data integrity improves and operational friction declines.

There is also a strategic layer.

Institutions investing in white label RWA tokenization platforms for invoice financing build infrastructure that can extend into other short-duration credit assets.

What begins with receivables can evolve into broader on-chain asset management capabilities without rebuilding core systems.

Tokenization, in this context, is not a single-product bet. It is infrastructure readiness for an evolving financial market structure.

For banks and fintechs evaluating long-term positioning, that readiness matters.

What Comes After the First Tokenized Invoices?

Invoice financing has always depended on trust; in data, ownership clarity, and risk management discipline.

Tokenization does not change those fundamentals. It enforces them more consistently.

When designed as infrastructure rather than experimentation, invoice-backed RWAs can strengthen compliance, improve transparency, and support scalable on-chain credit infrastructure.

Through its work with banks and fintech platforms, SoluLab supports teams translating credit structures into compliant, production-ready tokenization systems aligned with regulatory expectations and operational realities.

For institutions evaluating invoice-backed RWA products, structured readiness planning clarifies architecture choices, governance design, and realistic implementation timelines before significant capital is committed.

FAQs

Shipra Garg is a tech-focused content strategist and copywriter specializing in Web3, blockchain, and artificial intelligence. She has worked with startups and enterprise teams to craft high-conversion content that bridges deep tech with business impact. Her work translates complex innovations into clear, credible, and engaging narratives that drive growth and build trust in emerging tech markets.

![Top 10 Asset Tokenization Companies in the USA [2026 Edition]](https://www.solulab.com/wp-content/uploads/2025/10/Asset-Tokenization-Companies-in-USA.webp)