Every country is rebuilding, adopting the latest technology to stand its ground in the global tech markets. Saudi Arabia is also just modernizing its finance. It is redesigning how money moves across borders.

KSA Cross Border Payments are rising sharply as trade expands across the GCC, Asia, Europe, and Africa. Saudi Arabia is the largest economy in the Middle East, with a GDP above $1 trillion and growing cross-border trade flows in oil, construction, infrastructure, logistics, and technology.

At the same time, the Kingdom remains one of the world’s top remittance-sending countries, with outbound remittances often exceeding $35–40 billion annually.

Traditional cross-border payment processing solutions are slow, expensive, and layered with intermediaries. That model does not match Saudi Arabia’s Vision 2030 ambition for real-time digital infrastructure.

Now, blockchain in Saudi Arabia is moving from experimentation to enterprise-grade use cases. Banks, regulators, and fintechs are actively evaluating blockchain technology in banking to improve 80% speed, 100% transparency, and 70% liquidity management.

Key Takeaways

- Modernizing KSA Cross Border Payments requires more than speed. Regulatory alignment, liquidity design, and secure integration with the Saudi banking system define long-term success.

- Permissioned blockchain technology in banking can significantly reduce 40% settlement delays, improve transparency, and lower operational risk across cross-border payments in the Middle East.

- For enterprises building compliant, scalable cross-border payment processing solutions that strengthen treasury control and support Vision 2030 growth ambitions is the main goal.

