Germany’s financial world is quietly waking up. It’s not just a strict regulator sitting on the sidelines anymore. Banks are actually mixing crypto with their usual services, and white label crypto wallet solutions are suddenly hot. The numbers tell part of the story – By 2025, around 27.32 million Germans, approximately 32.84% of the population, will engage with digital currencies, but it’s the buzz behind the scenes that’s interesting.

Big banks are stepping in, and rules are making sense. Sparkassen-Finanzgruppe wants crypto trading for 50 million customers, and Deutsche Bank is fiddling with Ethereum layer-2. So, cryptocurrency wallet solutions are no longer a side project. They’re becoming the backbone for serious finance.

But everyone wants speed and compliance. Companies don’t want to reinvent the wheel, which is why white label crypto wallet providers are getting a shot. You take a ready-made platform, plug it in, and boom, you’re live in a market that’s growing and regulated. Fast, simple, and no guesswork.

Key Takeaways

Key Takeaways

- The status quo: Without clear frameworks, businesses face compliance risk and poor user trust—hindering scalable wallet deployment.

- ROI impact: German-compliant wallets gain higher user trust, broader EU reach, and stronger revenue potential through fiat on-ramps and licensed operations.

- How SoluLab helps: SoluLab builds Germany-ready white-label crypto wallets with regulatory alignment, robust security, and monetization features that drive adoption and long-term ROI.

Why Are Enterprises Launching White-Label Wallets in Germany?

Here’s the situation. Traditional banks in Germany are in a tough spot: their customers want crypto, but building it in-house is expensive, slow, and they often don’t have the expertise. That’s why white-label solutions are getting so much attention.

The surge isn’t random. There are a few clear reasons, and if you’re thinking about launching a white-label wallet in Germany, you need to know them.

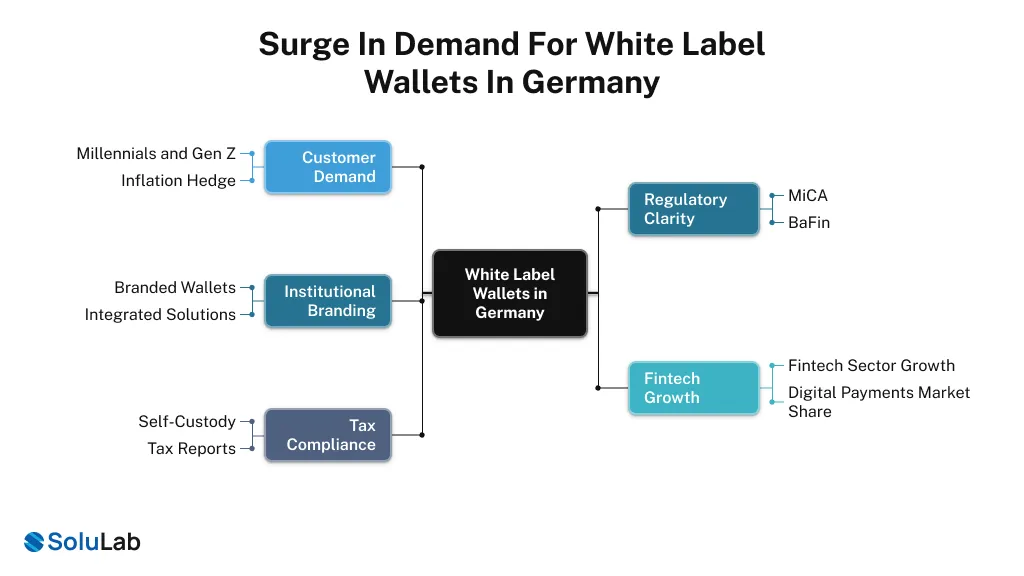

1. Banks Can’t Ignore Customers

Younger Germans, especially millennials and Gen Z, see crypto as a hedge against inflation and a fresh investment option. Retail adoption is climbing, and user-friendly wallets and apps are everywhere. When customers start asking, you can’t just sit still.

2. Regulations Are Clearer Now

Before MiCA, crypto was in a legal gray area. But with MiCA fully in effect since December 2024, banks now know exactly what to do. BaFin has spelled out licensing, custody, and operational rules. This kind of clarity not only cuts risk but also makes launching a German cryptocurrency wallet much faster and smoother.

3. Institutions Want Their Own Brand

Big banks and other players aren’t happy with generic wallets. They want something branded, fully integrated, and compliant. White-label crypto wallet development makes that possible without the long timelines or huge teams.

4. Fintech Growth and Open Banking

Germany’s fintech sector is booming at 14.71% annually, with digital payments taking 37.65% market share. PSD2 and open banking taught everyone to think API-first and embrace white-label integrations. That mindset naturally extends to crypto wallets too.

5. Tax Compliance Matters

Germans care about self-custody and taxes, and they want wallets that export clean transaction histories, label transfers correctly, and generate reports for tax authorities automatically. Generic wallets don’t cut it; that’s why the best crypto wallets in Germany have these features built in, so users and regulators are both happy.

How Do MiCA and BaFin Shape White Label Wallets in Germany for Enterprise Launches?

This is where Germany’s story starts to look very different from most of Europe. While other regulators were still debating what crypto should be, Germany moved ahead and made hard decisions. Not fast or flashy decisions, but deliberate ones that actually stuck.

From Conservative Skeptic to Pragmatic Innovator

Germany’s regulators have always been cautious, and BaFin in particular spent years treating crypto like something that could easily go wrong. Around 2020, though, the tone changed. Bitcoin was formally recognized as a financial instrument, crypto custody licenses started being issued, and more importantly, Germany began preparing for MiCA long before it became law.

That early move matters because regulation rewards preparation. Banks and financial institutions in Germany have been working with BaFin for years now, learning what custody really means in practice – governance, controls, audits, and operational discipline. So when MiCA came into force in December 2024, Germany didn’t need to scramble. Others did.

MiCA as a Distribution Gateway

MiCA isn’t just another compliance layer; it’s a single rulebook for all 27 EU countries. Once a CASP is licensed in Germany and meets BaFin’s standards, it can passport services across the EU. That changes the math completely.

Building in Germany isn’t about serving one country; it’s about unlocking the entire European market. For a German white-label crypto wallet solution, this means one thing – if you invest properly in German compliance, you’re not just launching locally, you’re setting yourself up to reach nearly 450 million users across Europe.

BaFin’s Custody Requirements Raise the Bar (and Your Moat)

BaFin’s 2025 custody reforms raised eyebrows, mostly because of the numbers. €750,000 in own funds for custody-only firms, and up to €2 million if custody is combined with trading or brokerage. On paper, that looks heavy, but in reality, it’s a filter.

Those requirements remove weak operators from the market and replace noise with trust. For banks and enterprises choosing a white-label custody partner, knowing that the provider meets strict capital rules and undergoes regular audits is a serious confidence booster. So compliance stops being a cost and starts becoming part of the product.

Cold Storage, Segregation, and Insurance

BaFin doesn’t stop at licensing. It gets very specific about how custody must actually work. Client assets must be segregated from proprietary funds, blockchain balances must reconcile in real time with internal ledgers, and cold storage has to be geographically diversified, with at least 30% held outside Germany. Add to that 24-hour disaster recovery and cyber insurance covering 150% of maximum client holdings.

None of this is optional in a wallet built for Germany. Any cryptocurrency wallet development company serious about this market has to design for these rules from day one. But once that infrastructure is in place, it becomes a real advantage. In Germany, regulation forces you to answer those questions properly, and that’s exactly why trust follows.

Read Also: How much would it cost to create a Crypto wallet on Solana?

Why Do White Label Wallets in Germany Fit a Compliance-First Market So Well?

Germans have a cultural expectation of order, transparency, and accountability. This is reflected in their financial system, think BaFin, the Bundesbank, and decades of banking stability. A white label wallet that wants to succeed in Germany needs to match this cultural DNA.