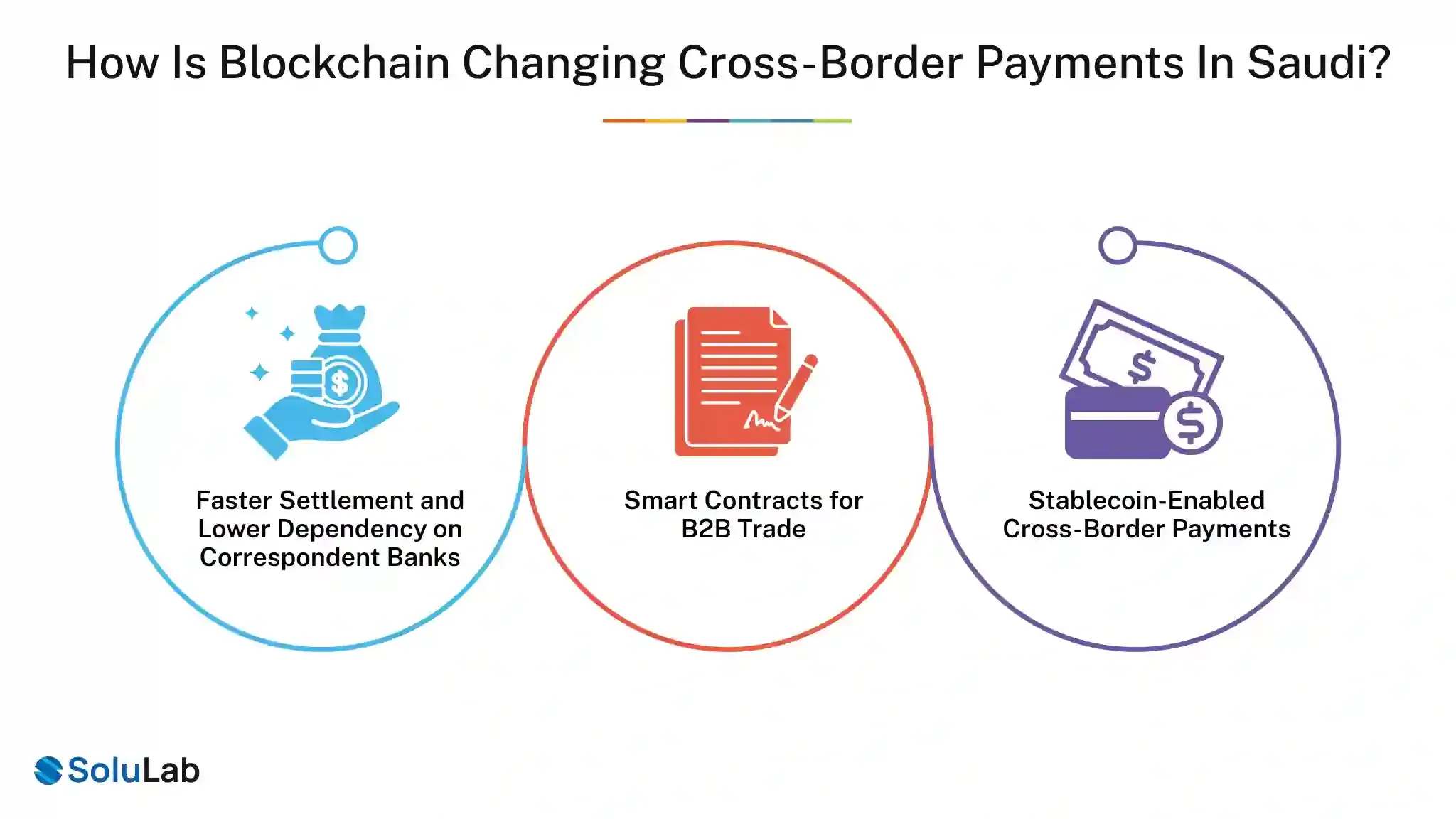

How Is Blockchain Changing Cross-Border Payments in Saudi?

Blockchain removes friction from settlement layers. Also, helps enterprises build a layered payment structure and gives control to users on privacy.

1. Faster Settlement and Lower Dependency on Correspondent Banks

Today, cross-border payments in the Middle East often rely on correspondent banking chains. Each intermediary adds fees, FX spreads, and time delays.

With blockchain-based cross-border payment solutions:

- Settlement can move from 2–5 days to near real-time

- Fewer intermediaries reduce fee layers

- Shared ledger visibility reduces reconciliation work

The Saudi Central Bank has already experimented with cross-border digital currency pilots, including Project Aber with the UAE. The objective was to test distributed ledger settlement between central banks.

That pilot showed one clear insight: blockchain reduces settlement risk while increasing audit transparency.

2. Smart Contracts for B2B Trade

For enterprises, cross-border payment solutions powered by blockchain allow:

- Automated invoice settlement

- Trigger-based release of funds

- Embedded compliance checks

- Real-time transaction tracking

In oil, logistics, and infrastructure contracts, this reduces working capital lock-up and improves treasury planning.

3. Stablecoin-Enabled Cross-Border Payments

Stablecoin-Enabled Cross-Border Payments are being explored globally because they:

- Operate 24/7

- Settle faster than SWIFT

- Reduce volatility compared to crypto assets

While Saudi regulators remain cautious, institutional-grade stablecoin for remittance use cases is gaining attention worldwide. For high-volume corridors, this model reduces FX conversion layers and settlement delays.

How Do Cross-Border Payments Work in Saudi Arabia Today?

To understand the SA blockchain opportunity, we must understand the pain points.

1. The Traditional Flow

Under the current Saudi banking system:

- A Saudi company initiates a payment through its bank

- The bank uses SWIFT messaging

- Funds pass through correspondent banks

- Currency conversion occurs along the chain

- The beneficiary bank credits the recipient

Each layer adds:

- Processing fees

- FX margins

- Compliance checks

- Settlement delays

For enterprise treasury teams, this creates three core problems:

- Poor cash flow predictability

- High transaction costs

- Manual reconciliation of overhead

Saudi Arabia’s trade volume continues to grow, especially with China, India, the UAE, and the US. This increases pressure on existing cross-border payment processing solutions.

2. Remittance Volume Pressure

Saudi Arabia consistently ranks among the world’s largest remittance senders. Millions of expatriate workers send funds to India, Pakistan, Bangladesh, Egypt, and the Philippines.

Even a 1% reduction in transfer fees could translate into hundreds of millions in savings annually across corridors.

That is why cross-border payments in the Middle East are under transformation pressure.

What Role Does Vision 2030 Play in Blockchain Payment Adoption?

Vision 2030 is not just about diversification. It is about digitization. The Saudi Vision 2030 includes strong financial sector development goals:

- Increase non-cash transactions

- Promote fintech innovation

- Attract global investors

- Improve financial infrastructure efficiency

Blockchain technology in banking aligns directly with these priorities.