Compliance as a Feature, Not a Burden

Here’s the shift happening in 2026: compliance is becoming a differentiator, not a barrier. A white-label wallet in Germany that includes built-in KYC/AML flows, transaction monitoring, audit logs, and regulatory reporting is selling trust.

When a German bank considers adopting a white-label wallet, executives ask:

- Does it handle our compliance workflows?

- Can our audit team pull reports directly?

- Does it flag suspicious transactions?

- Is the data handling GDPR-compliant?

A white-label solution that answers yes to all of these doesn’t just get approved faster; it becomes a strategic asset in the bank’s compliance arsenal.

Pre-Audited Custody Modules

The best white-label solutions ship with pre-audited custody modules that already comply with BaFin expectations around key management, segregation of duties, governance, and incident response. This means a bank can deploy a wallet knowing that the underlying custody infrastructure has been independently verified.

This accelerates everything – time-to-market shrinks, legal sign-off becomes easier, and customers get more confidence because the custody provider is regulated and audited.

SEPA, Euro-First Design, and Tax Reporting

A white-label wallet built for Germany looks different than a global wallet. It has:

- SEPA and instant SEPA support built in (Germans expect fast, cheap bank transfers)

- EUR as the primary denomination (not a secondary coin)

- Tax-friendly transaction export that matches German tax authority formats

- German language support with no awkward translations

- KYC flows optimized for German identity verification processes

These aren’t sexy features, but they’re what makes the difference between a wallet that works in Germany and one that’s just technically available there.

How Do White Label Wallets in Germany compare to Fully Custom Crypto Wallet Solutions?

Put yourself in the CTO seat of a German bank. The board has approved crypto, and now the pressure is on. You really only have two paths, and while both look viable on paper, they behave very differently once time, regulation, and risk show up.

You can build a custom wallet in-house, but that usually means 12–18 months of development, hiring 30–50 engineers and compliance specialists, and running repeated audits just to stay alive. Even then, you’re personally managing BaFin interactions, MiCA updates, and security patches, while burning €5–12M before your first customer ever signs up.

Or you deploy a white label wallet from SoluLab, which is what most serious institutions now do. In 8–12 weeks, you’ll be live using pre-audited custody, KYC, and reporting modules, and the vendor handles security certifications and ongoing compliance, often already aligned with BaFin. Instead of betting millions upfront, you operate on a €500K–1.5M annual model and start learning from real users within months.

When you look at it side by side, the decision stops being emotional and becomes operational.

| Factor | Custom Build | White Label Wallet |

| Time to market | 18+ months | 3–4 months |

| Upfront cost | €5–12M | €500K–1.5M/year |

| Compliance load | Fully internal | Vendor-led |

| Security audits | You manage | Pre-certified |

| Regulatory handling | Direct with BaFin | Via licensed partner |

This is why, for banks launching crypto in 2026, white label isn’t a shortcut; it’s the default. While custom teams are still building, competitors are already live, onboarding institutions, and refining the product based on real demand.

The Passporting Advantage Most Teams Miss

There’s another quiet advantage here. A white label wallet built to German BaFin standards can often be extended across other EU markets with minimal changes. You build once, then scale through passporting. With a custom build, every new country becomes a fresh compliance project.

What Should a German White-Label Crypto Wallet Solution Include Before Launch?

Of course, none of this matters if the product itself is weak. Core features like multi-chain support, fiat on-ramps, P2P transfers, mobile apps, and secure backups are expected. In Germany, these are the bare minimum.

What matters is how cleanly all of this works inside regulatory boundaries, because that’s where most products fail. Here are some additional Enhancements we do while building a white label wallet in the German market.

1. Tax-Friendly Reporting

Export transaction history in formats German accountants already use, and clearly tag income, capital gains, mining, or staking. Annual tax summaries make users trust the product.

2. GDPR-First Architecture

Data collection must be minimal and transparent, with clear consent flows and easy options to export or delete user data. In Germany, privacy is the baseline.