1. Financial Sector Development Program (FSDP)

Under Vision 2030, the Financial Sector Development Program aims to:

- Increase digital payment penetration

- Strengthen capital markets

- Enhance financial inclusion

Saudi Arabia has already seen rapid growth in digital payment adoption domestically. Extending this digital maturity to KSA Cross Border Payments is the logical next step.

2. Regional Leadership

Saudi Arabia aims to lead cross-border payments in the Middle East. By modernizing infrastructure, the Kingdom strengthens:

- Trade settlement reliability

- Investment inflow efficiency

- Regional payment corridor dominance

Blockchain in Saudi Arabia supports this strategic positioning.

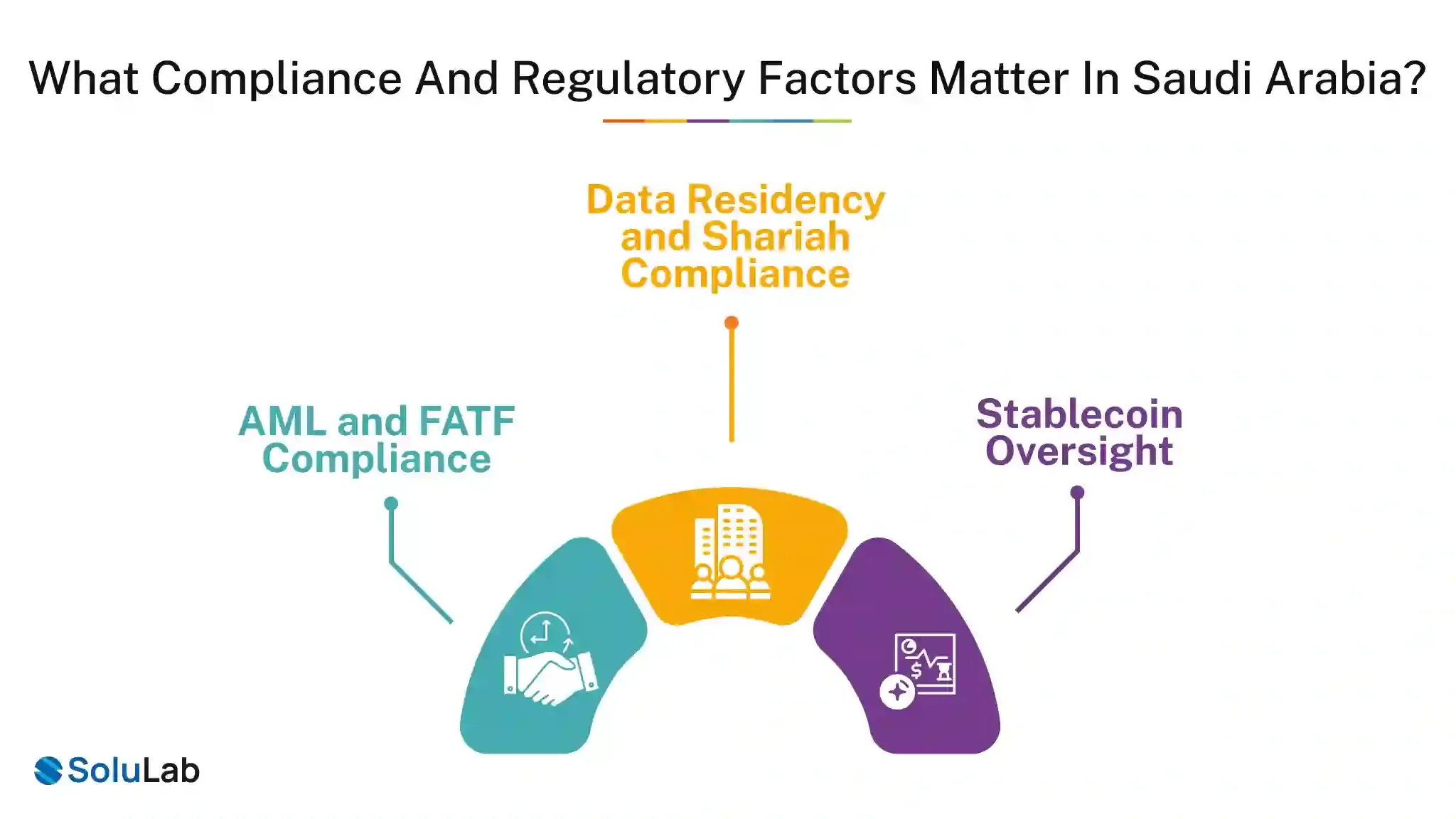

What Compliance and Regulatory Factors Matter in Saudi Arabia?

Blockchain adoption must align with regulation. Saudi Arabia maintains strong oversight under the Saudi Central Bank.

1. AML and FATF Compliance

Any cross-border payment solution must include:

- Know Your Customer (KYC)

- Anti-Money Laundering (AML) screening

- Counter-terror financing controls

- Real-time risk monitoring

Permissioned blockchain networks allow regulators to maintain visibility while improving settlement efficiency.

2. Data Residency and Shariah Compliance

Enterprise adoption in Saudi Arabia also requires:

- Data localization where applicable

- Shariah-aligned financial structuring

- Clear audit trails

Blockchain’s immutable ledger helps with regulatory reporting, but governance frameworks must be carefully designed.

3. Stablecoin Oversight

Stablecoin-Enabled Cross-Border Payments would require:

- Clear asset backing

- Licensed financial intermediaries

- Central bank approval

Saudi Arabia is more likely to adopt regulated, institution-backed digital settlement models rather than open, permissionless systems.

How Does Blockchain Improve Remittance Flows to and from Saudi Arabia?

Remittances are one of the strongest use cases.

1. Lower Fees for Workers

Saudi Arabia sends tens of billions of dollars abroad annually. Traditional remittance fees can range from 3% to 6%, depending on the corridor.

Blockchain-based stablecoin for remittance solutions can:

- Reduce intermediary layers

- Minimize FX spreads

- Enable same-day settlement

For workers sending money monthly, this makes a real difference.

2. Transparency and Tracking

Blockchain networks allow:

- End-to-end transaction tracking

- Confirmation visibility

- Reduced settlement uncertainty

This builds trust, especially in high-volume remittance corridors like Saudi–India and Saudi–Pakistan.

3. Banking Inclusion

Blockchain-based cross-border payment processing solutions can integrate fintech wallets and banking APIs, expanding reach beyond traditional banking networks.

What Infrastructure Is Required to Implement Blockchain Cross-Border Payments?

Enterprise-grade blockchain technology development requires more than just a network alignment.

1. Permissioned Blockchain Architecture

For regulatory alignment, Saudi institutions would likely deploy:

- Permissioned distributed ledger networks

- Controlled node access

- Central bank oversight integration

2. Core Banking Integration

Integration with existing Saudi banking system infrastructure is essential:

- API connectivity

- Real-time ledger synchronization

- Treasury management alignment

3. FX and Liquidity Management Layer

Cross-border payments require:

- Multi-currency settlement capabilities

- Liquidity pool management

- Automated FX execution

4. Compliance Automation

A strong cross-border payment solution must include:

- Embedded AML engines

- Transaction monitoring

- Regulatory reporting modules

5. Cybersecurity and Resilience

Enterprise networks must include:

- Node-level encryption

- Identity management

- Disaster recovery systems

This is where working with an experienced Blockchain development company becomes critical. Architecture design, regulatory alignment, and system integration determine long-term scalability.

Conclusion

With the right blockchain architecture and regulatory-first approach, your cross-border payment strategy in Saudi Arabia can shift from slow and expensive to fast and efficient. Now is the time to rethink how KSA cross-border payments should work.

Partnering with an experienced Blockchain consulting company like SoluLab helps you move with clarity and compliance. Our capabilities include:

- Regulatory-compliant network design

- Core banking and API integration

- Stablecoin-enabled cross-border payment models

- AML, KYC, and transaction monitoring systems

- Enterprise-grade wallet and treasury solutions

With 250+ in-house experts, we build secure, scalable cross-border payment solutions aligned with Saudi regulations and Vision 2030 goals.

Let’s build your next-generation payment infrastructure today!

FAQs

Deepika is a content writer who blends storytelling with strategic thinking. She explores topics across digital innovation, emerging tech, and the evolving blockchain industry. She enjoys breaking down complex ideas into simple, engaging narratives in the growing global markets.