3. KYC/AML Optimized for Germany

Onboarding should support Postident and eIDAS, connect smoothly with German banking systems, and maintain audit trails that stand up to BaFin reviews.

4. Clear, Contextual Risk Warnings

Users expect honesty. A web3 wallet must clearly explain volatility, custody risks, and regulatory exposure, without hiding details or sounding alarmist.

5. Institutional-Grade Reporting

Banks need real dashboards like custody balances, volumes, growth, and compliance metrics, so auditors can pull reports instantly, not request manual exports.

6. Stablecoin Support and Education

With MiCA-compliant stablecoins trending, the wallet should support them and clearly explain how different stablecoin wallets work and where the risks sit.

That’s the real reason smart companies choose white label – not because it’s easier, but because it lets them move faster without breaking things that regulators actually care about.

What Is the Smartest Path to Scale White Label Wallets in Germany Across the EU Under MiCA?

If you’re a blockchain development company, a bank, or a fintech looking to launch a white-label wallet in Germany, this is usually how it plays out in the real world, not on pitch decks. Germany works well as a starting point because the rules are clear, regulators are predictable, and once you get it right here, scaling across the EU becomes far more manageable.

Phase 1: Germany Pilot (Months 1–4)

You begin with a focused Germany pilot, typically over the first four months. The idea is not to overbuild, but to start in one market where you understand the regulatory landscape and can stay close to compliance. You decide early whether you’ll custody assets yourself or rely on a regulated sub-custodian, then pick a white-label wallet vendor and tailor the product to German UX expectations. Most teams test this with one or two institutional partners, such as a small bank unit or a trading desk, because that’s where real feedback shows up fast.

Phase 2: Compliance Hardening (Months 3–6)

While that pilot is running, you don’t pause. You harden compliance in parallel. This is when ISO 27001 and SOC 2 Type II come into play, along with documented governance, incident response, and AML processes. If you’re offering custody directly, this is also when conversations with BaFin get serious, or you double-check that your sub-custodian is fully licensed.

Phase 3: Commercial Launch (Months 6–9)

By 6-9 months, you’re ready for a proper commercial launch in Germany. At this point, onboarding at scale feels controlled, not chaotic, because audits are done and processes are already tested.

Phase 4: EU Passporting (Months 9–18)

From there, EU passporting becomes less about rebuilding and more about localizing. Languages, tax reporting, and payment rails change, but the core wallet and compliance stack stay intact. This isn’t theory. It’s the path institutions like DekaBank, Deutsche Bank, and DZ Bank are already taking.

Conclusion

Let’s step back and see what’s really happening. Germany isn’t becoming a key player in the white-label crypto wallet market by accident. It’s the result of three converging forces:

- Regulatory clarity and institutional confidence – MiCA created a rulebook; Germany was ready to implement it

- Institutional demand – Banks representing tens of millions of customers are actively building crypto services

- Market momentum – Germany’s fintech sector is maturing, and crypto is no longer fringe

For blockchain companies, banks, startups, and investors, this creates an opportunity window that probably doesn’t stay open forever. Right now, in 2026, there’s still room to become a leader, but in two years, the market will be more consolidated. The time to move is now.

If you’re thinking about entering the market, the answer isn’t to build a custom wallet. The answer is to find a trusted crypto solutions development partner like SoluLab, to customize it for German requirements, launch in 3-4 months, and then scale. That’s the playbook that’s working. Germany is no longer playing catch-up on crypto. It’s leading Europe. And the white label wallet market is where a lot of that leadership will be decided.

FAQs

With over 3 years of experience, I specialize in breaking down complex Web3 and crypto concepts into clear, actionable content. From deep-dive technical explainers to project documentation, I help brands educate and engage their audience through well-researched, developer-friendly writing.

![Why Invest in Cryptocurrency Wallet Development [2026 Guide]](https://www.solulab.com/wp-content/uploads/2023/10/Rise-of-Crypto-Wallets-300x149.png)